What is Global Drug Integrated Polymer Fibers Market?

The Global Drug Integrated Polymer Fibers Market is a specialized segment within the broader pharmaceutical and medical device industries. These fibers are engineered to deliver drugs in a controlled manner, offering a novel approach to drug delivery systems. The integration of drugs into polymer fibers allows for precise control over the release rate, enhancing the efficacy and safety of therapeutic treatments. This market is driven by the increasing demand for advanced drug delivery systems that can improve patient outcomes and reduce side effects. The fibers are typically made from biodegradable polymers, which break down in the body over time, releasing the drug in a controlled manner. This technology is particularly beneficial for chronic conditions that require long-term medication management. The market is expected to grow as more pharmaceutical companies and healthcare providers recognize the benefits of drug-integrated polymer fibers in improving patient care and treatment outcomes. The development of new polymers and drug formulations is also contributing to the expansion of this market, offering new opportunities for innovation and growth. As the healthcare industry continues to evolve, the Global Drug Integrated Polymer Fibers Market is poised to play a significant role in the future of drug delivery systems.

Polylactic Acid, Polydioxanone, Polycaprolactone in the Global Drug Integrated Polymer Fibers Market:

Polylactic Acid (PLA), Polydioxanone (PDO), and Polycaprolactone (PCL) are three key biodegradable polymers used in the Global Drug Integrated Polymer Fibers Market. Each of these polymers has unique properties that make them suitable for specific applications in drug delivery and medical devices. PLA is a thermoplastic aliphatic polyester derived from renewable resources like corn starch or sugarcane. It is known for its biodegradability and biocompatibility, making it an ideal choice for drug delivery systems. PLA fibers can be engineered to degrade at a controlled rate, allowing for the sustained release of drugs over time. This property is particularly useful in applications where long-term drug delivery is required, such as in the treatment of chronic diseases. PLA is also used in the production of sutures, stents, and other medical devices where biodegradability is a key requirement. Polydioxanone (PDO) is another biodegradable polymer used in the drug-integrated polymer fibers market. PDO is known for its flexibility and strength, making it suitable for applications that require a combination of durability and biodegradability. PDO fibers are commonly used in surgical sutures, where they provide the necessary strength to hold tissues together while gradually breaking down in the body. This eliminates the need for suture removal, reducing the risk of infection and improving patient comfort. PDO is also used in the development of drug delivery systems, where its controlled degradation rate allows for the sustained release of therapeutic agents. Polycaprolactone (PCL) is a biodegradable polyester with a low melting point and high flexibility. PCL is used in a variety of medical applications, including drug delivery systems, tissue engineering, and wound healing. Its flexibility and biocompatibility make it an ideal material for drug-integrated polymer fibers, where it can be used to deliver a wide range of therapeutic agents. PCL fibers can be engineered to degrade over a period of months, providing a sustained release of drugs for long-term treatment. This property is particularly beneficial in applications such as vascular stents and grafts, where long-term drug delivery is required to prevent restenosis and promote healing. In summary, PLA, PDO, and PCL are three key polymers used in the Global Drug Integrated Polymer Fibers Market. Each of these materials offers unique properties that make them suitable for specific applications in drug delivery and medical devices. The choice of polymer depends on the specific requirements of the application, including the desired degradation rate, mechanical properties, and biocompatibility. As the market continues to grow, the development of new polymers and drug formulations will provide new opportunities for innovation and advancement in the field of drug-integrated polymer fibers.

Drug Delivery, Orthopaedic Sutures, Vascular Stents, Vascular Grafts, Dermal Wound Healing in the Global Drug Integrated Polymer Fibers Market:

The Global Drug Integrated Polymer Fibers Market finds its application in various areas, including drug delivery, orthopedic sutures, vascular stents, vascular grafts, and dermal wound healing. In drug delivery, these fibers offer a controlled release mechanism that enhances the efficacy of therapeutic treatments. By integrating drugs into polymer fibers, it is possible to achieve a sustained release of medication over an extended period, reducing the frequency of dosing and improving patient compliance. This is particularly beneficial for chronic conditions that require long-term medication management. In orthopedic sutures, drug-integrated polymer fibers provide the dual benefit of mechanical support and localized drug delivery. These sutures can be used to deliver anti-inflammatory or antimicrobial agents directly to the surgical site, reducing the risk of infection and promoting faster healing. The biodegradability of the fibers eliminates the need for suture removal, further enhancing patient comfort and reducing the risk of complications. Vascular stents and grafts are another key application area for drug-integrated polymer fibers. These devices are used to treat conditions such as coronary artery disease and peripheral artery disease, where maintaining blood flow is critical. By incorporating drugs into the polymer fibers, it is possible to prevent restenosis and promote healing, improving the long-term success of the treatment. The controlled release of drugs from the fibers ensures that therapeutic levels are maintained over an extended period, reducing the risk of complications and improving patient outcomes. In dermal wound healing, drug-integrated polymer fibers offer a novel approach to wound care. These fibers can be used to deliver growth factors, antimicrobial agents, or other therapeutic compounds directly to the wound site, promoting faster healing and reducing the risk of infection. The fibers can be engineered to degrade at a controlled rate, providing a sustained release of medication that supports the natural healing process. This approach is particularly beneficial for chronic wounds or wounds that are difficult to heal, where traditional treatments may be less effective. Overall, the Global Drug Integrated Polymer Fibers Market offers a range of innovative solutions for drug delivery and medical device applications. By leveraging the unique properties of biodegradable polymers, it is possible to develop advanced therapeutic systems that improve patient outcomes and enhance the efficacy of medical treatments. As the market continues to evolve, the development of new applications and technologies will drive further growth and innovation in this exciting field.

Global Drug Integrated Polymer Fibers Market Outlook:

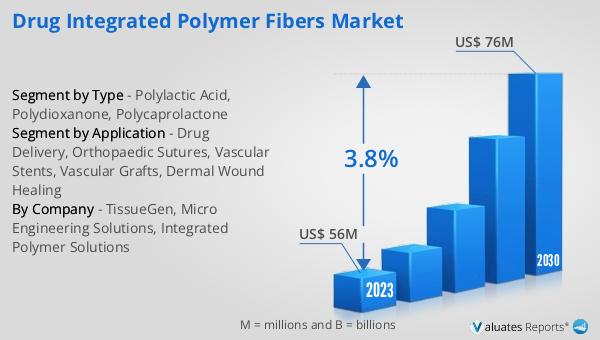

The outlook for the Global Drug Integrated Polymer Fibers Market indicates a steady growth trajectory. The market is anticipated to expand from $61 million in 2024 to $76 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 3.8% over the forecast period. This growth is driven by the increasing demand for advanced drug delivery systems that offer improved patient outcomes and reduced side effects. In the broader context, the global pharmaceutical market was valued at $1,475 billion in 2022 and is expected to grow at a CAGR of 5% over the next six years. This growth is indicative of the rising demand for innovative therapeutic solutions and the increasing investment in research and development. In comparison, the chemical drug market has shown a steady increase from $1,005 billion in 2018 to $1,094 billion in 2022. This growth highlights the ongoing demand for chemical-based therapeutics and the continued importance of this segment within the pharmaceutical industry. The Global Drug Integrated Polymer Fibers Market is poised to benefit from these broader industry trends, as the demand for advanced drug delivery systems continues to rise. The development of new polymers and drug formulations will further drive innovation and growth in this market, offering new opportunities for companies operating in this space. As the healthcare industry continues to evolve, the Global Drug Integrated Polymer Fibers Market is expected to play a significant role in shaping the future of drug delivery systems.

| Report Metric | Details |

| Report Name | Drug Integrated Polymer Fibers Market |

| Accounted market size in 2024 | US$ 61 million |

| Forecasted market size in 2030 | US$ 76 million |

| CAGR | 3.8 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Segment by Region |

|

| By Company | Integrated Polymer Solutions |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |