What is Global Augmented Reality Surgical System Market?

The Global Augmented Reality Surgical System Market is a rapidly evolving sector within the medical field that leverages augmented reality (AR) technology to enhance surgical procedures. This market focuses on integrating AR systems into surgical environments to provide surgeons with real-time, 3D visualizations of patient anatomy, which can be overlaid onto the actual surgical site. These systems aim to improve precision, reduce the risk of errors, and enhance overall surgical outcomes. By offering detailed, interactive views of the surgical area, AR systems assist surgeons in navigating complex anatomical structures, planning surgical interventions, and making informed decisions during operations. The market encompasses a wide range of applications, including neurosurgery, spinal surgery, orthopedic surgery, otolaryngology surgery, and other specialized fields. As the technology continues to advance, the Global Augmented Reality Surgical System Market is expected to play a crucial role in transforming surgical practices, making procedures safer, more efficient, and less invasive for patients.

Video Perspective (VST), Optical Perspective (OST) in the Global Augmented Reality Surgical System Market:

Video Perspective (VST) and Optical Perspective (OST) are two key technologies within the Global Augmented Reality Surgical System Market that offer distinct approaches to enhancing surgical visualization. VST-based systems utilize video cameras to capture real-time images of the surgical field, which are then processed and displayed on a screen or through a head-mounted display (HMD). This allows surgeons to view the augmented images superimposed onto the live video feed, providing a comprehensive view of the surgical site. VST systems are particularly beneficial in minimally invasive surgeries, where direct visualization of the surgical area is limited. By integrating AR overlays, VST systems help surgeons navigate through small incisions, identify critical structures, and perform precise maneuvers with greater confidence. On the other hand, OST-based systems use optical see-through displays, such as transparent HMDs or smart glasses, to project AR content directly onto the surgeon's field of view. This approach allows surgeons to see both the real-world environment and the augmented information simultaneously, without the need for an intermediary screen. OST systems offer a more immersive experience, enabling surgeons to maintain situational awareness and spatial orientation while accessing critical data. These systems are particularly useful in complex surgeries, where real-time guidance and accurate visualization are essential for successful outcomes. Both VST and OST technologies have their unique advantages and are being continuously refined to meet the specific needs of different surgical specialties. As the Global Augmented Reality Surgical System Market continues to grow, the adoption of VST and OST technologies is expected to increase, driving further advancements in surgical precision, safety, and efficiency.

Neurosurgery, Spinal Surgery, Orthopaedic Surgery, Otolaryngology Surgery, Other in the Global Augmented Reality Surgical System Market:

The usage of Global Augmented Reality Surgical System Market in various surgical fields is transforming the way surgeries are performed, offering significant benefits across different specialties. In neurosurgery, AR systems provide detailed, 3D visualizations of the brain, allowing surgeons to plan and execute complex procedures with greater accuracy. By overlaying critical information, such as tumor boundaries and blood vessels, onto the surgical site, AR helps neurosurgeons navigate through delicate brain tissues, reducing the risk of damage to healthy structures. In spinal surgery, AR systems assist in the precise placement of screws and implants, enhancing the accuracy of spinal alignments and reducing the likelihood of complications. The ability to visualize the spine in 3D and overlay surgical plans onto the patient's anatomy enables surgeons to perform minimally invasive procedures with improved outcomes. Orthopedic surgery also benefits from AR technology, as it provides real-time guidance for joint replacements, fracture repairs, and other orthopedic interventions. By offering detailed views of bone structures and implant positions, AR systems help orthopedic surgeons achieve optimal alignment and fit, leading to better patient outcomes and faster recovery times. In otolaryngology surgery, AR systems enhance the visualization of complex anatomical structures within the ear, nose, and throat, aiding surgeons in performing delicate procedures with greater precision. The ability to overlay CT or MRI scans onto the surgical field allows for more accurate navigation and reduces the risk of complications. Additionally, AR technology is being explored in other surgical fields, such as cardiovascular surgery, where it can assist in the precise placement of stents and other devices, and in plastic and reconstructive surgery, where it can aid in the planning and execution of complex reconstructions. Overall, the integration of AR systems into various surgical specialties is revolutionizing the way surgeries are performed, making them safer, more efficient, and less invasive for patients.

Global Augmented Reality Surgical System Market Outlook:

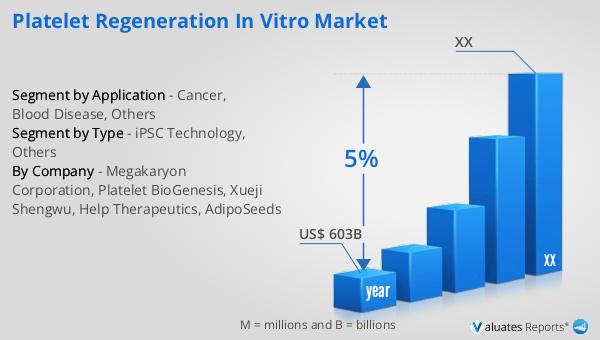

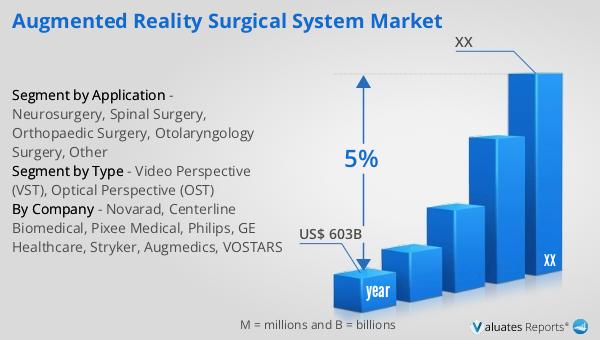

Based on our research, the global market for medical devices is projected to reach approximately US$ 603 billion by the year 2023, with an anticipated growth rate of 5% annually over the next six years. This growth is driven by advancements in medical technology, increasing demand for innovative healthcare solutions, and the rising prevalence of chronic diseases. The medical device market encompasses a wide range of products, including diagnostic equipment, surgical instruments, and therapeutic devices, all of which play a crucial role in improving patient care and outcomes. As the healthcare industry continues to evolve, the demand for advanced medical devices is expected to rise, driven by factors such as an aging population, increasing healthcare expenditure, and the growing adoption of minimally invasive procedures. The integration of cutting-edge technologies, such as augmented reality, artificial intelligence, and robotics, into medical devices is further propelling market growth, offering new possibilities for diagnosis, treatment, and patient management. With ongoing research and development efforts, the medical device market is poised to witness significant advancements, ultimately enhancing the quality of healthcare services and improving patient outcomes worldwide.

| Report Metric | Details |

| Report Name | Augmented Reality Surgical System Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Novarad, Centerline Biomedical, Pixee Medical, Philips, GE Healthcare, Stryker, Augmedics, VOSTARS |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |