What is Volatile Organic Compounds (VOC) Recovery System - Global Market?

Volatile Organic Compounds (VOC) Recovery Systems are essential technologies used to capture and recycle VOCs, which are harmful pollutants emitted from various industrial processes. These systems are crucial in reducing environmental pollution and improving air quality. VOCs are organic chemicals that easily vaporize at room temperature, and they are found in products like paints, solvents, and fuels. The global market for VOC recovery systems is driven by stringent environmental regulations and the growing awareness of the need to reduce air pollution. These systems help industries comply with environmental standards by capturing VOC emissions before they are released into the atmosphere. The market is diverse, with various technologies available to suit different industrial needs. As industries continue to seek sustainable solutions, the demand for VOC recovery systems is expected to grow. This growth is supported by advancements in technology that make these systems more efficient and cost-effective. Overall, VOC recovery systems play a vital role in promoting environmental sustainability and protecting public health by minimizing the release of harmful pollutants into the air.

Regenerative Thermal Oxidation, Recuperative Thermal Oxidation, Catalytic Oxidation, Adsorption by Activated Carbon, Cryocondensation, Others in the Volatile Organic Compounds (VOC) Recovery System - Global Market:

Regenerative Thermal Oxidation (RTO) is a widely used technology in VOC recovery systems. It involves the use of high temperatures to oxidize VOCs into carbon dioxide and water vapor. The process is highly efficient, as it uses a regenerative heat exchanger to preheat the incoming air stream, reducing the energy required for oxidation. This makes RTO an energy-efficient option for industries looking to reduce VOC emissions. Recuperative Thermal Oxidation, on the other hand, also uses heat to oxidize VOCs but employs a different heat recovery system. It uses a heat exchanger to transfer heat from the exhaust gases to the incoming air stream, which is less efficient than RTO but still effective in reducing emissions. Catalytic Oxidation is another method used in VOC recovery systems. It involves the use of a catalyst to lower the temperature required for oxidation, making it an energy-efficient option. This method is particularly useful for industries with low concentrations of VOCs. Adsorption by Activated Carbon is a physical process where VOCs are captured on the surface of activated carbon. This method is effective for low concentrations of VOCs and is often used in combination with other technologies. Cryocondensation is a process that involves cooling the VOC-laden air stream to condense the VOCs into a liquid form. This method is highly effective for high concentrations of VOCs and is often used in industries with large emissions. Other technologies in the VOC recovery market include biofiltration and membrane separation, which offer alternative solutions for capturing and recycling VOCs. Each of these technologies has its advantages and limitations, and the choice of technology depends on the specific needs of the industry. Overall, the global market for VOC recovery systems is diverse, with a range of technologies available to meet the growing demand for sustainable solutions.

Petroleum and Petrochemical, Packaging and Printing, Pharmaceuticals, Food Industry, Plastic and Rubber Industry, Iron and Steel Industry, Coatings and Inks, Other in the Volatile Organic Compounds (VOC) Recovery System - Global Market:

The usage of Volatile Organic Compounds (VOC) Recovery Systems spans across various industries, each with its unique requirements and challenges. In the petroleum and petrochemical industry, VOC recovery systems are crucial for capturing emissions during the extraction, refining, and distribution of oil and gas. These systems help in reducing air pollution and improving the efficiency of operations by recovering valuable hydrocarbons. In the packaging and printing industry, VOCs are emitted from inks, adhesives, and coatings. VOC recovery systems help in capturing these emissions, ensuring compliance with environmental regulations and improving indoor air quality. The pharmaceutical industry also relies on VOC recovery systems to capture emissions from solvents used in the manufacturing process. This not only helps in reducing environmental impact but also in recovering valuable solvents for reuse. In the food industry, VOC recovery systems are used to capture emissions from processes like frying and baking, ensuring a cleaner and safer working environment. The plastic and rubber industry emits VOCs during the production and processing of materials. VOC recovery systems help in capturing these emissions, reducing environmental impact, and improving the quality of products. In the iron and steel industry, VOCs are emitted during the production and processing of metals. VOC recovery systems help in capturing these emissions, ensuring compliance with environmental regulations and improving the efficiency of operations. The coatings and inks industry also relies on VOC recovery systems to capture emissions from paints, varnishes, and inks. This helps in reducing air pollution and improving the quality of products. Other industries, such as electronics and textiles, also use VOC recovery systems to capture emissions from various processes. Overall, the usage of VOC recovery systems is essential for industries looking to reduce their environmental impact and improve the efficiency of their operations.

Volatile Organic Compounds (VOC) Recovery System - Global Market Outlook:

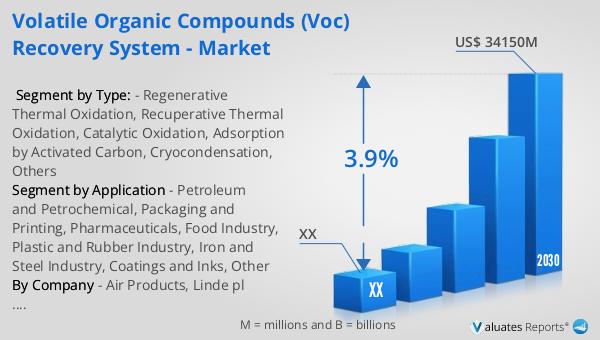

The global market for Volatile Organic Compounds (VOC) Recovery Systems was valued at approximately $26.15 billion in 2023. This market is projected to grow, reaching an estimated value of $34.15 billion by 2030, with a compound annual growth rate (CAGR) of 3.9% during the forecast period from 2024 to 2030. This growth is driven by increasing environmental regulations and the need for industries to reduce their carbon footprint. As industries become more aware of the environmental impact of VOC emissions, the demand for recovery systems is expected to rise. The market is also supported by advancements in technology, which make VOC recovery systems more efficient and cost-effective. These systems are essential for industries looking to comply with environmental standards and improve the sustainability of their operations. The growth of the VOC recovery market is a positive sign for the environment, as it indicates a shift towards more sustainable industrial practices. As the market continues to expand, it is expected to play a crucial role in reducing air pollution and protecting public health. Overall, the global market for VOC recovery systems is poised for significant growth, driven by the increasing demand for sustainable solutions and the need to reduce environmental impact.

| Report Metric | Details |

| Report Name | Volatile Organic Compounds (VOC) Recovery System - Market |

| Forecasted market size in 2030 | US$ 34150 million |

| CAGR | 3.9% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Air Products, Linde pl (Praxair), Wärtsilä, Munters, TOYOBO, Taikisha, Nippon Gases, Calgon Carbon Corporation, Condorchem Envitech, Gulf Coast Environmental Systems, Anguil, ComEnCo Systems, POLARIS SRL, Bay Environmental Technology, KVT Process Technology, CECO Environmental, SINOPEC Qingdao Safety Engineering, Naide, ECOTEC, Beijing CEC Environmental Engineering |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |