What is Stereotactic Surgical Planning Software - Global Market?

Stereotactic surgical planning software is a specialized tool used in the medical field to assist surgeons in planning and executing precise surgical procedures. This software is particularly valuable in neurosurgery, where accuracy is crucial due to the complexity and sensitivity of the brain and surrounding structures. The global market for this software is expanding as healthcare providers increasingly recognize its benefits in improving surgical outcomes. By integrating advanced imaging techniques, such as MRI and CT scans, the software allows surgeons to create detailed 3D models of a patient's anatomy. This enables them to plan the surgical approach with high precision, minimizing risks and improving the chances of success. The software also facilitates real-time navigation during surgery, providing surgeons with critical information to make informed decisions. As technology continues to advance, the demand for stereotactic surgical planning software is expected to grow, driven by the need for safer and more effective surgical interventions. The global market is witnessing increased adoption across various regions, with healthcare institutions investing in this technology to enhance their surgical capabilities and improve patient outcomes.

Biopsy Planning, Deep Brain Stimulation (DBS), Others in the Stereotactic Surgical Planning Software - Global Market:

Stereotactic surgical planning software plays a crucial role in various medical procedures, including biopsy planning, deep brain stimulation (DBS), and other complex surgeries. In biopsy planning, the software aids in accurately targeting specific areas within the body to obtain tissue samples for diagnostic purposes. By utilizing detailed imaging data, the software helps surgeons identify the precise location of the biopsy site, reducing the risk of complications and ensuring that the sample is representative of the area of interest. This precision is particularly important in cases where the target area is small or located near critical structures. In the context of deep brain stimulation (DBS), stereotactic surgical planning software is instrumental in guiding the placement of electrodes within the brain. DBS is a treatment used for neurological conditions such as Parkinson's disease, essential tremor, and dystonia. The software assists in mapping the brain's intricate structures, allowing surgeons to determine the optimal trajectory for electrode insertion. This precision is vital to maximize the therapeutic benefits of DBS while minimizing potential side effects. Additionally, the software's ability to integrate with real-time imaging and navigation systems enhances the accuracy of electrode placement, contributing to improved patient outcomes. Beyond biopsy planning and DBS, stereotactic surgical planning software is utilized in a range of other procedures, including tumor resections, epilepsy surgery, and functional neurosurgery. In tumor resections, the software aids in delineating the boundaries of the tumor, helping surgeons achieve complete removal while preserving healthy tissue. This is particularly important in brain tumors, where preserving cognitive and motor functions is a priority. In epilepsy surgery, the software assists in identifying and targeting epileptogenic zones, enabling precise removal or disconnection of the affected areas. This can significantly reduce seizure frequency and improve the quality of life for patients with drug-resistant epilepsy. Functional neurosurgery, which encompasses procedures aimed at treating movement disorders and psychiatric conditions, also benefits from the precision offered by stereotactic surgical planning software. By accurately targeting specific brain regions, surgeons can achieve therapeutic effects while minimizing adverse outcomes. Overall, the versatility and precision of stereotactic surgical planning software make it an invaluable tool in modern medicine, contributing to safer and more effective surgical interventions across a wide range of applications.

Hospital, Ambulatory Surgery Center, Clinic in the Stereotactic Surgical Planning Software - Global Market:

The usage of stereotactic surgical planning software is prevalent in various healthcare settings, including hospitals, ambulatory surgery centers, and clinics. In hospitals, this software is an integral part of the neurosurgical department, where it is used to plan and execute complex brain surgeries. Hospitals often have access to advanced imaging technologies, such as MRI and CT scanners, which are essential for the software to create accurate 3D models of a patient's anatomy. The integration of these imaging modalities with the software allows neurosurgeons to plan surgical procedures with high precision, reducing the risk of complications and improving patient outcomes. In addition to neurosurgery, hospitals may also use stereotactic surgical planning software in other specialties, such as oncology and orthopedics, where precise surgical planning is critical. Ambulatory surgery centers, which focus on providing same-day surgical care, also benefit from the use of stereotactic surgical planning software. These centers often perform minimally invasive procedures that require precise targeting of specific areas within the body. The software's ability to integrate with real-time imaging and navigation systems enhances the accuracy of these procedures, allowing surgeons to achieve optimal results with minimal disruption to surrounding tissues. This precision is particularly important in ambulatory settings, where patients are expected to recover quickly and return home on the same day. By utilizing stereotactic surgical planning software, ambulatory surgery centers can offer high-quality care while minimizing the risk of complications and reducing recovery times. Clinics, particularly those specializing in neurology and neurosurgery, also utilize stereotactic surgical planning software to enhance their diagnostic and treatment capabilities. In a clinical setting, the software is often used for preoperative planning and consultation, allowing physicians to discuss surgical options with patients and provide detailed explanations of the planned procedure. This can help alleviate patient anxiety and improve understanding of the surgical process. Additionally, clinics may use the software to collaborate with other healthcare providers, sharing detailed surgical plans and imaging data to ensure continuity of care. Overall, the use of stereotactic surgical planning software across hospitals, ambulatory surgery centers, and clinics highlights its versatility and importance in modern healthcare. By enabling precise surgical planning and execution, the software contributes to improved patient outcomes and enhances the quality of care provided in various healthcare settings.

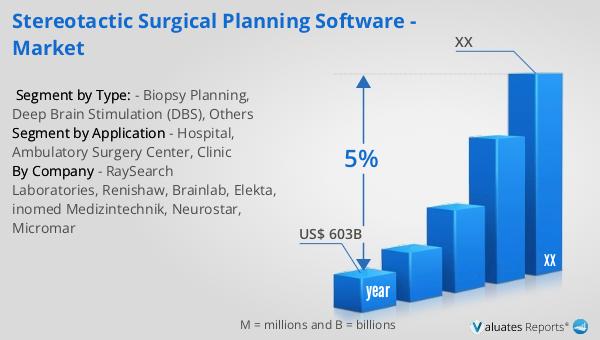

Stereotactic Surgical Planning Software - Global Market Outlook:

Based on our research, the global market for medical devices is projected to reach approximately $603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This growth is driven by several factors, including advancements in medical technology, increasing demand for minimally invasive procedures, and the rising prevalence of chronic diseases. As healthcare systems worldwide continue to evolve, there is a growing emphasis on improving patient outcomes and reducing healthcare costs. Medical devices, including stereotactic surgical planning software, play a crucial role in achieving these goals by enabling precise and efficient surgical interventions. The expanding global market reflects the increasing adoption of advanced medical technologies across various regions, with healthcare providers investing in innovative solutions to enhance their capabilities. As the market continues to grow, it is expected to create new opportunities for manufacturers and developers of medical devices, driving further innovation and development in the field. The projected growth of the medical device market underscores the importance of continued investment in research and development to meet the evolving needs of healthcare providers and patients. By staying at the forefront of technological advancements, companies can capitalize on the growing demand for innovative medical solutions and contribute to the ongoing transformation of the healthcare industry.

| Report Metric | Details |

| Report Name | Stereotactic Surgical Planning Software - Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | RaySearch Laboratories, Renishaw, Brainlab, Elekta, inomed Medizintechnik, Neurostar, Micromar |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |