What is Global Wireless Fast Charging Chip Market?

The Global Wireless Fast Charging Chip Market is a rapidly expanding sector within the technology industry, focusing on the development and distribution of chips that enable fast charging capabilities for a variety of devices without the need for physical connectors or cables. Essentially, these chips are the heart of wireless charging systems, allowing electrical energy to be transferred from a power source to a device battery, enhancing convenience and reducing wear and tear on physical charging ports. As of 2023, the market has been valued at a significant figure, reflecting its growing importance in our increasingly wireless world. These chips are not just about speeding up the charging process; they are also about making it more efficient and adaptable to a range of devices, from smartphones to laptops and beyond. The technology behind these chips is constantly evolving, driven by the demand for faster, more efficient charging solutions that can keep up with the high energy consumption of modern electronic devices. This market's growth is propelled by the widespread adoption of wireless charging in public spaces, homes, and offices, alongside the integration of such capabilities in newer vehicle models, indicating a bright future for this technology.

Below 30W, 30-60W, 60-120W, Above 120W in the Global Wireless Fast Charging Chip Market:

The Global Wireless Fast Charging Chip Market is segmented based on the power output of the chips, which includes Below 30W, 30-60W, 60-120W, and Above 120W categories. Each segment caters to different devices and charging needs, reflecting the diverse applications of these chips. The Below 30W chips are typically used in smartphones and other small devices that require relatively low power for charging. This segment is quite popular due to the vast number of smartphones and similar devices in use worldwide. Moving up, the 30-60W chips are designed for devices that need a bit more power, like tablets and smaller laptops, providing a balance between charging speed and energy efficiency. The 60-120W segment is where we start to see chips capable of handling the needs of larger laptops, gaming devices, and other high-power electronics, offering faster charging times without compromising the device's safety or battery health. Finally, the Above 120W chips are at the cutting edge of this technology, designed for the most demanding applications, including industrial tools and some electric vehicles, pushing the boundaries of what wireless charging can achieve. Across these segments, the market is driven by the push for greater convenience, the elimination of wires, and the desire for faster charging times, reflecting the evolving needs and expectations of consumers and professionals alike.

Smart Phone, Laptop, Electrical Tools, IoT Devices, Others in the Global Wireless Fast Charging Chip Market:

The usage of the Global Wireless Fast Charging Chip Market spans across various areas, including Smart Phones, Laptops, Electrical Tools, IoT Devices, and Others, showcasing the versatility and widespread application of this technology. In smartphones, these chips have become almost a standard feature, with consumers expecting quick and convenient charging solutions that keep their devices powered throughout the day without the hassle of cables. Laptops, too, are beginning to benefit from wireless fast charging, offering users the freedom to charge their devices in cafes, libraries, or offices without needing to carry a charger everywhere. Electrical tools, including drills, saws, and other handheld devices, are also seeing the integration of these chips, reducing downtime on job sites and improving efficiency by allowing for quick power boosts without the need for cumbersome cord management. IoT devices, which are becoming increasingly prevalent in both homes and industries, rely on efficient, wireless charging to remain operational without constant maintenance, making these chips crucial for the scalability of smart technologies. The 'Others' category encompasses a broad range of devices, including but not limited to wearable tech, medical devices, and automotive applications, indicating the potential for wireless fast charging to revolutionize how we power our electronic devices across all facets of life.

Global Wireless Fast Charging Chip Market Outlook:

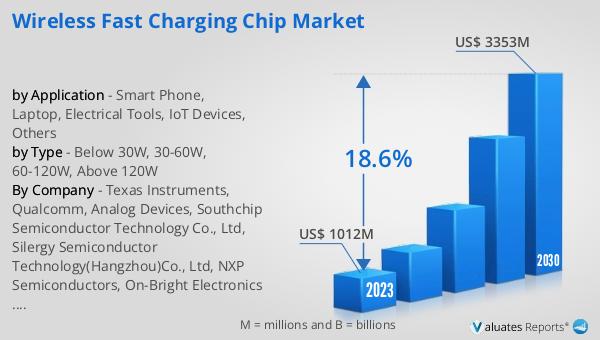

The market outlook for the Global Wireless Fast Charging Chip Market presents a promising future, with its valuation in 2023 standing at approximately $1012 million. This figure is expected to soar to around $3353 million by the year 2030, marking a Compound Annual Growth Rate (CAGR) of 18.6% throughout the forecast period from 2024 to 2030. This significant growth trajectory underscores the increasing adoption and integration of wireless fast charging technologies across a myriad of sectors, driven by consumer demand for more efficient, convenient, and advanced charging solutions. The escalation in market value reflects the technological advancements within the sector, as well as the expanding application range of these chips, from personal electronics to industrial tools and beyond. As the world continues to embrace wireless technologies and seeks to minimize the reliance on physical connectors and cables, the Global Wireless Fast Charging Chip Market is poised for substantial growth, highlighting its critical role in the evolution of modern electronic devices and charging infrastructures.

| Report Metric | Details |

| Report Name | Wireless Fast Charging Chip Market |

| Accounted market size in 2023 | US$ 1012 million |

| Forecasted market size in 2030 | US$ 3353 million |

| CAGR | 18.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Texas Instruments, Qualcomm, Analog Devices, Southchip Semiconductor Technology Co., Ltd, Silergy Semiconductor Technology(Hangzhou)Co., Ltd, NXP Semiconductors, On-Bright Electronics Co., Ltd, MPS, Zhuhai Zhirong Technology Co., Ltd., SG Micro Corp (SGMICRO), Cirrus Logic, Shenzhen Injoinic Technology Co.,Ltd, Wuxi Chipown Micro-electronics Limited, Halo Microelectronics Co., Ltd, Joulwatt Electronic(Hangzhou)Co., Ltd., Shanghai Awinic Technology Co., Ltd., NuVolta Technologies, Rockchip Electronics Co., Ltd, STMicroelectronics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |