What is Global Cooled Thermal Infrared Imagers Market?

The Global Cooled Thermal Infrared Imagers Market is a specialized segment within the broader thermal imaging industry, focusing on devices that utilize cooled infrared detectors to capture thermal images. These imagers are designed to detect infrared radiation, which is emitted by all objects based on their temperature, and convert it into a visible image. The "cooled" aspect refers to the use of cryogenic cooling systems that enhance the sensitivity and resolution of the detectors, allowing them to capture finer details and detect minute temperature differences. This makes them particularly valuable in applications requiring high precision and accuracy. The market for these devices is driven by their extensive use in various sectors, including military and defense, where they are employed for surveillance and target acquisition, as well as in industrial settings for monitoring equipment and processes. Additionally, advancements in technology have led to the development of more compact and efficient cooled thermal imagers, broadening their applicability and appeal across different industries. As a result, the Global Cooled Thermal Infrared Imagers Market is poised for significant growth, driven by increasing demand for high-performance thermal imaging solutions.

Vanadium Oxide (VOx), Amorphous Silicon (A-Si) in the Global Cooled Thermal Infrared Imagers Market:

Vanadium Oxide (VOx) and Amorphous Silicon (A-Si) are two prominent materials used in the manufacturing of detectors for thermal infrared imagers, each offering distinct advantages and characteristics. Vanadium Oxide (VOx) is widely recognized for its high sensitivity and excellent thermal stability, making it a preferred choice for applications requiring precise temperature measurements. VOx detectors operate by changing their electrical resistance in response to temperature variations, allowing them to produce detailed thermal images. This material is particularly favored in military and defense applications, where accuracy and reliability are paramount. The ability of VOx detectors to operate effectively in a wide range of environmental conditions further enhances their suitability for demanding applications. On the other hand, Amorphous Silicon (A-Si) is known for its cost-effectiveness and ease of integration into various systems. A-Si detectors are typically used in applications where cost is a significant consideration, such as in consumer electronics and automotive industries. While they may not offer the same level of sensitivity as VOx detectors, A-Si detectors provide a viable solution for applications where moderate performance is acceptable. The choice between VOx and A-Si often depends on the specific requirements of the application, including factors such as budget, performance needs, and environmental conditions. In the context of the Global Cooled Thermal Infrared Imagers Market, both VOx and A-Si play crucial roles in meeting the diverse needs of different industries. The ongoing advancements in material science and detector technology continue to enhance the performance and capabilities of both VOx and A-Si detectors, contributing to the growth and evolution of the market. As industries increasingly recognize the value of thermal imaging technology, the demand for high-quality detectors, whether based on VOx or A-Si, is expected to rise. This demand is further fueled by the expanding range of applications for thermal imagers, from traditional uses in military and defense to emerging opportunities in smart home technology and medical diagnostics. The versatility and adaptability of VOx and A-Si detectors ensure that they remain integral components of the Global Cooled Thermal Infrared Imagers Market, catering to the diverse and evolving needs of modern industries.

Military and Defense, Automotive, Smart Home, Medical, Others in the Global Cooled Thermal Infrared Imagers Market:

The Global Cooled Thermal Infrared Imagers Market finds extensive usage across various sectors, each benefiting from the unique capabilities of thermal imaging technology. In the military and defense sector, cooled thermal infrared imagers are indispensable tools for surveillance, reconnaissance, and target acquisition. Their ability to detect heat signatures in complete darkness or through smoke and fog provides a tactical advantage, enabling military personnel to operate effectively in challenging environments. These imagers are also used in border security and search and rescue operations, where their high sensitivity and resolution are critical for identifying threats or locating individuals in distress. In the automotive industry, cooled thermal infrared imagers are increasingly being integrated into advanced driver-assistance systems (ADAS) to enhance vehicle safety. They enable the detection of pedestrians, animals, and other vehicles in low-light conditions, reducing the risk of accidents. As the automotive industry moves towards autonomous driving, the demand for reliable and accurate thermal imaging solutions is expected to grow. In the realm of smart home technology, thermal imagers are used for energy efficiency and security purposes. They can identify areas of heat loss in a home, allowing homeowners to make informed decisions about insulation and energy usage. Additionally, thermal imagers can enhance home security systems by detecting intruders based on their heat signatures, even in complete darkness. The medical field also benefits from the capabilities of cooled thermal infrared imagers, particularly in diagnostics and patient monitoring. These imagers can detect subtle temperature changes in the human body, aiding in the early detection of conditions such as inflammation or infection. They are also used in monitoring the healing process of wounds and assessing the effectiveness of treatments. Beyond these sectors, cooled thermal infrared imagers find applications in various other industries, including industrial inspection, where they are used to monitor equipment and detect potential failures before they occur. The versatility and adaptability of these imagers make them valuable tools across a wide range of applications, driving their demand and contributing to the growth of the Global Cooled Thermal Infrared Imagers Market.

Global Cooled Thermal Infrared Imagers Market Outlook:

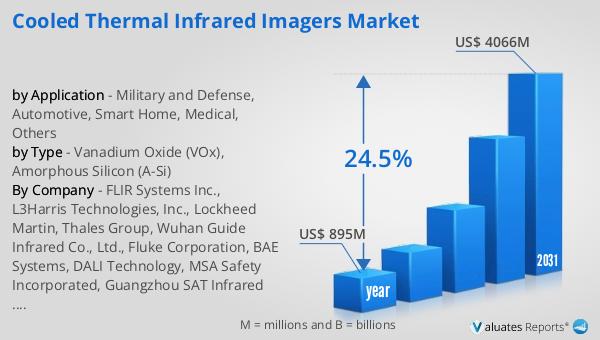

The global market for Cooled Thermal Infrared Imagers, initially valued at $895 million in 2024, is anticipated to expand significantly, reaching an estimated $4,066 million by 2031. This growth trajectory reflects a robust compound annual growth rate (CAGR) of 24.5% over the forecast period. The substantial increase in market size underscores the rising demand for advanced thermal imaging solutions across various industries. The impressive CAGR indicates a strong market momentum, driven by technological advancements and the expanding range of applications for cooled thermal infrared imagers. As industries continue to recognize the value of high-performance thermal imaging technology, the market is poised for sustained growth. The projected market size of $4,066 million by 2031 highlights the significant opportunities for manufacturers and stakeholders in the Global Cooled Thermal Infrared Imagers Market. This growth is expected to be fueled by increasing investments in research and development, as well as the adoption of thermal imaging technology in emerging sectors. The market outlook suggests a promising future for cooled thermal infrared imagers, with continued innovation and expansion into new applications driving their demand and market presence.

| Report Metric | Details |

| Report Name | Cooled Thermal Infrared Imagers Market |

| Accounted market size in year | US$ 895 million |

| Forecasted market size in 2031 | US$ 4066 million |

| CAGR | 24.5% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | FLIR Systems Inc., L3Harris Technologies, Inc., Lockheed Martin, Thales Group, Wuhan Guide Infrared Co., Ltd., Fluke Corporation, BAE Systems, DALI Technology, MSA Safety Incorporated, Guangzhou SAT Infrared Technology Co., Ltd., Elbit Systems, Testo SE & Co. KGaA, Hikvision, NEC Corporation, Fotric Inc., Bullard, Keysight Technologies, Inc. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |