What is Global DC Distribution Networks Market?

The Global DC Distribution Networks Market refers to the worldwide industry focused on the development, implementation, and management of direct current (DC) power distribution systems. Unlike traditional alternating current (AC) systems, DC distribution networks offer several advantages, including improved energy efficiency, reduced power losses, and enhanced compatibility with renewable energy sources like solar panels and wind turbines. These networks are increasingly being adopted in various sectors, such as commercial buildings, telecommunications, electric vehicle charging, and military applications, due to their ability to efficiently manage and distribute power. The market encompasses a wide range of components, including converters, inverters, and control systems, which are essential for the seamless operation of DC networks. As the demand for sustainable and efficient energy solutions grows, the Global DC Distribution Networks Market is poised for significant expansion, driven by technological advancements and the increasing integration of renewable energy sources into power grids. This market plays a crucial role in the transition towards more sustainable energy systems, offering solutions that align with global efforts to reduce carbon emissions and enhance energy security.

Low Voltage, Medium Voltage, High Voltage in the Global DC Distribution Networks Market:

In the context of the Global DC Distribution Networks Market, voltage levels are categorized into low, medium, and high voltage, each serving distinct applications and offering unique benefits. Low voltage DC distribution networks typically operate at voltages below 1,500 volts. They are commonly used in residential and commercial buildings, where they power lighting systems, small appliances, and electronic devices. The advantage of low voltage systems lies in their safety and ease of installation, making them ideal for environments where human interaction is frequent. Additionally, low voltage DC networks are increasingly being integrated with renewable energy sources, such as solar panels, to enhance energy efficiency and reduce reliance on traditional power grids. Medium voltage DC distribution networks, on the other hand, operate at voltages ranging from 1,500 to 35,000 volts. These networks are often employed in industrial settings, where they power heavy machinery and equipment. The use of medium voltage DC systems in industrial applications is driven by their ability to deliver high power levels over long distances with minimal energy loss. This makes them suitable for large-scale manufacturing facilities and data centers, where energy efficiency and reliability are paramount. Furthermore, medium voltage DC networks are gaining traction in the renewable energy sector, particularly in wind farms and solar power plants, where they facilitate the efficient transmission of power from generation sites to the grid. High voltage DC distribution networks operate at voltages above 35,000 volts and are primarily used for long-distance power transmission. These networks are essential for connecting remote renewable energy sources, such as offshore wind farms, to the main power grid. High voltage DC systems offer several advantages over traditional AC transmission, including reduced power losses and the ability to transmit power over longer distances without the need for intermediate substations. This makes them a critical component of modern power infrastructure, enabling the integration of renewable energy sources into national and international grids. In addition to their use in renewable energy transmission, high voltage DC networks are also employed in interconnecting different power grids, allowing for the efficient exchange of electricity between regions and countries. This enhances grid stability and energy security, particularly in regions with fluctuating energy demands. Overall, the Global DC Distribution Networks Market is characterized by a diverse range of voltage levels, each tailored to specific applications and offering unique benefits. As the demand for efficient and sustainable energy solutions continues to grow, the adoption of DC distribution networks across various voltage levels is expected to increase, driven by advancements in technology and the integration of renewable energy sources.

Commercial Building Subsystems, Telecom/Village Power Systems, Electric Vehicle Charging Systems, LED Lighting Anchors, Military Applications, Other in the Global DC Distribution Networks Market:

The Global DC Distribution Networks Market finds extensive usage across various sectors, each leveraging the unique advantages of DC power distribution to enhance efficiency and sustainability. In commercial building subsystems, DC distribution networks are increasingly being adopted to power lighting systems, HVAC units, and other building automation technologies. The use of DC power in these applications reduces energy losses associated with AC-DC conversion, leading to improved energy efficiency and lower operational costs. Additionally, DC networks facilitate the integration of renewable energy sources, such as solar panels, into building power systems, further enhancing sustainability. In the telecom and village power systems sector, DC distribution networks play a crucial role in powering remote communication infrastructure and off-grid communities. The ability of DC systems to efficiently transmit power over long distances with minimal losses makes them ideal for these applications, where reliable and sustainable power supply is essential. Furthermore, the use of DC power in telecom systems reduces the need for complex power conversion equipment, simplifying system design and maintenance. Electric vehicle charging systems are another key area where DC distribution networks are making a significant impact. The growing adoption of electric vehicles has led to increased demand for efficient and fast charging solutions, which DC networks are well-suited to provide. DC fast chargers can deliver high power levels directly to vehicle batteries, reducing charging times and enhancing the convenience of electric vehicle ownership. Additionally, the integration of DC distribution networks with renewable energy sources, such as solar panels, enables the development of sustainable charging infrastructure, further promoting the adoption of electric vehicles. In the realm of LED lighting anchors, DC distribution networks offer significant advantages in terms of energy efficiency and control. LED lighting systems inherently operate on DC power, making them well-suited for integration with DC distribution networks. This eliminates the need for AC-DC conversion, reducing energy losses and improving overall system efficiency. Furthermore, DC networks enable advanced lighting control and automation, allowing for the implementation of smart lighting solutions that enhance energy savings and user comfort. Military applications also benefit from the use of DC distribution networks, particularly in remote and mobile operations. The ability of DC systems to efficiently transmit power over long distances and operate in harsh environments makes them ideal for military applications, where reliable and resilient power supply is critical. Additionally, the use of DC power in military systems reduces the need for complex power conversion equipment, simplifying system design and enhancing operational efficiency. Other sectors, such as data centers and industrial automation, are also increasingly adopting DC distribution networks to enhance energy efficiency and sustainability. In data centers, the use of DC power reduces energy losses associated with AC-DC conversion, leading to improved energy efficiency and lower operational costs. In industrial automation, DC networks enable the efficient operation of machinery and equipment, reducing energy consumption and enhancing productivity. Overall, the Global DC Distribution Networks Market is characterized by a diverse range of applications, each leveraging the unique advantages of DC power distribution to enhance efficiency and sustainability. As the demand for efficient and sustainable energy solutions continues to grow, the adoption of DC distribution networks across various sectors is expected to increase, driven by advancements in technology and the integration of renewable energy sources.

Global DC Distribution Networks Market Outlook:

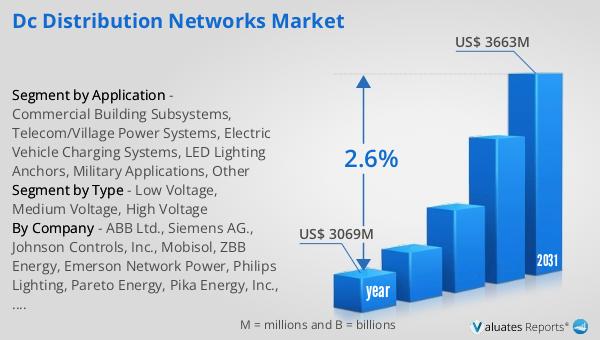

The outlook for the Global DC Distribution Networks Market indicates a positive growth trajectory over the coming years. In 2024, the market was valued at approximately $3,069 million, reflecting its significant role in the energy sector. By 2031, it is anticipated that the market will expand to a revised size of around $3,663 million. This growth is expected to occur at a compound annual growth rate (CAGR) of 2.6% during the forecast period. This steady growth rate underscores the increasing adoption of DC distribution networks across various industries, driven by the need for efficient and sustainable energy solutions. The market's expansion is likely to be fueled by technological advancements, the integration of renewable energy sources, and the growing demand for energy-efficient power distribution systems. As industries and governments worldwide continue to prioritize sustainability and energy efficiency, the Global DC Distribution Networks Market is poised to play a crucial role in the transition towards more sustainable energy systems. The market's growth is also expected to be supported by the increasing adoption of electric vehicles, the expansion of renewable energy infrastructure, and the rising demand for efficient power distribution solutions in commercial and industrial applications. Overall, the Global DC Distribution Networks Market is set to experience steady growth, driven by the increasing demand for efficient and sustainable energy solutions across various sectors.

| Report Metric | Details |

| Report Name | DC Distribution Networks Market |

| Accounted market size in year | US$ 3069 million |

| Forecasted market size in 2031 | US$ 3663 million |

| CAGR | 2.6% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | ABB Ltd., Siemens AG., Johnson Controls, Inc., Mobisol, ZBB Energy, Emerson Network Power, Philips Lighting, Pareto Energy, Pika Energy, Inc., Nextek Power Systems, Inc. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |