What is Global Amalgam Separator Filter System Market?

The Global Amalgam Separator Filter System Market is a specialized segment within the broader dental and medical equipment industry. Amalgam separators are devices used to capture and remove amalgam particles from dental wastewater, preventing them from entering the sewage system. These particles often contain mercury, which is harmful to the environment and human health. The market for these systems is driven by stringent environmental regulations and the increasing awareness of the need for proper waste management in dental practices. The systems are designed to be efficient, easy to install, and compliant with various international standards. They are widely adopted in dental clinics, hospitals, and other healthcare facilities to ensure that mercury and other hazardous materials are effectively filtered out. The market is characterized by a range of products that vary in terms of capacity, efficiency, and cost, catering to different needs and budgets. As environmental concerns continue to rise, the demand for amalgam separator filter systems is expected to grow, making it a crucial component of modern dental and medical waste management practices.

Sedimentation Type, Centrifugal Type, Other in the Global Amalgam Separator Filter System Market:

The Global Amalgam Separator Filter System Market can be categorized based on the type of separation technology used, namely Sedimentation Type, Centrifugal Type, and Other types. Sedimentation Type amalgam separators work on the principle of gravity. They allow the heavier amalgam particles to settle at the bottom of a container while the cleaner water flows out from the top. This type is generally more straightforward and cost-effective, making it popular among smaller dental practices. However, it may require more frequent maintenance and cleaning to ensure optimal performance. On the other hand, Centrifugal Type amalgam separators use centrifugal force to separate amalgam particles from the wastewater. These systems are more efficient and can handle larger volumes of wastewater, making them suitable for larger dental clinics and hospitals. The centrifugal force pushes the heavier amalgam particles to the outer edges of a spinning chamber, where they are collected and removed. This type of separator is generally more expensive but offers higher efficiency and lower maintenance requirements. Other types of amalgam separators may include advanced filtration systems that use a combination of mechanical and chemical processes to remove amalgam particles. These systems are often designed for specialized applications and may offer the highest levels of efficiency and compliance with environmental regulations. They can be customized to meet the specific needs of a dental practice or healthcare facility, providing a tailored solution for amalgam waste management. Each type of amalgam separator has its own set of advantages and disadvantages, and the choice of system often depends on factors such as the size of the practice, the volume of wastewater generated, and budget constraints. As technology continues to evolve, new and more efficient types of amalgam separators are likely to emerge, further enhancing the capabilities of dental and medical waste management systems.

Hospital, Dental Clinic, Others in the Global Amalgam Separator Filter System Market:

The usage of Global Amalgam Separator Filter Systems is widespread across various healthcare settings, including hospitals, dental clinics, and other facilities. In hospitals, these systems are crucial for managing the waste generated by dental departments. Hospitals often have high patient turnover and generate significant amounts of dental wastewater containing amalgam particles. The use of amalgam separators ensures that this waste is effectively filtered, preventing harmful mercury from entering the sewage system and posing a risk to the environment and public health. Dental clinics are perhaps the most common users of amalgam separator filter systems. These clinics generate a substantial amount of amalgam waste due to the frequent use of dental amalgam in fillings and other procedures. By installing amalgam separators, dental clinics can comply with environmental regulations and demonstrate their commitment to sustainable practices. The systems help in maintaining a clean and safe working environment for dental professionals and their patients. Other facilities that may use amalgam separator filter systems include dental schools, research institutions, and specialized dental laboratories. These settings also generate dental wastewater that needs to be properly managed to prevent environmental contamination. In dental schools, for example, students perform numerous procedures that produce amalgam waste, making the use of separators essential for maintaining compliance with environmental standards. Research institutions and dental laboratories also benefit from these systems as they often handle large volumes of dental materials and need to ensure that their waste management practices are up to par. Overall, the use of amalgam separator filter systems is integral to modern dental and medical waste management. These systems not only help in complying with stringent environmental regulations but also contribute to the overall sustainability efforts of healthcare facilities. By effectively capturing and removing harmful amalgam particles, these systems play a vital role in protecting the environment and public health.

Global Amalgam Separator Filter System Market Outlook:

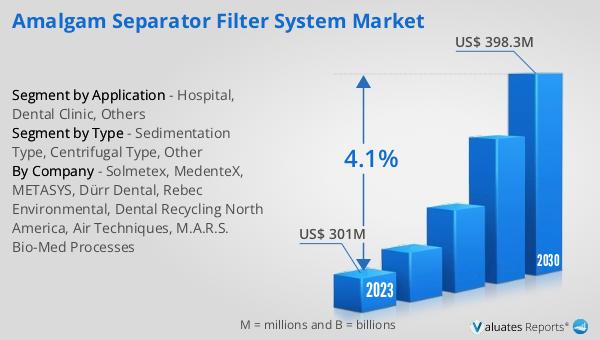

The global Amalgam Separator Filter System market was valued at US$ 301 million in 2023 and is anticipated to reach US$ 398.3 million by 2030, witnessing a CAGR of 4.1% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory driven by increasing environmental awareness and stringent regulations regarding dental waste management. The rising adoption of amalgam separators in dental clinics, hospitals, and other healthcare facilities is a key factor contributing to this growth. As more healthcare providers recognize the importance of proper waste management, the demand for efficient and reliable amalgam separator filter systems is expected to rise. The market is also likely to benefit from technological advancements that enhance the efficiency and ease of use of these systems. With a growing emphasis on sustainability and environmental protection, the global Amalgam Separator Filter System market is poised for significant expansion in the coming years.

| Report Metric | Details |

| Report Name | Amalgam Separator Filter System Market |

| Accounted market size in 2023 | US$ 301 million |

| Forecasted market size in 2030 | US$ 398.3 million |

| CAGR | 4.1% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Solmetex, MedenteX, METASYS, Dürr Dental, Rebec Environmental, Dental Recycling North America, Air Techniques, M.A.R.S. Bio-Med Processes |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |