What is Global CAR T-Cell Therapy Market?

The Global CAR T-Cell Therapy Market is a rapidly evolving sector within the field of oncology, focusing on a groundbreaking approach to cancer treatment. CAR T-cell therapy involves modifying a patient's T-cells, a type of immune cell, to better recognize and attack cancer cells. This therapy has shown remarkable success in treating certain types of blood cancers, such as leukemia and lymphoma, by targeting specific proteins on the surface of cancer cells. The market for CAR T-cell therapy is driven by increasing incidences of cancer worldwide, advancements in genetic engineering, and a growing understanding of tumor immunology. As more clinical trials demonstrate the efficacy and safety of CAR T-cell therapies, regulatory approvals are expanding, further fueling market growth. The therapy's potential to provide long-term remission and even cure certain cancers positions it as a transformative force in oncology, attracting significant investment from pharmaceutical companies and research institutions. However, challenges such as high treatment costs, complex manufacturing processes, and potential side effects remain. Despite these hurdles, the Global CAR T-Cell Therapy Market is poised for substantial growth, offering hope to patients and reshaping the landscape of cancer treatment.

CD19 - Targeted, BCMA - Targeted in the Global CAR T-Cell Therapy Market:

CD19-targeted and BCMA-targeted therapies are two prominent approaches within the Global CAR T-Cell Therapy Market, each focusing on different cancer types and patient needs. CD19-targeted CAR T-cell therapy is primarily used to treat B-cell malignancies, such as acute lymphoblastic leukemia (ALL) and certain types of non-Hodgkin lymphoma. CD19 is a protein found on the surface of B-cells, and by engineering T-cells to target this protein, the therapy can effectively eliminate cancerous B-cells. This approach has shown high response rates and durable remissions in patients, making it a cornerstone of CAR T-cell therapy. On the other hand, BCMA-targeted CAR T-cell therapy is designed to treat multiple myeloma, a cancer of plasma cells. BCMA, or B-cell maturation antigen, is a protein expressed on the surface of malignant plasma cells. By targeting BCMA, this therapy aims to eradicate myeloma cells, offering a new treatment option for patients who have exhausted other therapies. Both CD19 and BCMA-targeted therapies represent significant advancements in personalized medicine, as they are tailored to the specific antigens present on a patient's cancer cells. The development of these therapies involves complex processes, including the extraction and genetic modification of a patient's T-cells, followed by their expansion and reinfusion into the patient. Despite the challenges associated with manufacturing and delivering these therapies, their potential to provide long-lasting remissions and improve survival rates is driving their adoption in clinical practice. The success of CD19 and BCMA-targeted therapies has also spurred further research into other potential targets, expanding the scope of CAR T-cell therapy to a broader range of cancers. As the Global CAR T-Cell Therapy Market continues to evolve, these targeted therapies are expected to play a crucial role in advancing cancer treatment and improving patient outcomes.

Lymphoma, Multiple Myeloma in the Global CAR T-Cell Therapy Market:

The Global CAR T-Cell Therapy Market has shown significant promise in the treatment of lymphoma and multiple myeloma, two areas where traditional therapies often fall short. In lymphoma, CAR T-cell therapy has emerged as a game-changer, particularly for patients with relapsed or refractory disease. By targeting specific antigens on the surface of lymphoma cells, such as CD19, CAR T-cell therapy can induce deep and durable remissions, offering hope to patients who have exhausted other treatment options. Clinical trials have demonstrated impressive response rates, with some patients achieving complete remission. This success has led to the approval of several CAR T-cell therapies for lymphoma, expanding treatment options and improving outcomes for patients. In multiple myeloma, BCMA-targeted CAR T-cell therapy is making waves as a novel treatment approach. Multiple myeloma is a challenging cancer to treat, with many patients experiencing relapses after initial therapy. BCMA-targeted CAR T-cell therapy offers a new avenue for treatment, with studies showing promising results in terms of response rates and progression-free survival. By specifically targeting BCMA on myeloma cells, this therapy can effectively reduce tumor burden and improve quality of life for patients. However, the use of CAR T-cell therapy in these areas is not without challenges. The high cost of treatment, potential side effects, and the need for specialized facilities and expertise for manufacturing and administration are significant hurdles. Despite these challenges, the potential benefits of CAR T-cell therapy in lymphoma and multiple myeloma are driving continued research and development, with the aim of making these therapies more accessible and effective for a broader range of patients. As the Global CAR T-Cell Therapy Market continues to grow, its impact on the treatment landscape for lymphoma and multiple myeloma is expected to be profound, offering new hope and possibilities for patients worldwide.

Global CAR T-Cell Therapy Market Outlook:

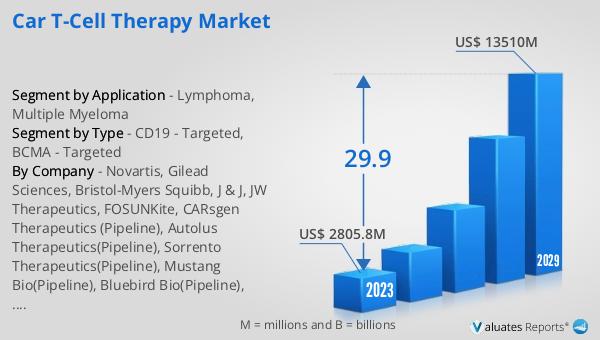

The global market for CAR T-cell therapy was valued at $4,087 million in 2024 and is anticipated to expand significantly, reaching an estimated $21,680 million by 2031. This growth is driven by a robust compound annual growth rate (CAGR) of 26.0% during the forecast period. Dominating the market are three major players: Novartis, Gilead Sciences, and Bristol-Myers Squibb, collectively holding over 99% of the market share. Among these, Gilead Sciences stands out as the largest player, commanding more than 50% of the market. North America emerges as the most significant consumer market for CAR T-cell therapy, accounting for over 65% of the global market share. In terms of therapy types, CD19-targeted CAR T-cell therapy is predominant, capturing over 90% of the market share. When it comes to applications, the use of CAR T-cell therapy in treating lymphoma is particularly noteworthy, with a market share exceeding 90%. This data underscores the substantial impact and potential of CAR T-cell therapy in transforming cancer treatment, driven by key players and significant regional demand.

| Report Metric | Details |

| Report Name | CAR T-Cell Therapy Market |

| Accounted market size in year | US$ 4087 million |

| Forecasted market size in 2031 | US$ 21680 million |

| CAGR | 26.0% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Novartis, Gilead Sciences, Bristol-Myers Squibb, J & J, JW Therapeutics, FOSUNKite, CARsgen Therapeutics (Pipeline), Autolus Therapeutics(Pipeline), Sorrento Therapeutics(Pipeline), Mustang Bio(Pipeline), Bluebird Bio(Pipeline), Cellectis(Pipeline), Allogene Therapeutics(Pipeline), Celyad(Pipeline) |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |