What is Global Automotive Transient Suppression Diodes Market?

The Global Automotive Transient Suppression Diodes Market is a specialized segment within the broader automotive electronics industry. These diodes are crucial components designed to protect automotive electronic systems from voltage spikes and transient surges, which can occur due to various factors such as load switching, electrostatic discharge, and lightning strikes. As vehicles become increasingly sophisticated with advanced electronic systems, the demand for reliable transient suppression solutions has grown significantly. These diodes ensure the longevity and reliability of automotive electronics by clamping excess voltage and preventing damage to sensitive components. The market encompasses a range of diode types, including uni-polar and bi-polar TVS (Transient Voltage Suppression) diodes, each offering specific benefits depending on the application. The market's growth is driven by the rising adoption of electric vehicles, advancements in automotive technology, and stringent safety regulations. Key players in this market are continuously innovating to enhance the performance and efficiency of these diodes, catering to the evolving needs of the automotive industry. As a result, the Global Automotive Transient Suppression Diodes Market is poised for steady growth, reflecting the increasing complexity and electronic content in modern vehicles.

Uni - Polar TVS, Bi - Polar TVS in the Global Automotive Transient Suppression Diodes Market:

Uni-polar and bi-polar TVS diodes are integral components of the Global Automotive Transient Suppression Diodes Market, each serving distinct roles in safeguarding automotive electronics. Uni-polar TVS diodes are designed to protect against voltage spikes in one direction, making them suitable for applications where the polarity of the voltage is known and consistent. These diodes are typically used in circuits where the voltage is expected to remain positive or negative, providing a straightforward and efficient solution for transient suppression. They are often employed in systems with a single power supply polarity, such as certain types of sensors and control units in vehicles. On the other hand, bi-polar TVS diodes offer protection against voltage spikes in both directions, making them versatile and ideal for applications where the polarity of the voltage can vary. This feature is particularly beneficial in automotive environments where voltage fluctuations can occur due to various factors, including load dumps and inductive load switching. Bi-polar TVS diodes are commonly used in more complex automotive systems, such as infotainment systems, advanced driver-assistance systems (ADAS), and electric vehicle charging circuits, where bidirectional protection is essential. The choice between uni-polar and bi-polar TVS diodes depends on the specific requirements of the application, including the expected voltage conditions and the level of protection needed. In the context of the Global Automotive Transient Suppression Diodes Market, bi-polar TVS diodes hold a significant market share due to their versatility and ability to provide comprehensive protection in diverse automotive applications. As vehicles continue to evolve with more electronic content and connectivity features, the demand for robust transient suppression solutions like bi-polar TVS diodes is expected to rise. Manufacturers in this market are focused on developing diodes with enhanced performance characteristics, such as faster response times, higher power handling capabilities, and improved thermal management, to meet the stringent demands of modern automotive systems. Additionally, the integration of these diodes into compact and lightweight packages is a key trend, aligning with the industry's push towards miniaturization and space-saving designs. Overall, uni-polar and bi-polar TVS diodes play a critical role in ensuring the reliability and safety of automotive electronics, contributing to the growth and development of the Global Automotive Transient Suppression Diodes Market.

Commercial Vehicle, Passenger Car in the Global Automotive Transient Suppression Diodes Market:

The usage of Global Automotive Transient Suppression Diodes Market in commercial vehicles and passenger cars is pivotal in enhancing the safety and reliability of these vehicles. In commercial vehicles, which include trucks, buses, and heavy-duty vehicles, transient suppression diodes are essential for protecting the extensive electronic systems that control everything from engine management to telematics and communication systems. These vehicles often operate in harsh environments and are subject to significant electrical stress due to their size and complexity. Transient suppression diodes help prevent voltage spikes that can damage critical components, ensuring the smooth operation of commercial vehicles and reducing downtime caused by electronic failures. In passenger cars, the role of transient suppression diodes is equally important. Modern passenger cars are equipped with a wide array of electronic systems, including infotainment, navigation, climate control, and advanced safety features like ADAS. These systems are highly sensitive to voltage fluctuations, and any disruption can lead to malfunctions or even complete system failures. Transient suppression diodes provide a protective barrier against such disruptions, enhancing the overall reliability and performance of passenger cars. As the automotive industry continues to shift towards electric and hybrid vehicles, the importance of transient suppression diodes is further amplified. Electric vehicles, in particular, have high-voltage systems that require robust protection against transient events to ensure the safety of both the vehicle and its occupants. The integration of transient suppression diodes in these vehicles helps mitigate the risks associated with high-voltage spikes, contributing to the safe and efficient operation of electric and hybrid vehicles. Furthermore, the increasing adoption of connected car technologies and the Internet of Things (IoT) in the automotive sector has led to a greater need for reliable transient suppression solutions. These technologies rely on seamless communication and data exchange between various electronic systems, making them vulnerable to voltage disturbances. Transient suppression diodes play a crucial role in maintaining the integrity of these systems, supporting the growth of connected and autonomous vehicles. In summary, the usage of Global Automotive Transient Suppression Diodes Market in commercial vehicles and passenger cars is integral to the advancement of automotive technology, providing essential protection for the complex electronic systems that define modern vehicles.

Global Automotive Transient Suppression Diodes Market Outlook:

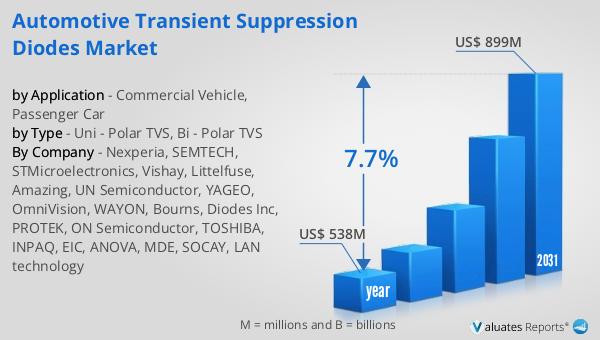

The worldwide market for Automotive Transient Suppression Diodes was valued at $538 million in 2024 and is anticipated to expand to a revised size of $899 million by 2031, reflecting a compound annual growth rate (CAGR) of 7.7% throughout the forecast period. The top five global manufacturers in this sector, namely Nexperia, SEMTECH, STMicroelectronics, Vishay, and Littelfuse, collectively hold over 50% of the market share. Among these, Nexperia stands out as the largest manufacturer, commanding approximately 15% of the market. China emerges as the leading global producer of automotive transient suppression diodes, contributing around 60% to the market share. In terms of diode types, bi-polar TVS diodes dominate with a market share exceeding 90%. This market outlook highlights the significant role of key players and regions in shaping the dynamics of the Global Automotive Transient Suppression Diodes Market. The robust growth trajectory underscores the increasing demand for effective transient suppression solutions in the automotive industry, driven by advancements in vehicle electronics and the rising adoption of electric and hybrid vehicles. As the market continues to evolve, manufacturers are focusing on innovation and strategic partnerships to enhance their competitive edge and meet the growing needs of the automotive sector.

| Report Metric | Details |

| Report Name | Automotive Transient Suppression Diodes Market |

| Accounted market size in year | US$ 538 million |

| Forecasted market size in 2031 | US$ 899 million |

| CAGR | 7.7% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Nexperia, SEMTECH, STMicroelectronics, Vishay, Littelfuse, Amazing, UN Semiconductor, YAGEO, OmniVision, WAYON, Bourns, Diodes Inc, PROTEK, ON Semiconductor, TOSHIBA, INPAQ, EIC, ANOVA, MDE, SOCAY, LAN technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |