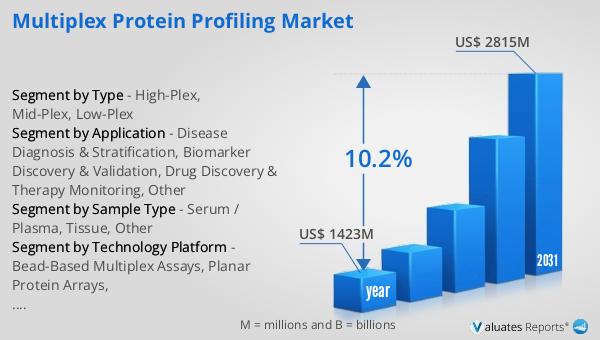

What is Integrated Circuit (IC) Pin Probe - Global Market?

Integrated Circuit (IC) Pin Probes are essential components in the global electronics market, serving as critical tools for testing and ensuring the functionality of integrated circuits. These probes are designed to make contact with the pins of an IC, allowing for the transmission of electrical signals during testing processes. The global market for IC pin probes is driven by the increasing demand for electronic devices and the need for efficient testing solutions in the semiconductor industry. As technology advances, the complexity of integrated circuits increases, necessitating more sophisticated testing equipment. IC pin probes are used in various applications, including quality control, research and development, and production testing. They are crucial for ensuring that ICs meet the required specifications and function correctly in their intended applications. The market is characterized by continuous innovation, with manufacturers focusing on developing probes that offer higher precision, durability, and compatibility with a wide range of ICs. As the electronics industry continues to grow, the demand for IC pin probes is expected to rise, driven by the need for reliable and efficient testing solutions.

Gold Plating, Nickel Plating, Others in the Integrated Circuit (IC) Pin Probe - Global Market:

Gold plating, nickel plating, and other types of plating are critical in the manufacturing and performance of Integrated Circuit (IC) Pin Probes. Gold plating is widely used due to its excellent conductivity and resistance to corrosion, making it ideal for ensuring reliable electrical connections. The gold layer provides a smooth and stable surface, which is crucial for maintaining consistent contact with the IC pins during testing. This type of plating is particularly beneficial in applications where high precision and reliability are required, such as in aerospace and medical devices. Nickel plating, on the other hand, offers a cost-effective alternative with good wear resistance and moderate conductivity. It is often used in applications where cost is a significant consideration, and the environmental conditions are less demanding. Nickel plating provides a hard surface that can withstand repeated use, making it suitable for high-volume testing environments. Other types of plating, such as palladium or silver, are also used depending on the specific requirements of the application. These materials offer unique properties that can enhance the performance of IC pin probes in certain conditions. For instance, palladium plating provides excellent wear resistance and is often used in applications where durability is a primary concern. Silver plating, known for its superior conductivity, is used in applications where minimizing electrical resistance is critical. The choice of plating material is influenced by factors such as the intended application, environmental conditions, and cost considerations. Manufacturers of IC pin probes continuously explore new materials and plating techniques to improve the performance and longevity of their products. The global market for IC pin probes is highly competitive, with companies striving to offer innovative solutions that meet the evolving needs of the electronics industry. As technology advances, the demand for high-performance IC pin probes with specialized plating will continue to grow, driven by the increasing complexity of electronic devices and the need for precise testing solutions.

Automotive, Medical, Communications, Aviation, Consumer Electronics, Others in the Integrated Circuit (IC) Pin Probe - Global Market:

Integrated Circuit (IC) Pin Probes play a vital role in various industries, including automotive, medical, communications, aviation, consumer electronics, and others. In the automotive industry, IC pin probes are used extensively in the testing of electronic control units (ECUs), sensors, and other critical components that ensure the safety and efficiency of modern vehicles. With the increasing integration of electronics in vehicles, the demand for reliable testing solutions like IC pin probes is on the rise. In the medical field, these probes are essential for testing medical devices and equipment, ensuring they meet stringent safety and performance standards. The accuracy and reliability of IC pin probes are crucial in this sector, where the stakes are high, and any malfunction can have serious consequences. In the communications industry, IC pin probes are used to test a wide range of devices, from smartphones to network infrastructure equipment. As the demand for faster and more reliable communication technologies grows, so does the need for efficient testing solutions. In aviation, IC pin probes are used to test avionics systems, which are critical for the safe operation of aircraft. The precision and durability of these probes are essential in this industry, where failure is not an option. In the consumer electronics sector, IC pin probes are used to test a variety of devices, from televisions to gaming consoles. The rapid pace of innovation in this industry drives the need for advanced testing solutions that can keep up with the latest technologies. Other industries, such as industrial automation and renewable energy, also rely on IC pin probes for testing and quality assurance. The versatility and reliability of these probes make them indispensable tools in the global electronics market. As technology continues to evolve, the demand for IC pin probes in these industries is expected to grow, driven by the need for precise and efficient testing solutions.

Integrated Circuit (IC) Pin Probe - Global Market Outlook:

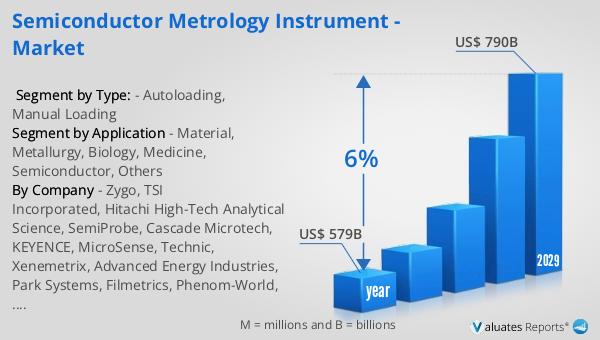

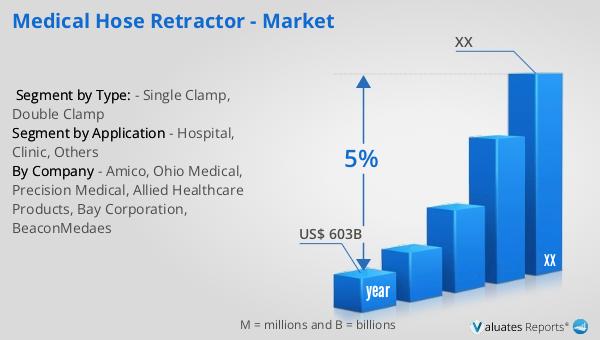

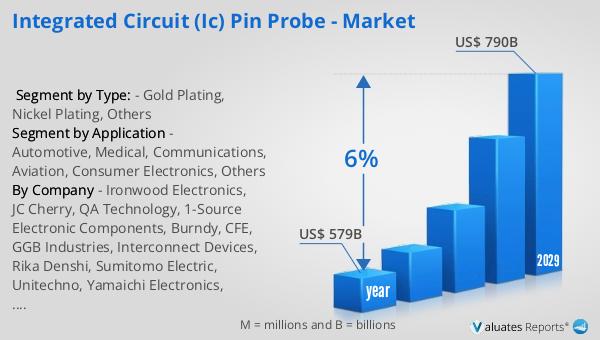

The global semiconductor market, which was valued at approximately $579 billion in 2022, is anticipated to reach around $790 billion by 2029, reflecting a compound annual growth rate (CAGR) of 6% over the forecast period. This growth is indicative of the increasing demand for semiconductors across various industries, driven by advancements in technology and the proliferation of electronic devices. The semiconductor market is a critical component of the global economy, underpinning the development and production of a wide range of electronic products. As industries such as automotive, consumer electronics, and telecommunications continue to expand, the demand for semiconductors is expected to rise correspondingly. The projected growth in the semiconductor market highlights the importance of innovation and investment in this sector, as companies strive to meet the evolving needs of consumers and businesses. The increasing complexity of electronic devices and the push for more efficient and powerful technologies are key drivers of this growth. As a result, the semiconductor industry is poised for significant expansion, with opportunities for growth and development in various segments. The anticipated increase in market size underscores the critical role that semiconductors play in the modern world, enabling advancements in technology and driving economic growth.

| Report Metric | Details |

| Report Name | Integrated Circuit (IC) Pin Probe - Market |

| Accounted market size in year | US$ 579 billion |

| Forecasted market size in 2029 | US$ 790 billion |

| CAGR | 6% |

| Base Year | year |

| Forecasted years | 2024 - 2029 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Ironwood Electronics, JC Cherry, QA Technology, 1-Source Electronic Components, Burndy, CFE, GGB Industries, Interconnect Devices, Rika Denshi, Sumitomo Electric, Unitechno, Yamaichi Electronics, Technoprobe, C.C.P. Contact Probes, SFENG, Shanghai Fintest Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |