What is Global Red Seaweed Extract Market?

The Global Red Seaweed Extract Market is a rapidly expanding sector within the broader natural ingredients industry. Red seaweed, a type of marine algae, is harvested primarily for its rich content of carrageenan, agar, and other valuable compounds. These extracts are widely used across various industries due to their gelling, thickening, and stabilizing properties. The market's growth is driven by increasing consumer demand for natural and organic products, as well as the rising awareness of the health benefits associated with red seaweed extracts. These benefits include improved digestion, enhanced immune function, and potential anti-inflammatory effects. Additionally, the sustainability aspect of seaweed cultivation, which requires no fertilizers or pesticides and absorbs carbon dioxide, adds to its appeal. The market is also influenced by technological advancements in extraction processes, which enhance the quality and yield of the extracts. As a result, the Global Red Seaweed Extract Market is poised for significant growth, with applications spanning from food and beverages to pharmaceuticals and cosmetics, reflecting its versatility and increasing importance in various sectors.

Powder, Liquid, Gel, Others in the Global Red Seaweed Extract Market:

In the Global Red Seaweed Extract Market, the product is available in several forms, including powder, liquid, gel, and others, each catering to different industrial needs and applications. The powdered form of red seaweed extract is particularly popular due to its ease of storage, transportation, and long shelf life. It is widely used in the food industry as a thickening agent in products like sauces, soups, and dairy items. The powder form is also favored in the cosmetics industry for its ability to blend seamlessly into formulations, providing skin benefits such as hydration and anti-aging properties. On the other hand, the liquid form of red seaweed extract is often utilized in applications where immediate solubility is required. It is commonly used in beverages, where it acts as a stabilizer and enhances the texture of the drink. The liquid form is also preferred in the pharmaceutical industry for its ease of incorporation into liquid medicines and supplements. The gel form of red seaweed extract is primarily used in the food industry, particularly in the production of jellies, desserts, and confectioneries, where it provides the desired gel-like consistency. Additionally, the gel form is used in the cosmetics industry for its moisturizing properties and ability to form a protective barrier on the skin. Other forms of red seaweed extract, such as flakes or granules, are used in niche applications where specific textural or functional properties are required. These diverse forms of red seaweed extract highlight the versatility of the product and its ability to meet the varying demands of different industries. The choice of form often depends on the specific application requirements, processing conditions, and desired end-product characteristics. As the market continues to grow, manufacturers are likely to innovate and develop new forms of red seaweed extract to cater to emerging needs and applications.

Food and Beverage, Paints, Cosmetics, Animal Feed Additives, Pharmaceuticals, Industrial Applications, Others in the Global Red Seaweed Extract Market:

The Global Red Seaweed Extract Market finds extensive usage across various sectors, each leveraging the unique properties of the extract to enhance their products. In the food and beverage industry, red seaweed extract is primarily used as a natural thickening, gelling, and stabilizing agent. It is commonly found in dairy products, processed meats, and plant-based alternatives, where it improves texture and shelf life. In the beverage sector, it helps stabilize emulsions and suspensions, ensuring a consistent product. The paints industry utilizes red seaweed extract for its rheological properties, which enhance the viscosity and stability of paint formulations. This results in improved application and finish quality. In cosmetics, red seaweed extract is valued for its hydrating and anti-aging benefits. It is incorporated into skincare products, such as creams and serums, to improve skin texture and elasticity. The animal feed industry uses red seaweed extract as a nutritional supplement, providing essential minerals and promoting gut health in livestock. In pharmaceuticals, the extract is used for its potential health benefits, including anti-inflammatory and immune-boosting properties. It is often included in dietary supplements and functional foods. Industrial applications of red seaweed extract include its use in bioplastics and biodegradable films, where it contributes to the development of sustainable materials. Other niche applications may involve its use in water treatment and agriculture, where its natural properties offer environmental benefits. Overall, the diverse applications of red seaweed extract across these sectors underscore its versatility and growing importance as a natural ingredient.

Global Red Seaweed Extract Market Outlook:

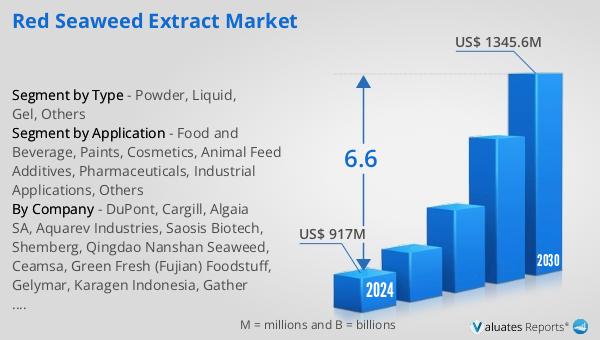

The outlook for the Global Red Seaweed Extract Market is promising, with projections indicating significant growth in the coming years. The market is expected to expand from a valuation of US$ 917 million in 2024 to approximately US$ 1345.6 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 6.6% during the forecast period. This growth is driven by increasing consumer demand for natural and sustainable products, as well as the expanding applications of red seaweed extract across various industries. In particular, the food and beverage, cosmetics, and pharmaceutical sectors are anticipated to be key contributors to this growth, as they continue to incorporate red seaweed extract into their product offerings. Additionally, the market size of China's plant extract industry is projected to grow at a CAGR of 10% from 2023 to 2028, highlighting the broader trend towards natural ingredients in the global market. This growth is supported by advancements in extraction technologies, which enhance the quality and efficiency of red seaweed extract production. As a result, the Global Red Seaweed Extract Market is poised for robust expansion, driven by its versatility, sustainability, and alignment with consumer preferences for natural products.

| Report Metric | Details |

| Report Name | Red Seaweed Extract Market |

| Accounted market size in 2024 | US$ 917 million |

| Forecasted market size in 2030 | US$ 1345.6 million |

| CAGR | 6.6 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | DuPont, Cargill, Algaia SA, Aquarev Industries, Saosis Biotech, Shemberg, Qingdao Nanshan Seaweed, Ceamsa, Green Fresh (Fujian) Foodstuff, Gelymar, Karagen Indonesia, Gather Great Ocean |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |