What is Medical Ultrasonic Scalpel System - Global Market?

The Medical Ultrasonic Scalpel System is a sophisticated surgical tool that has revolutionized the way surgeries are performed globally. This system uses ultrasonic vibrations to cut and coagulate tissue simultaneously, offering a precise and efficient alternative to traditional surgical methods. The technology behind the ultrasonic scalpel allows for minimal thermal damage to surrounding tissues, which is a significant advantage over conventional electrosurgical devices. This precision reduces the risk of complications and promotes faster healing, making it an invaluable tool in various surgical procedures, including those in delicate areas such as the liver or pancreas. The global market for medical ultrasonic scalpel systems is expanding rapidly, driven by the increasing demand for minimally invasive surgeries and the growing awareness of the benefits of advanced surgical technologies. As healthcare systems worldwide strive to improve patient outcomes and reduce recovery times, the adoption of ultrasonic scalpel systems is expected to continue its upward trajectory, making it a critical component of modern surgical practice.

Suction Ultrasonic Scalpel, Cutting Ultrasonic Scalpel in the Medical Ultrasonic Scalpel System - Global Market:

The Medical Ultrasonic Scalpel System encompasses various types of devices, including the Suction Ultrasonic Scalpel and the Cutting Ultrasonic Scalpel, each designed to meet specific surgical needs. The Suction Ultrasonic Scalpel is particularly useful in procedures where fluid management is crucial. It combines the cutting and coagulating capabilities of the ultrasonic scalpel with a suction mechanism, allowing surgeons to maintain a clear surgical field by removing blood and other fluids as they operate. This feature is especially beneficial in surgeries involving highly vascularized tissues, where bleeding can obscure the surgical site and complicate the procedure. By integrating suction, this scalpel type enhances visibility and precision, contributing to more efficient and safer surgeries. On the other hand, the Cutting Ultrasonic Scalpel is designed to provide exceptional cutting precision with minimal thermal spread. This scalpel type is ideal for surgeries requiring meticulous dissection and minimal collateral damage to surrounding tissues. The ultrasonic vibrations enable the scalpel to cut through tissues with ease, reducing the need for excessive force and minimizing trauma to the patient. This precision is particularly advantageous in oncological surgeries, where preserving healthy tissue while removing cancerous growths is paramount. The Cutting Ultrasonic Scalpel's ability to achieve clean and precise cuts makes it a preferred choice for surgeons aiming to optimize surgical outcomes and enhance patient recovery. Both the Suction and Cutting Ultrasonic Scalpels are integral components of the Medical Ultrasonic Scalpel System, contributing to its versatility and effectiveness in a wide range of surgical applications. The global market for these devices is driven by the increasing demand for advanced surgical tools that offer improved precision, safety, and efficiency. As healthcare providers continue to seek innovative solutions to enhance surgical outcomes, the adoption of ultrasonic scalpel systems is expected to grow, further solidifying their role in modern surgical practice. The ongoing advancements in ultrasonic technology and the continuous refinement of these devices ensure that they remain at the forefront of surgical innovation, meeting the evolving needs of surgeons and patients alike.

Hospital, Clinic, Outpatient Center, Others in the Medical Ultrasonic Scalpel System - Global Market:

The Medical Ultrasonic Scalpel System finds extensive usage across various healthcare settings, including hospitals, clinics, outpatient centers, and other medical facilities. In hospitals, these systems are integral to the surgical departments, where they are used in a wide range of procedures, from general surgery to specialized fields such as neurosurgery and cardiovascular surgery. The precision and efficiency offered by ultrasonic scalpels make them invaluable in complex surgeries, where minimizing tissue damage and reducing recovery times are critical. Hospitals, being the primary centers for advanced surgical procedures, are significant adopters of this technology, leveraging its benefits to enhance patient care and surgical outcomes. In clinics, the Medical Ultrasonic Scalpel System is utilized for less invasive procedures that do not require hospitalization. Clinics often focus on outpatient surgeries, where the goal is to perform the procedure and discharge the patient on the same day. The ultrasonic scalpel's ability to reduce bleeding and promote faster healing aligns perfectly with the needs of outpatient surgeries, making it a preferred choice for clinics aiming to provide efficient and effective surgical care. The system's versatility allows it to be used in various specialties, including dermatology, gynecology, and urology, where precise cutting and coagulation are essential. Outpatient centers, similar to clinics, benefit from the use of ultrasonic scalpel systems in performing minimally invasive surgeries. These centers cater to patients who require surgical interventions but do not need the extensive resources of a hospital. The ultrasonic scalpel's ability to perform precise cuts with minimal thermal damage is particularly advantageous in outpatient settings, where quick recovery and minimal postoperative complications are priorities. By incorporating this advanced technology, outpatient centers can offer high-quality surgical care while maintaining cost-effectiveness and patient satisfaction. Beyond hospitals, clinics, and outpatient centers, the Medical Ultrasonic Scalpel System is also used in other medical facilities, such as specialized surgical centers and research institutions. These facilities often focus on specific types of surgeries or experimental procedures, where the precision and versatility of ultrasonic scalpels are highly valued. The system's ability to adapt to various surgical needs makes it a valuable asset in these settings, where innovation and excellence in surgical care are paramount. As the global market for medical ultrasonic scalpel systems continues to grow, their usage across diverse healthcare environments is expected to expand, further enhancing the quality and efficiency of surgical care worldwide.

Medical Ultrasonic Scalpel System - Global Market Outlook:

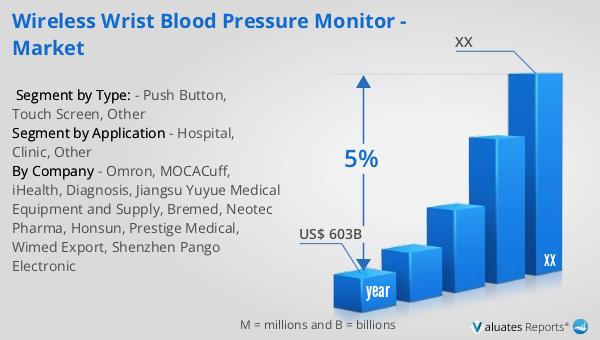

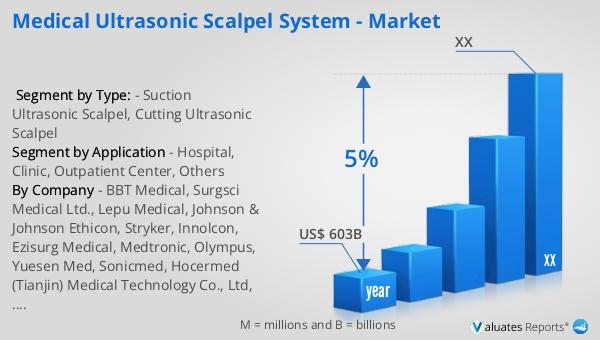

Based on our research, the global market for medical devices, including the Medical Ultrasonic Scalpel System, is projected to reach approximately $603 billion in 2023. This substantial market size reflects the growing demand for advanced medical technologies that enhance patient care and surgical outcomes. The market is anticipated to grow at a compound annual growth rate (CAGR) of 5% over the next six years, indicating a steady increase in the adoption of innovative medical devices. This growth is driven by several factors, including the rising prevalence of chronic diseases, the increasing number of surgical procedures, and the continuous advancements in medical technology. As healthcare systems worldwide strive to improve patient outcomes and reduce healthcare costs, the demand for efficient and effective medical devices is expected to rise. The Medical Ultrasonic Scalpel System, with its ability to provide precise and efficient surgical solutions, is well-positioned to capitalize on this growing market. As the market continues to evolve, the focus on innovation and quality will remain paramount, ensuring that medical devices meet the ever-changing needs of healthcare providers and patients alike.

| Report Metric | Details |

| Report Name | Medical Ultrasonic Scalpel System - Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | BBT Medical, Surgsci Medical Ltd., Lepu Medical, Johnson & Johnson Ethicon, Stryker, Innolcon, Ezisurg Medical, Medtronic, Olympus, Yuesen Med, Sonicmed, Hocermed (Tianjin) Medical Technology Co., Ltd, Mediserve, Misonix Inc, Hunan Handlike Minimally Invasive Surgery Co., Ltd, Hangzhou Rex Medical Instrument Co., Ltd., Sound Reach, Wuhan Banbiantian Medical Technology Development Co., Ltd. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |