What is Global Display Driver Chip Packaging and Testing Market?

The Global Display Driver Chip Packaging and Testing Market is a specialized segment within the semiconductor industry that focuses on the processes involved in preparing display driver chips for use in various electronic devices. Display driver chips are integral components that control the pixels on screens, enabling the display of images and videos on devices such as smartphones, tablets, televisions, and computer monitors. The packaging process involves encasing the chip in a protective shell to safeguard it from physical damage and environmental factors, while also facilitating its integration into electronic devices. Testing, on the other hand, ensures that these chips function correctly and meet the required performance standards before they are deployed in consumer products. This market is driven by the increasing demand for high-resolution displays and the proliferation of electronic devices across the globe. As technology advances, the need for more sophisticated and efficient display driver chips continues to grow, making packaging and testing crucial steps in the production process. The market is characterized by continuous innovation and the adoption of advanced technologies to enhance the performance and reliability of display driver chips.

Chip Packaging, Chip Testing in the Global Display Driver Chip Packaging and Testing Market:

Chip packaging and testing are critical components of the Global Display Driver Chip Packaging and Testing Market, ensuring that display driver chips are ready for integration into electronic devices. Chip packaging involves several steps, starting with the selection of appropriate materials to encase the chip. The packaging must provide protection against physical damage, moisture, and other environmental factors while maintaining the chip's electrical performance. Various packaging techniques are employed, such as wire bonding, flip-chip, and wafer-level packaging, each offering different advantages in terms of size, cost, and performance. Wire bonding is a traditional method where fine wires connect the chip to the package, while flip-chip involves mounting the chip directly onto the substrate, allowing for better electrical performance and heat dissipation. Wafer-level packaging, on the other hand, is a more advanced technique that allows for smaller and thinner packages, ideal for compact devices. Once the chip is packaged, it undergoes rigorous testing to ensure its functionality and reliability. Testing is a multi-step process that includes electrical testing, thermal testing, and mechanical testing. Electrical testing verifies that the chip operates correctly under various conditions, checking for defects such as short circuits or open circuits. Thermal testing assesses the chip's ability to dissipate heat, ensuring it can operate within safe temperature ranges. Mechanical testing evaluates the chip's physical durability, ensuring it can withstand stresses such as vibration and impact. Advanced testing methods, such as automated test equipment (ATE) and built-in self-test (BIST) techniques, are employed to enhance testing efficiency and accuracy. The importance of chip packaging and testing cannot be overstated, as they directly impact the performance, reliability, and lifespan of display driver chips. As electronic devices become more sophisticated, the demand for high-quality display driver chips increases, driving innovation in packaging and testing technologies. Companies in this market are continually investing in research and development to improve packaging materials and testing methodologies, aiming to reduce costs and enhance chip performance. The integration of artificial intelligence and machine learning in testing processes is also gaining traction, offering the potential for more precise and efficient testing. In summary, chip packaging and testing are vital processes in the Global Display Driver Chip Packaging and Testing Market, ensuring that display driver chips meet the high standards required for modern electronic devices. These processes involve a combination of traditional and advanced techniques, with ongoing innovation aimed at improving efficiency and performance. As the demand for high-resolution displays and compact electronic devices continues to grow, the importance of effective chip packaging and testing will only increase, driving further advancements in this dynamic market.

Communication, Consumer Electronics, Vehicle Electronics, Aerospace, Other in the Global Display Driver Chip Packaging and Testing Market:

The Global Display Driver Chip Packaging and Testing Market plays a crucial role in various sectors, including communication, consumer electronics, vehicle electronics, aerospace, and others. In the communication sector, display driver chips are essential for devices such as smartphones, tablets, and smartwatches, which require high-quality displays for clear and vibrant visuals. The packaging and testing of these chips ensure that they can deliver the necessary performance and reliability, supporting the seamless operation of communication devices. As the demand for advanced communication technologies grows, the need for efficient display driver chips becomes increasingly important, driving innovation in packaging and testing processes. In the consumer electronics sector, display driver chips are used in a wide range of devices, including televisions, monitors, and gaming consoles. These devices require high-resolution displays to provide users with an immersive viewing experience. The packaging and testing of display driver chips ensure that they can meet the stringent performance standards required for consumer electronics, delivering crisp and clear images. As consumer preferences shift towards larger and more advanced displays, the demand for high-quality display driver chips continues to rise, highlighting the importance of effective packaging and testing. Vehicle electronics is another area where the Global Display Driver Chip Packaging and Testing Market is making a significant impact. Modern vehicles are equipped with various display systems, such as infotainment screens, digital dashboards, and rearview cameras, all of which rely on display driver chips. The packaging and testing of these chips ensure that they can withstand the harsh conditions of the automotive environment, including temperature fluctuations and vibrations. As the automotive industry moves towards more connected and autonomous vehicles, the demand for reliable display driver chips is expected to grow, emphasizing the need for robust packaging and testing solutions. In the aerospace sector, display driver chips are used in cockpit displays, navigation systems, and in-flight entertainment systems. These applications require chips that can operate reliably under extreme conditions, such as high altitudes and varying temperatures. The packaging and testing of display driver chips for aerospace applications ensure that they meet the rigorous standards required for safety and performance. As the aerospace industry continues to innovate, the demand for advanced display driver chips is likely to increase, driving further advancements in packaging and testing technologies. Beyond these sectors, the Global Display Driver Chip Packaging and Testing Market also serves other industries, such as healthcare and industrial automation, where display driver chips are used in medical imaging devices and control panels. The packaging and testing of these chips ensure that they can deliver the necessary performance and reliability, supporting the efficient operation of critical systems. As technology continues to evolve, the demand for high-quality display driver chips across various industries is expected to grow, underscoring the importance of effective packaging and testing processes.

Global Display Driver Chip Packaging and Testing Market Outlook:

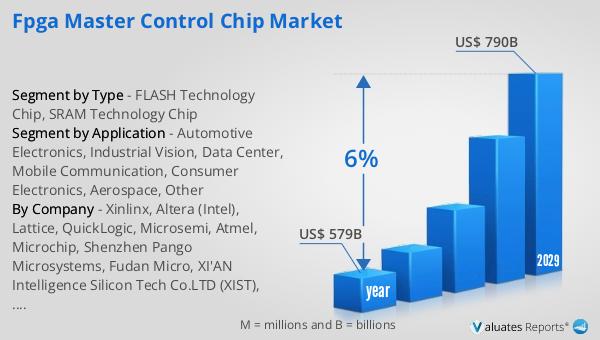

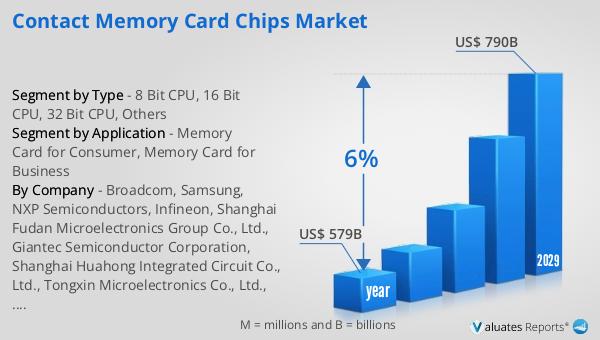

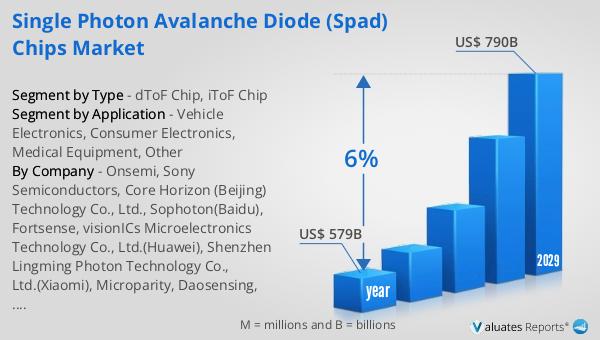

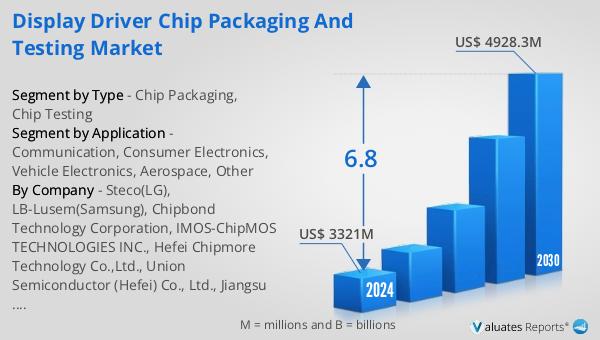

The outlook for the Global Display Driver Chip Packaging and Testing Market indicates a promising growth trajectory. The market is anticipated to expand from $3,321 million in 2024 to $4,928.3 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 6.8% during the forecast period. This growth is driven by the increasing demand for advanced display technologies across various sectors, including consumer electronics, automotive, and aerospace. As electronic devices become more sophisticated, the need for high-performance display driver chips continues to rise, fueling the demand for efficient packaging and testing solutions. The broader semiconductor market, which was valued at $579 billion in 2022, is also projected to grow significantly, reaching $790 billion by 2029 with a CAGR of 6%. This growth underscores the importance of the Display Driver Chip Packaging and Testing Market within the semiconductor industry, as it plays a critical role in ensuring the quality and reliability of display driver chips. As technology continues to advance, the market is expected to witness further innovations in packaging and testing methodologies, enhancing the performance and efficiency of display driver chips. This positive outlook highlights the potential for continued growth and development in the Global Display Driver Chip Packaging and Testing Market, driven by the increasing demand for high-quality display technologies across various industries.

| Report Metric | Details |

| Report Name | Display Driver Chip Packaging and Testing Market |

| Accounted market size in 2024 | US$ 3321 million |

| Forecasted market size in 2030 | US$ 4928.3 million |

| CAGR | 6.8 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Steco(LG), LB-Lusem(Samsung), Chipbond Technology Corporation, IMOS-ChipMOS TECHNOLOGIES INC., Hefei Chipmore Technology Co.,Ltd., Union Semiconductor (Hefei) Co., Ltd., Jiangsu Napace Semiconductor Co., Ltd., Tongfu Microelectronics Co.,ltd., JCET Group Co.,Ltd., ADVANCED SEMICONDUCTOR ENGINEERING, INC., Hitech Semiconductor (Wuxi) Co., Ltd., Hefei Chipmore Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |