What is Liquid Crystal Mixtures - Global Market?

Liquid crystal mixtures are a fascinating component of the global market, primarily because they are the backbone of many display technologies we use today. These mixtures are composed of liquid crystals, which are substances that exhibit properties between those of conventional liquids and solid crystals. They are particularly valued for their ability to modulate light, making them essential in the creation of displays for a wide range of electronic devices. The global market for liquid crystal mixtures is driven by the increasing demand for high-quality displays in consumer electronics, automotive displays, and medical devices. As technology advances, the need for more efficient, brighter, and energy-saving displays grows, pushing the market for liquid crystal mixtures forward. The versatility of these mixtures allows them to be tailored for specific applications, enhancing their appeal across various industries. This adaptability, combined with ongoing research and development, ensures that liquid crystal mixtures remain a critical component in the evolution of display technologies. As a result, the global market for these mixtures is poised for continued growth, driven by innovation and the ever-expanding demand for advanced display solutions.

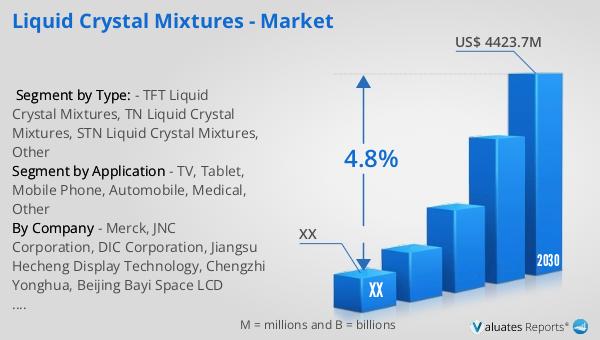

TFT Liquid Crystal Mixtures, TN Liquid Crystal Mixtures, STN Liquid Crystal Mixtures, Other in the Liquid Crystal Mixtures - Global Market:

TFT, TN, STN, and other types of liquid crystal mixtures each play a unique role in the global market, catering to different technological needs and applications. Thin-Film Transistor (TFT) liquid crystal mixtures are widely used in high-resolution displays, such as those found in smartphones, tablets, and computer monitors. TFT technology allows for precise control of each pixel, resulting in sharp images and vibrant colors. This makes TFT liquid crystal mixtures highly desirable in the consumer electronics market, where display quality is a key selling point. Twisted Nematic (TN) liquid crystal mixtures, on the other hand, are known for their fast response times and cost-effectiveness. They are commonly used in applications where speed is more critical than color accuracy, such as in gaming monitors and some types of industrial displays. TN technology is one of the oldest liquid crystal technologies, and while it may not offer the same color richness as TFT, its affordability and quick response make it a popular choice for budget-conscious consumers and specific industrial applications. Super Twisted Nematic (STN) liquid crystal mixtures offer a middle ground between TFT and TN technologies. They provide better color and viewing angles than TN displays, though not quite reaching the quality of TFT displays. STN technology is often used in devices where moderate display quality is sufficient, such as in calculators, older mobile phones, and some types of automotive displays. The "Other" category in liquid crystal mixtures includes a variety of specialized mixtures designed for niche applications. These can include mixtures used in advanced technologies like OLED displays, which require specific liquid crystal properties to function effectively. Each type of liquid crystal mixture has its own set of advantages and limitations, making them suitable for different applications based on the specific needs of the device or industry. The diversity in liquid crystal mixtures allows manufacturers to choose the most appropriate technology for their products, balancing factors such as cost, performance, and energy efficiency. As the global market for liquid crystal mixtures continues to evolve, we can expect to see further innovations and refinements in these technologies, driven by the ever-changing demands of consumers and industries alike.

TV, Tablet, Mobile Phone, Automobile, Medical, Other in the Liquid Crystal Mixtures - Global Market:

Liquid crystal mixtures are integral to a wide range of applications, particularly in the fields of television, tablets, mobile phones, automobiles, medical devices, and beyond. In the television industry, liquid crystal mixtures are used to produce LCD screens, which are known for their excellent picture quality and energy efficiency. These screens have largely replaced older technologies like CRTs, offering consumers a more immersive viewing experience with thinner, lighter, and more aesthetically pleasing designs. In tablets and mobile phones, liquid crystal mixtures are crucial for creating displays that are not only visually appealing but also responsive to touch. The demand for high-resolution screens in these devices has driven advancements in liquid crystal technology, enabling manufacturers to produce displays that offer vibrant colors, sharp images, and smooth touch interactions. In the automotive sector, liquid crystal mixtures are used in a variety of displays, from dashboard screens to infotainment systems. These displays provide drivers with critical information, such as navigation and vehicle diagnostics, in an easy-to-read format. The use of liquid crystal mixtures in automotive displays is expected to grow as vehicles become more technologically advanced, incorporating features like heads-up displays and digital instrument clusters. In the medical field, liquid crystal mixtures are used in a range of diagnostic and monitoring equipment. Their ability to provide clear, precise images makes them ideal for use in devices like ultrasound machines and patient monitors. The clarity and reliability of these displays are crucial in medical settings, where accurate information can be a matter of life and death. Beyond these specific applications, liquid crystal mixtures are also used in a variety of other industries, including aerospace, industrial equipment, and consumer electronics. Their versatility and adaptability make them a valuable component in any application where high-quality displays are required. As technology continues to advance, the use of liquid crystal mixtures is likely to expand into new areas, driven by the need for more efficient, high-performance display solutions.

Liquid Crystal Mixtures - Global Market Outlook:

The global market for liquid crystal mixtures was valued at approximately $3,189 million in 2023 and is projected to grow to around $4,423.7 million by 2030, reflecting a compound annual growth rate (CAGR) of 4.8% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for advanced display technologies across various industries. Hybrid LCD technology, which combines traditional liquid crystals with other materials or technologies, is one of the innovations driving this market expansion. By integrating different materials, hybrid LCDs can offer unique properties, such as improved brightness, contrast, and energy efficiency, making them highly attractive for both manufacturers and consumers. The ability to tailor these displays to specific applications further enhances their appeal, allowing for more customized and efficient solutions. As industries continue to seek out more advanced and versatile display technologies, the market for liquid crystal mixtures is expected to see sustained growth, driven by ongoing innovation and the ever-evolving needs of consumers and businesses alike.

| Report Metric | Details |

| Report Name | Liquid Crystal Mixtures - Market |

| Forecasted market size in 2030 | US$ 4423.7 million |

| CAGR | 4.8% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Merck, JNC Corporation, DIC Corporation, Jiangsu Hecheng Display Technology, Chengzhi Yonghua, Beijing Bayi Space LCD Technology, Yantai Xianhua Chem-Tech |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |