What is Global Anode Layer Ion Sources Market?

The Global Anode Layer Ion Sources Market is a specialized segment within the broader ion source industry, focusing on devices that generate ions through an anode layer. These ion sources are crucial in various applications, including materials processing, surface treatment, and thin-film deposition. The market is driven by the increasing demand for advanced materials and technologies in industries such as electronics, aerospace, and automotive. Anode layer ion sources are known for their efficiency and ability to produce a high-density ion beam, making them ideal for precision applications. The market is characterized by continuous innovation and development, with manufacturers striving to enhance the performance and versatility of these ion sources. As industries continue to seek more efficient and effective methods for material modification and surface treatment, the demand for anode layer ion sources is expected to grow. This growth is further supported by advancements in technology and the increasing adoption of ion beam techniques in various industrial processes. The market is also influenced by factors such as regulatory standards, environmental concerns, and the need for cost-effective solutions. Overall, the Global Anode Layer Ion Sources Market plays a vital role in supporting the advancement of modern technologies and industrial processes.

Round, Linear in the Global Anode Layer Ion Sources Market:

In the Global Anode Layer Ion Sources Market, two primary configurations are prevalent: round and linear ion sources. Round ion sources are typically used in applications where a focused, high-density ion beam is required. These sources are designed to produce a circular beam profile, making them ideal for tasks that demand precision and uniformity, such as ion beam sputtering and ion beam assisted deposition. The round configuration allows for a concentrated ion flow, which is beneficial in achieving consistent results across the treated surface. On the other hand, linear ion sources are designed to produce a broad, rectangular ion beam, which is particularly useful in applications that require coverage over a larger area. This configuration is often employed in processes like ion cleaning and ion etching, where a wide beam can efficiently treat extensive surfaces. Linear ion sources are favored in industries that require high throughput and efficiency, as they can cover more surface area in a shorter amount of time compared to their round counterparts. Both round and linear ion sources have their unique advantages and are chosen based on the specific requirements of the application. The choice between round and linear configurations often depends on factors such as the size and shape of the target surface, the desired ion beam density, and the specific process requirements. In many cases, the decision is also influenced by the cost considerations and the availability of equipment that can accommodate the chosen ion source configuration. As the Global Anode Layer Ion Sources Market continues to evolve, manufacturers are focusing on developing versatile ion sources that can cater to a wide range of applications. This includes innovations in design and technology that enhance the performance and adaptability of both round and linear ion sources. The market is also witnessing a trend towards the integration of advanced control systems that allow for precise manipulation of the ion beam, further expanding the potential applications of these devices. Additionally, there is a growing emphasis on sustainability and energy efficiency, prompting manufacturers to develop ion sources that minimize energy consumption and reduce environmental impact. This is particularly important in industries that are subject to stringent environmental regulations and are seeking to adopt greener technologies. As a result, the Global Anode Layer Ion Sources Market is not only expanding in terms of application scope but also evolving to meet the changing demands of modern industries. The ongoing advancements in ion source technology are expected to drive further growth and innovation in this market, providing new opportunities for manufacturers and end-users alike.

Ion Cleaning, Ion Etching, Ion Beam Assisted Deposition, Ion Beam Sputtering in the Global Anode Layer Ion Sources Market:

The Global Anode Layer Ion Sources Market finds extensive usage in various applications, including ion cleaning, ion etching, ion beam assisted deposition, and ion beam sputtering. In ion cleaning, anode layer ion sources are used to remove contaminants and impurities from surfaces, preparing them for subsequent processing. This process is essential in industries such as semiconductor manufacturing, where cleanliness is critical to ensure the quality and performance of electronic components. The high-density ion beam produced by anode layer ion sources effectively dislodges particles and residues, resulting in a clean and pristine surface. Ion etching, another key application, involves the use of ion beams to selectively remove material from a substrate. This technique is widely used in the fabrication of microelectronic devices, where precise patterning and material removal are required. Anode layer ion sources provide the precision and control needed to achieve the desired etching results, making them indispensable in the production of advanced electronic components. Ion beam assisted deposition is a process that combines ion beam technology with traditional deposition methods to enhance the properties of thin films. In this application, anode layer ion sources are used to bombard the substrate with ions during the deposition process, improving film adhesion, density, and uniformity. This technique is particularly valuable in the production of optical coatings, protective films, and other advanced materials. Finally, ion beam sputtering is a method used to deposit thin films by sputtering material from a target onto a substrate. Anode layer ion sources play a crucial role in this process by providing the ion beam needed to dislodge atoms from the target material. The resulting thin films are used in a wide range of applications, including electronics, optics, and coatings. The versatility and precision of anode layer ion sources make them an essential tool in these applications, enabling the production of high-quality materials and components. As industries continue to demand more advanced and efficient processing techniques, the usage of anode layer ion sources in these applications is expected to grow, driving further innovation and development in the Global Anode Layer Ion Sources Market.

Global Anode Layer Ion Sources Market Outlook:

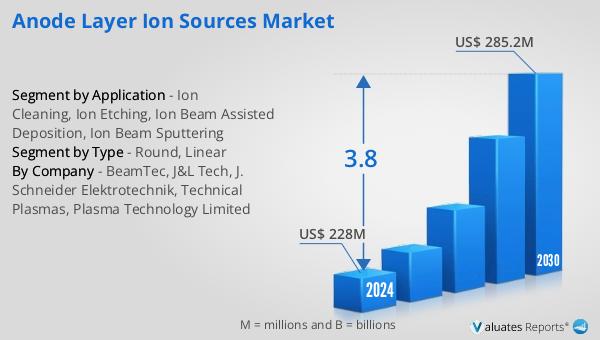

The outlook for the Global Anode Layer Ion Sources Market indicates a promising growth trajectory, with projections suggesting an increase from $228 million in 2024 to $285.2 million by 2030, reflecting a compound annual growth rate (CAGR) of 3.8% during this period. This growth is driven by the rising demand for advanced ion source technologies across various industries. In the construction machinery sector, for instance, there has been a notable increase in sales, particularly in Europe, where sales surged by 24% in 2021. By 2022, the construction machinery revenue in Europe reached approximately $22 billion, while the U.S. market recorded sales of about $36 billion. Asian companies have established a dominant presence in this market, accounting for 50% of the revenue, followed by Europe and North America, which contribute 26% and 23%, respectively. These figures highlight the significant role of Asian companies in the global market, underscoring their competitive advantage and market influence. The growth in the Anode Layer Ion Sources Market is further supported by technological advancements and the increasing adoption of ion beam techniques in various industrial processes. As industries continue to seek more efficient and effective methods for material modification and surface treatment, the demand for anode layer ion sources is expected to grow. This growth is also influenced by factors such as regulatory standards, environmental concerns, and the need for cost-effective solutions. Overall, the Global Anode Layer Ion Sources Market is poised for significant expansion, driven by the increasing demand for advanced materials and technologies in industries such as electronics, aerospace, and automotive.

| Report Metric | Details |

| Report Name | Anode Layer Ion Sources Market |

| Accounted market size in 2024 | US$ 228 million |

| Forecasted market size in 2030 | US$ 285.2 million |

| CAGR | 3.8 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | BeamTec, J&L Tech, J. Schneider Elektrotechnik, Technical Plasmas, Plasma Technology Limited |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |