What is Fully Rugged Tablets - Global Market?

Fully rugged tablets are specialized devices designed to withstand harsh environments and demanding conditions. These tablets are built with robust materials and advanced technology to ensure durability, making them ideal for industries where standard tablets would fail. The global market for fully rugged tablets is driven by the need for reliable, portable computing solutions in sectors such as military, construction, and public safety. These tablets are resistant to water, dust, extreme temperatures, and shocks, which makes them suitable for outdoor and industrial use. They often come with features like sunlight-readable screens, long battery life, and enhanced connectivity options. As industries continue to digitize their operations, the demand for fully rugged tablets is expected to grow, providing a reliable solution for field workers who require durable and efficient devices. The market is characterized by a variety of products catering to different needs, from lightweight models for easy portability to more robust versions for heavy-duty applications. With advancements in technology, these tablets are becoming more powerful and versatile, further expanding their use across various sectors. The global market for fully rugged tablets is poised for growth as more industries recognize the benefits of these durable devices.

Windows, Android, Others in the Fully Rugged Tablets - Global Market:

Fully rugged tablets are available with different operating systems, primarily Windows, Android, and others, each offering unique advantages and features tailored to specific industry needs. Windows-based fully rugged tablets are popular in sectors that require compatibility with existing enterprise software and systems. These tablets offer a familiar interface and robust security features, making them suitable for industries like manufacturing, government, and military. Windows tablets are often preferred for their ability to run complex applications and integrate seamlessly with other Windows-based devices and networks. They provide a comprehensive solution for professionals who need powerful computing capabilities in challenging environments. On the other hand, Android-based fully rugged tablets are favored for their flexibility and user-friendly interface. These tablets are widely used in industries such as retail, transportation, and public safety, where ease of use and quick access to applications are crucial. Android tablets offer a wide range of apps and customization options, allowing businesses to tailor the devices to their specific needs. They are also known for their cost-effectiveness, making them an attractive option for companies looking to equip large teams with durable devices. Additionally, the open-source nature of Android allows for greater innovation and adaptability, enabling businesses to develop custom solutions for their operations. Other operating systems, though less common, are also present in the fully rugged tablet market. These may include proprietary systems developed by manufacturers to meet specific industry requirements. Such tablets are often used in niche markets where specialized software and hardware integration are necessary. Regardless of the operating system, fully rugged tablets are designed to provide reliable performance in extreme conditions, ensuring that professionals can carry out their tasks efficiently and effectively. The choice of operating system depends largely on the specific needs of the industry and the applications required. As technology continues to evolve, the capabilities of fully rugged tablets are expected to expand, offering even more options for businesses seeking durable and versatile computing solutions.

Energy, Manufacturing, Construction, Transportation & Distribution, Public Safety, Retail, Medical, Government, Military in the Fully Rugged Tablets - Global Market:

Fully rugged tablets are utilized across various industries due to their durability and reliability in harsh environments. In the energy sector, these tablets are essential for field workers who need to access and input data in remote locations. They provide real-time information and communication capabilities, enabling efficient monitoring and management of energy resources. In manufacturing, fully rugged tablets streamline operations by allowing workers to access production data and control systems on the go. They enhance productivity by providing a mobile solution for quality control, inventory management, and equipment maintenance. The construction industry benefits from these tablets as they enable project managers and workers to access blueprints, track progress, and communicate effectively on-site. Their rugged design ensures they can withstand the dust and debris commonly found in construction environments. In transportation and distribution, fully rugged tablets facilitate logistics management by providing real-time tracking and communication capabilities. They help optimize routes, manage deliveries, and ensure timely updates, improving overall efficiency. Public safety professionals rely on these tablets for their robust communication features and ability to access critical information in emergency situations. They are used by police, firefighters, and emergency medical services to coordinate responses and ensure public safety. In the retail sector, fully rugged tablets enhance customer service by providing sales associates with access to inventory data and customer information. They enable seamless transactions and improve the overall shopping experience. The medical industry uses these tablets for patient data management and communication between healthcare professionals. Their durability ensures they can withstand frequent cleaning and disinfection, making them suitable for hospital environments. Government agencies utilize fully rugged tablets for fieldwork, data collection, and communication. They provide a secure and reliable solution for various government operations. In the military, these tablets are crucial for mission-critical operations, offering secure communication and data access in challenging environments. Their rugged design ensures they can withstand the rigors of military use, providing reliable performance in the field. Overall, fully rugged tablets are indispensable tools across these industries, offering durability, reliability, and advanced features to meet the demands of challenging environments.

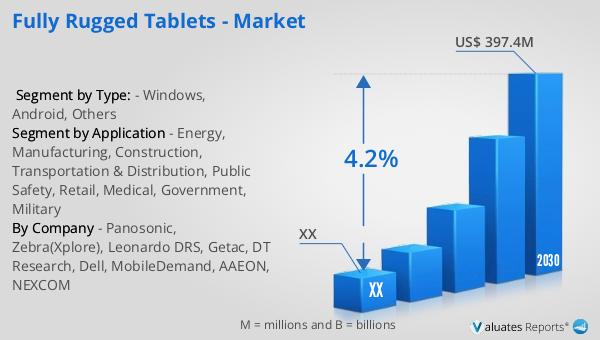

Fully Rugged Tablets - Global Market Outlook:

The global market for fully rugged tablets was valued at approximately $299.2 million in 2023. This market is projected to grow, reaching an estimated size of $397.4 million by 2030, with a compound annual growth rate (CAGR) of 4.2% during the forecast period from 2024 to 2030. This growth reflects the increasing demand for durable and reliable computing solutions across various industries. In North America, the market for fully rugged tablets was valued at a significant amount in 2023, with expectations of continued growth through 2030. The CAGR for this region during the forecast period is indicative of the strong demand for these devices in industries such as military, public safety, and construction. The robust growth in the global and North American markets underscores the importance of fully rugged tablets in providing reliable performance in challenging environments. As industries continue to digitize their operations and require durable devices for fieldwork, the demand for fully rugged tablets is expected to rise. These tablets offer a unique combination of durability, advanced features, and compatibility with industry-specific applications, making them an essential tool for professionals working in harsh conditions. The market outlook for fully rugged tablets is positive, with steady growth anticipated as more industries recognize the benefits of these durable devices.

| Report Metric | Details |

| Report Name | Fully Rugged Tablets - Market |

| Forecasted market size in 2030 | US$ 397.4 million |

| CAGR | 4.2% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Panosonic, Zebra(Xplore), Leonardo DRS, Getac, DT Research, Dell, MobileDemand, AAEON, NEXCOM |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |