What is Global Healthcare Head Mounted Display Market?

The Global Healthcare Head Mounted Display Market refers to the sector that focuses on the development and application of head-mounted display (HMD) technology within the healthcare industry. These devices are essentially wearable displays that can be mounted on the head, allowing users to view digital content directly in their line of sight. In healthcare, HMDs are used for various purposes, including enhancing surgical precision, providing immersive training experiences, and improving patient care. The market is driven by advancements in technology, increasing demand for minimally invasive surgeries, and the growing need for efficient training tools for healthcare professionals. As the healthcare industry continues to embrace digital transformation, the adoption of HMDs is expected to rise, offering new opportunities for innovation and improved patient outcomes. The market is characterized by a diverse range of products, including helmet-mounted displays and eyewear displays, each catering to specific needs within the healthcare sector. With ongoing research and development, the Global Healthcare Head Mounted Display Market is poised for significant growth, driven by the increasing integration of augmented reality (AR) and virtual reality (VR) technologies in medical applications.

Helmet Mounted Display, Eye Wear Display in the Global Healthcare Head Mounted Display Market:

Helmet Mounted Displays (HMDs) and Eye Wear Displays are two prominent categories within the Global Healthcare Head Mounted Display Market, each offering unique features and benefits tailored to specific healthcare applications. Helmet Mounted Displays are typically more robust and are designed to provide a comprehensive visual experience, often used in environments where full immersion and hands-free operation are crucial. These displays are particularly beneficial in surgical settings, where surgeons can access real-time data, 3D models, and patient information without diverting their attention from the procedure. The immersive nature of helmet-mounted displays allows for enhanced precision and accuracy, reducing the risk of errors and improving surgical outcomes. Additionally, these displays can be integrated with other medical devices and systems, providing a seamless flow of information and enhancing the overall efficiency of surgical procedures. On the other hand, Eye Wear Displays are more lightweight and versatile, resembling traditional eyeglasses or goggles. These displays are designed for ease of use and comfort, making them ideal for applications that require mobility and flexibility. In the healthcare sector, eyewear displays are often used for training and education purposes, allowing medical students and professionals to engage in realistic simulations and interactive learning experiences. By overlaying digital information onto the real world, eyewear displays enable users to visualize complex medical concepts and procedures, enhancing their understanding and retention of knowledge. Furthermore, these displays can be used in telemedicine, enabling remote consultations and diagnostics by providing healthcare professionals with real-time access to patient data and medical records. The integration of augmented reality (AR) and virtual reality (VR) technologies in eyewear displays further enhances their capabilities, allowing for more immersive and interactive experiences. As the demand for innovative and efficient healthcare solutions continues to grow, both helmet-mounted and eyewear displays are expected to play a significant role in transforming the healthcare landscape, offering new possibilities for patient care, medical training, and surgical precision.

Surgery, Training, Others in the Global Healthcare Head Mounted Display Market:

The usage of Global Healthcare Head Mounted Display Market in areas such as Surgery, Training, and Others is revolutionizing the way healthcare services are delivered and experienced. In the realm of surgery, head-mounted displays are proving to be invaluable tools for surgeons, providing them with real-time access to critical information and enhancing their ability to perform complex procedures with precision. By overlaying digital images and data onto the surgical field, these displays allow surgeons to visualize anatomical structures, monitor vital signs, and access patient records without having to look away from the operative site. This hands-free access to information not only improves surgical accuracy but also reduces the risk of errors and complications, ultimately leading to better patient outcomes. In addition to surgery, head-mounted displays are also transforming the way healthcare professionals are trained. Traditional training methods often rely on textbooks and static models, which can be limiting in terms of providing a realistic and immersive learning experience. With head-mounted displays, medical students and professionals can engage in interactive simulations and virtual reality scenarios that mimic real-life medical situations. This hands-on approach to learning allows trainees to practice and refine their skills in a safe and controlled environment, enhancing their confidence and competence. Furthermore, head-mounted displays can facilitate remote training and collaboration, enabling healthcare professionals from different locations to connect and learn from each other in real-time. Beyond surgery and training, head-mounted displays are finding applications in various other areas of healthcare. For instance, they are being used in telemedicine to enable remote consultations and diagnostics, providing healthcare professionals with the ability to assess and treat patients from a distance. This is particularly beneficial in rural or underserved areas where access to healthcare services may be limited. Additionally, head-mounted displays are being utilized in patient education, allowing patients to visualize their medical conditions and treatment plans in a more engaging and understandable way. By providing patients with a clearer understanding of their health, these displays can improve patient compliance and satisfaction. As the Global Healthcare Head Mounted Display Market continues to evolve, the potential applications and benefits of this technology are expected to expand, offering new opportunities for innovation and improvement in healthcare delivery.

Global Healthcare Head Mounted Display Market Outlook:

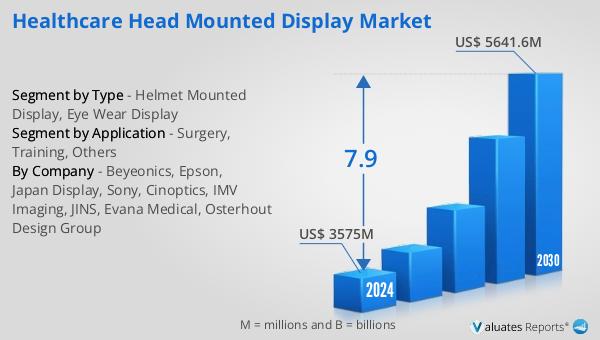

The outlook for the Global Healthcare Head Mounted Display Market is promising, with projections indicating significant growth in the coming years. The market is expected to expand from approximately $3,575 million in 2024 to around $5,641.6 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 7.9% during the forecast period. This growth is driven by the increasing adoption of advanced technologies in healthcare, the rising demand for minimally invasive surgeries, and the need for efficient training tools for healthcare professionals. In parallel, the broader medical devices market is also experiencing growth, with an estimated value of $603 billion in 2023 and a projected CAGR of 5% over the next six years. This indicates a growing recognition of the importance of technological innovation in improving healthcare outcomes and efficiency. As healthcare providers continue to seek ways to enhance patient care and streamline operations, the demand for head-mounted displays and other advanced medical devices is expected to rise. The integration of augmented reality (AR) and virtual reality (VR) technologies in these devices further enhances their capabilities, offering new possibilities for surgical precision, medical training, and patient engagement. As a result, the Global Healthcare Head Mounted Display Market is poised for continued growth and innovation, driven by the ongoing digital transformation of the healthcare industry.

| Report Metric | Details |

| Report Name | Healthcare Head Mounted Display Market |

| Accounted market size in 2024 | US$ 3575 million |

| Forecasted market size in 2030 | US$ 5641.6 million |

| CAGR | 7.9 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Segment by Region |

|

| By Company | Beyeonics, Epson, Japan Display, Sony, Cinoptics, IMV Imaging, JINS, Evana Medical, Osterhout Design Group |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |