What is Automotive High-speed CAN Transceivers - Global Market?

Automotive High-speed CAN (Controller Area Network) Transceivers are integral components in modern vehicles, facilitating communication between various electronic control units (ECUs) within a vehicle. These transceivers enable high-speed data exchange, ensuring that different systems such as engine control, transmission, braking, and infotainment can communicate effectively and efficiently. The global market for these transceivers is driven by the increasing complexity and sophistication of automotive electronics, as vehicles become more reliant on digital systems for enhanced performance, safety, and user experience. With the rise of electric and autonomous vehicles, the demand for robust and reliable communication networks within vehicles has surged, further propelling the market for high-speed CAN transceivers. These components are crucial for maintaining the seamless operation of a vehicle's electronic systems, ensuring that data is transmitted quickly and accurately across various subsystems. As the automotive industry continues to evolve, the role of high-speed CAN transceivers becomes even more critical, supporting advancements in vehicle technology and contributing to the overall efficiency and safety of modern automobiles.

Max Data Rate 1Mbps, Max Data Rate 5Mbps, Others in the Automotive High-speed CAN Transceivers - Global Market:

In the realm of automotive high-speed CAN transceivers, the maximum data rate is a critical specification that determines the speed at which data can be transmitted across the vehicle's network. The most common data rates in this context are 1Mbps and 5Mbps, each serving different needs and applications within the automotive industry. A maximum data rate of 1Mbps is typically sufficient for most traditional automotive applications, where the communication between ECUs does not require extremely high-speed data transfer. This data rate supports essential functions such as engine management, transmission control, and basic safety systems, providing a reliable and efficient means of communication that meets the needs of most conventional vehicles. However, as vehicles become more advanced, with features such as advanced driver-assistance systems (ADAS), infotainment, and connectivity, the demand for higher data rates has increased. This is where the 5Mbps data rate comes into play, offering a faster and more robust communication channel that can handle the increased data load from these sophisticated systems. The 5Mbps transceivers are particularly beneficial in scenarios where real-time data processing is crucial, such as in autonomous driving technologies, where rapid and accurate data exchange is essential for the vehicle's operation and safety. Beyond these standard data rates, there are also other options available in the market, catering to specific needs and applications. These may include custom data rates or specialized transceivers designed for unique automotive applications, providing flexibility and adaptability to meet the diverse requirements of modern vehicles. As the automotive industry continues to innovate and evolve, the demand for high-speed CAN transceivers with varying data rates will likely grow, driven by the need for faster, more reliable communication networks within vehicles. This evolution reflects the broader trend towards increased digitalization and connectivity in the automotive sector, as manufacturers strive to enhance vehicle performance, safety, and user experience through advanced electronic systems.

Passenger Cars, Commercial Vehicles in the Automotive High-speed CAN Transceivers - Global Market:

The usage of automotive high-speed CAN transceivers is prevalent in both passenger cars and commercial vehicles, each with its unique set of requirements and applications. In passenger cars, these transceivers play a vital role in ensuring the smooth operation of various electronic systems that enhance the driving experience and safety. For instance, they facilitate communication between the engine control unit and other critical systems such as the transmission, braking, and steering, ensuring that the vehicle operates efficiently and safely. Additionally, high-speed CAN transceivers support advanced features such as adaptive cruise control, lane-keeping assist, and collision avoidance systems, which rely on rapid data exchange to function effectively. In the realm of infotainment, these transceivers enable seamless connectivity between the vehicle's multimedia systems, navigation, and external devices, providing a rich and integrated user experience. In commercial vehicles, the role of high-speed CAN transceivers is equally important, albeit with a focus on different priorities. Commercial vehicles, such as trucks and buses, often require robust and reliable communication networks to support their complex operations and ensure safety and efficiency. High-speed CAN transceivers facilitate the integration of various systems, such as engine management, transmission control, and telematics, enabling fleet operators to monitor and manage their vehicles effectively. These transceivers also support advanced safety features, such as electronic stability control and anti-lock braking systems, which are crucial for the safe operation of large commercial vehicles. Furthermore, in the context of logistics and transportation, high-speed CAN transceivers enable real-time data exchange between the vehicle and external systems, supporting functions such as route optimization, fuel management, and predictive maintenance. This capability is particularly valuable for fleet operators, who rely on accurate and timely data to optimize their operations and reduce costs. As both passenger cars and commercial vehicles continue to evolve, the demand for high-speed CAN transceivers will likely increase, driven by the need for more sophisticated electronic systems and enhanced connectivity. This trend reflects the broader shift towards digitalization and automation in the automotive industry, as manufacturers and operators seek to improve vehicle performance, safety, and efficiency through advanced technology.

Automotive High-speed CAN Transceivers - Global Market Outlook:

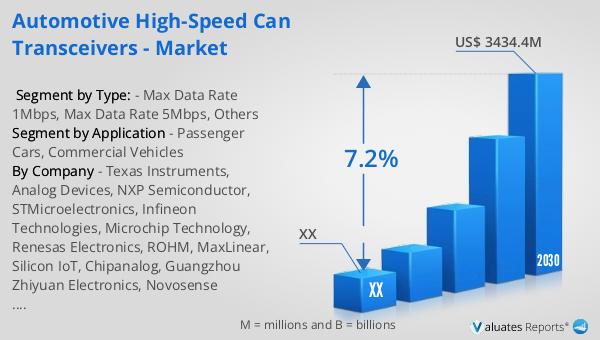

The global market for automotive high-speed CAN transceivers was valued at approximately $2,103 million in 2023. It is projected to grow to a revised size of around $3,434.4 million by 2030, reflecting a compound annual growth rate (CAGR) of 7.2% during the forecast period from 2024 to 2030. Currently, over 90% of the world's automobiles are concentrated in three major continents: Asia, Europe, and North America. Among these, Asia leads with 56% of global automobile production, followed by Europe with 20%, and North America with 16%. This distribution highlights the significant role these regions play in the automotive industry, both in terms of production and consumption. The growth in the market for high-speed CAN transceivers is closely linked to the increasing demand for advanced automotive electronics and the ongoing digital transformation within the industry. As vehicles become more connected and reliant on sophisticated electronic systems, the need for efficient and reliable communication networks, such as those provided by high-speed CAN transceivers, becomes increasingly important. This trend is expected to continue as the automotive industry evolves, driven by advancements in technology and changing consumer preferences.

| Report Metric | Details |

| Report Name | Automotive High-speed CAN Transceivers - Market |

| Forecasted market size in 2030 | US$ 3434.4 million |

| CAGR | 7.2% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Texas Instruments, Analog Devices, NXP Semiconductor, STMicroelectronics, Infineon Technologies, Microchip Technology, Renesas Electronics, ROHM, MaxLinear, Silicon IoT, Chipanalog, Guangzhou Zhiyuan Electronics, Novosense Microelectronics, Huaguan Semiconductor |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |