What is Global Diesel Engine Block Market?

The Global Diesel Engine Block Market is a significant segment within the automotive industry, focusing on the production and distribution of engine blocks specifically designed for diesel engines. Diesel engine blocks are crucial components that house the cylinders and other essential parts of an engine, providing the structural integrity needed to withstand the high pressures and temperatures generated during combustion. This market encompasses a wide range of activities, including the manufacturing of engine blocks using various materials, such as cast iron and aluminum alloys, and the supply chain logistics involved in delivering these components to automotive manufacturers worldwide. The demand for diesel engine blocks is driven by the widespread use of diesel engines in various applications, including passenger cars, commercial vehicles, and industrial machinery. As the automotive industry continues to evolve, with increasing emphasis on fuel efficiency and emissions reduction, the diesel engine block market is also adapting, with innovations in materials and manufacturing processes aimed at enhancing performance and sustainability. This market is characterized by a mix of established players and emerging companies, all striving to meet the diverse needs of automotive manufacturers and end-users across different regions.

Cast Iron Cylinder Block, Aluminum Alloy Cylinder Block, Other in the Global Diesel Engine Block Market:

In the Global Diesel Engine Block Market, the choice of material for manufacturing engine blocks is critical, as it directly impacts the performance, durability, and efficiency of the engine. Cast iron cylinder blocks have been a traditional choice due to their excellent strength and wear resistance. They are particularly favored in heavy-duty applications where durability is paramount. Cast iron's ability to withstand high temperatures and pressures makes it ideal for diesel engines, which operate under more strenuous conditions compared to gasoline engines. However, the downside of cast iron is its weight, which can negatively affect fuel efficiency and vehicle performance. On the other hand, aluminum alloy cylinder blocks are gaining popularity due to their lightweight nature, which contributes to improved fuel efficiency and handling. Aluminum alloys offer good thermal conductivity, which helps in better heat dissipation, thus enhancing engine performance. They are increasingly used in passenger cars and light commercial vehicles where weight reduction is a priority. Despite being more expensive than cast iron, the benefits of aluminum alloys in terms of fuel economy and emissions reduction make them an attractive option for modern automotive manufacturers. Additionally, there are other materials and technologies being explored in the market, such as compacted graphite iron (CGI) and hybrid materials, which aim to combine the benefits of both cast iron and aluminum. CGI, for instance, offers a middle ground with better strength than aluminum and lighter weight than traditional cast iron. These innovations reflect the ongoing efforts within the industry to balance performance, cost, and environmental considerations. As the market evolves, manufacturers are continuously investing in research and development to explore new materials and manufacturing techniques that can meet the stringent demands of modern diesel engines. This dynamic landscape presents opportunities for both established companies and new entrants to innovate and capture market share by offering advanced solutions that cater to the diverse needs of automotive manufacturers and consumers worldwide.

Passenger Cars, Commercial Vehicles in the Global Diesel Engine Block Market:

The usage of diesel engine blocks in passenger cars and commercial vehicles highlights the versatility and importance of this market segment. In passenger cars, diesel engines are often chosen for their superior fuel efficiency and torque, making them ideal for long-distance travel and highway driving. Diesel engine blocks in passenger cars are typically made from lightweight materials like aluminum alloys to enhance fuel economy and reduce emissions. The focus in this segment is on balancing performance with environmental considerations, as consumers increasingly demand vehicles that are both powerful and eco-friendly. Manufacturers are therefore investing in advanced materials and technologies to produce diesel engine blocks that meet these dual objectives. In commercial vehicles, such as trucks and buses, diesel engines are the preferred choice due to their robustness and ability to deliver high power output and torque, essential for transporting heavy loads over long distances. The engine blocks used in commercial vehicles are often made from cast iron or compacted graphite iron, materials known for their strength and durability. These vehicles require engine blocks that can withstand the rigors of continuous operation and high-stress conditions. The commercial vehicle segment places a premium on reliability and longevity, with manufacturers focusing on producing engine blocks that can endure the demanding environments in which these vehicles operate. As the global economy continues to grow, the demand for commercial vehicles is expected to rise, further driving the need for durable and efficient diesel engine blocks. Both passenger cars and commercial vehicles benefit from ongoing advancements in diesel engine block technology, which aim to improve performance, reduce emissions, and enhance fuel efficiency. As regulatory standards become more stringent, particularly concerning emissions, the diesel engine block market is under pressure to innovate and adapt. This has led to increased collaboration between automotive manufacturers and material scientists to develop new solutions that meet the evolving needs of the industry. The future of diesel engine blocks in both passenger cars and commercial vehicles will likely be shaped by these technological advancements and the industry's ability to respond to changing consumer preferences and regulatory requirements.

Global Diesel Engine Block Market Outlook:

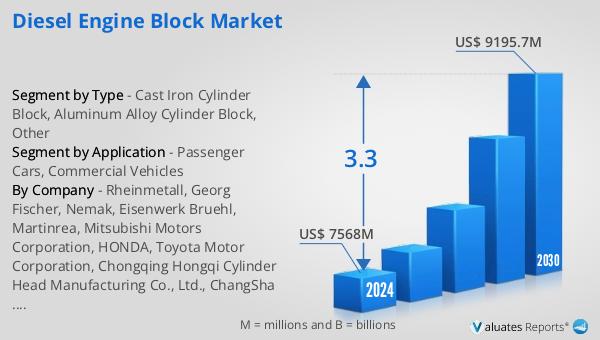

The outlook for the Global Diesel Engine Block Market indicates a steady growth trajectory over the coming years. The market is anticipated to expand from a valuation of approximately $7,568 million in 2024 to around $9,195.7 million by 2030. This growth is expected to occur at a Compound Annual Growth Rate (CAGR) of 3.3% during the forecast period. This projected increase reflects the ongoing demand for diesel engine blocks across various automotive segments, driven by the need for efficient and durable engine solutions. The market's growth is supported by several factors, including advancements in material technology, increasing production of diesel-powered vehicles, and the rising demand for commercial vehicles in emerging economies. As manufacturers continue to innovate and improve the performance and efficiency of diesel engine blocks, the market is poised to capitalize on these developments. Additionally, the emphasis on reducing emissions and enhancing fuel efficiency is likely to spur further investment in research and development, leading to the introduction of new materials and manufacturing processes. This positive market outlook underscores the importance of diesel engine blocks in the automotive industry and highlights the opportunities for growth and innovation in this sector.

| Report Metric | Details |

| Report Name | Diesel Engine Block Market |

| Accounted market size in 2024 | US$ 7568 in million |

| Forecasted market size in 2030 | US$ 9195.7 million |

| CAGR | 3.3 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Rheinmetall, Georg Fischer, Nemak, Eisenwerk Bruehl, Martinrea, Mitsubishi Motors Corporation, HONDA, Toyota Motor Corporation, Chongqing Hongqi Cylinder Head Manufacturing Co., Ltd., ChangSha XiMai Mechanical Construction Co.,Ltd., Linamar(Wuxi) Corporation, Xiangyang Changyuandonggu Industry Co.,Ltd., Wuxi Best Precision Machinery Co.,Ltd., Ningbo Xusheng Group Co.,ltd., IKD Co.,Ltd., Anhui Quanchai Engine Co.,Ltd, Guangdong Hongtu Technology (Holdings) Co.,Ltd., Loncin Motor Co.,Ltd., Faw Foundry Co., Ltd., Ruifeng Power Group |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |