What is Commercial Grain Mills - Global Market?

Commercial grain mills are essential machines used in the food processing industry to grind grains into flour or meal. These mills are vital for producing a variety of grain-based products, such as bread, pasta, and cereals, which are staples in diets worldwide. The global market for commercial grain mills is driven by the increasing demand for processed grains and the growing awareness of the health benefits associated with whole grains. These mills come in various types, including automatic, manual, and semi-automatic, each catering to different needs and scales of production. The market is characterized by technological advancements that enhance efficiency and output quality. Additionally, the rise in urbanization and changing dietary preferences are contributing to the expansion of this market. As more consumers seek healthier food options, the demand for commercial grain mills is expected to grow, supporting the production of whole grain products. The market is also influenced by factors such as government regulations, environmental concerns, and the availability of raw materials. Overall, the commercial grain mills market plays a crucial role in the global food supply chain, ensuring the availability of essential grain-based products to meet the nutritional needs of the population.

Automatic, Manual, Semi-Automatic in the Commercial Grain Mills - Global Market:

Commercial grain mills are categorized into three main types: automatic, manual, and semi-automatic, each serving distinct purposes and catering to different user needs. Automatic grain mills are designed for high efficiency and large-scale production. They are equipped with advanced technology that allows for continuous operation with minimal human intervention. These mills are ideal for large food processing companies that require consistent and high-volume output. The automation in these mills ensures precision in grinding, leading to uniform particle size and quality. They often come with features such as programmable settings, self-cleaning mechanisms, and energy-efficient motors, making them a preferred choice for industrial applications. On the other hand, manual grain mills are more suited for small-scale operations or personal use. They require human effort to operate, making them less efficient compared to their automatic counterparts. However, they offer the advantage of being more affordable and portable. Manual mills are often used in rural areas or by small businesses that do not have access to electricity or prefer a more traditional approach to grain milling. These mills are simple in design, easy to maintain, and can be used to grind a variety of grains. Semi-automatic grain mills bridge the gap between manual and automatic mills. They offer a balance of efficiency and control, making them suitable for medium-sized operations. These mills require some level of human intervention but are equipped with features that enhance productivity and ease of use. Semi-automatic mills are often used by small to medium-sized enterprises that need a reliable and cost-effective solution for grain milling. They provide flexibility in operation, allowing users to adjust settings according to their specific requirements. The choice between automatic, manual, and semi-automatic grain mills depends on factors such as production scale, budget, and specific needs of the user. Each type has its own advantages and limitations, and understanding these can help businesses make informed decisions when investing in grain milling equipment. As the demand for processed grains continues to rise, the market for commercial grain mills is expected to grow, with each type playing a significant role in meeting the diverse needs of the food processing industry.

Corn, Wheat, Rice, Others in the Commercial Grain Mills - Global Market:

Commercial grain mills are widely used in processing various types of grains, including corn, wheat, rice, and others, each serving different purposes in the food industry. Corn is one of the most commonly processed grains in commercial grain mills. It is used to produce cornmeal, corn flour, and other corn-based products that are staples in many cuisines around the world. The versatility of corn allows it to be used in a wide range of food products, from tortillas and cornbread to snacks and breakfast cereals. Commercial grain mills play a crucial role in ensuring the consistent quality and texture of corn products, which is essential for both consumer satisfaction and meeting industry standards. Wheat is another major grain processed by commercial grain mills. It is the primary ingredient in bread, pasta, and many baked goods, making it a staple in diets globally. The demand for wheat-based products continues to grow, driven by population growth and changing dietary preferences. Commercial grain mills are essential for producing high-quality wheat flour, which is crucial for the texture, taste, and nutritional value of wheat-based products. These mills ensure that the flour is ground to the desired fineness, which is important for achieving the right consistency in baked goods. Rice is also a significant grain processed by commercial grain mills. It is a staple food for a large portion of the world's population, particularly in Asia. Commercial grain mills are used to produce rice flour, which is used in a variety of food products, including noodles, snacks, and gluten-free baked goods. The milling process is critical for removing the husk and bran layers from the rice, resulting in a polished product that is ready for consumption. Other grains processed by commercial grain mills include oats, barley, and rye. These grains are used in a variety of food products, from breakfast cereals and granola bars to beer and whiskey. The versatility of commercial grain mills allows them to handle different types of grains, ensuring that they are ground to the desired consistency for various applications. The ability to process a wide range of grains makes commercial grain mills an essential component of the global food supply chain, supporting the production of diverse and nutritious food products.

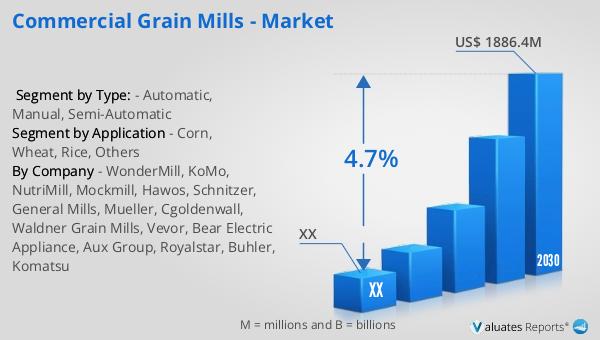

Commercial Grain Mills - Global Market Outlook:

The global market for commercial grain mills was valued at approximately $1,368 million in 2023. It is projected to grow to a revised size of $1,886.4 million by 2030, reflecting a compound annual growth rate (CAGR) of 4.7% during the forecast period from 2024 to 2030. This growth is largely driven by the increasing demand for whole grains, as more consumers become aware of their health benefits. Whole grains are rich in nutrients and fiber, which are essential for maintaining a healthy diet. As a result, there is a growing trend towards incorporating whole grains into daily meals, leading to a higher demand for commercial grain mills. These mills are crucial for processing whole grains into flour and other products that can be easily incorporated into various food items. The market is also influenced by factors such as technological advancements in milling equipment, which enhance efficiency and product quality. Additionally, the rise in health-conscious consumers and the increasing popularity of gluten-free and organic products are contributing to the growth of the commercial grain mills market. As the demand for healthier food options continues to rise, the market for commercial grain mills is expected to expand, supporting the production of nutritious and high-quality grain-based products.

| Report Metric | Details |

| Report Name | Commercial Grain Mills - Market |

| Forecasted market size in 2030 | US$ 1886.4 million |

| CAGR | 4.7% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | WonderMill, KoMo, NutriMill, Mockmill, Hawos, Schnitzer, General Mills, Mueller, Cgoldenwall, Waldner Grain Mills, Vevor, Bear Electric Appliance, Aux Group, Royalstar, Buhler, Komatsu |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |