What is Global Enteroviruses Testing Kit Market?

The Global Enteroviruses Testing Kit Market is a specialized segment within the broader medical diagnostics industry, focusing on the detection and analysis of enteroviruses. Enteroviruses are a group of viruses that can cause a variety of diseases, ranging from mild respiratory illnesses to more severe conditions like meningitis and myocarditis. These viruses are highly contagious and can spread rapidly, making timely and accurate diagnosis crucial for effective disease management and control. The testing kits are designed to identify the presence of enteroviruses in human samples, such as blood, stool, or cerebrospinal fluid, using various diagnostic techniques. The market for these testing kits is driven by the increasing prevalence of enterovirus infections, advancements in diagnostic technologies, and a growing awareness of the importance of early detection. Additionally, the rise in healthcare expenditure and the expansion of healthcare infrastructure in emerging economies are contributing to the market's growth. As healthcare providers and laboratories seek more efficient and reliable diagnostic solutions, the demand for enteroviruses testing kits is expected to continue rising, offering significant opportunities for manufacturers and stakeholders in the industry.

Rapid Detection Test, RT- Polymerase Chain Reaction(PCR) in the Global Enteroviruses Testing Kit Market:

Rapid Detection Tests (RDTs) and RT-Polymerase Chain Reaction (PCR) are two pivotal methodologies employed in the Global Enteroviruses Testing Kit Market, each offering unique advantages in the detection and analysis of enteroviruses. Rapid Detection Tests are designed to provide quick results, often within minutes to a few hours, making them invaluable in clinical settings where time is of the essence. These tests typically involve the use of immunoassays that detect viral antigens or antibodies in patient samples. The primary advantage of RDTs is their speed and ease of use, which allows healthcare providers to make swift decisions regarding patient management and treatment. However, while RDTs offer convenience, they may not always match the sensitivity and specificity of more advanced techniques like RT-PCR. RT-Polymerase Chain Reaction, on the other hand, is a molecular diagnostic technique that amplifies viral RNA to detectable levels, allowing for highly sensitive and specific detection of enteroviruses. This method involves extracting RNA from the patient sample, converting it into complementary DNA (cDNA) using reverse transcription, and then amplifying the cDNA through a series of thermal cycles. The amplified product is then analyzed to confirm the presence of enteroviruses. RT-PCR is considered the gold standard in enterovirus detection due to its high accuracy and ability to detect even low levels of viral RNA. This makes it particularly useful in cases where the viral load is low or when early detection is critical. The choice between RDTs and RT-PCR often depends on the clinical context and the resources available. In emergency situations or resource-limited settings, RDTs may be preferred due to their rapid turnaround time and minimal equipment requirements. Conversely, in well-equipped laboratories where accuracy is paramount, RT-PCR is often the method of choice. The integration of these testing methods into the Global Enteroviruses Testing Kit Market reflects the diverse needs of healthcare providers and the ongoing advancements in diagnostic technologies. Moreover, the development of multiplex RT-PCR assays, which can simultaneously detect multiple pathogens, is a significant advancement in the field. These assays enhance the efficiency of testing by reducing the time and resources needed to diagnose co-infections or differentiate between similar viral infections. As the demand for comprehensive and accurate diagnostic solutions grows, the role of RT-PCR in the enteroviruses testing kit market is expected to expand further. In conclusion, both Rapid Detection Tests and RT-Polymerase Chain Reaction play crucial roles in the Global Enteroviruses Testing Kit Market. While RDTs offer speed and convenience, RT-PCR provides unmatched accuracy and sensitivity. The choice between these methods depends on various factors, including the clinical setting, available resources, and the specific diagnostic needs. As the market continues to evolve, the integration of these technologies will be essential in meeting the growing demand for efficient and reliable enterovirus diagnostics.

Hospitals, Speciality Clinics, Research Laboratories in the Global Enteroviruses Testing Kit Market:

The usage of Global Enteroviruses Testing Kits in hospitals, specialty clinics, and research laboratories is integral to the effective management and study of enterovirus infections. In hospitals, these testing kits are crucial for the timely diagnosis and treatment of patients presenting with symptoms indicative of enterovirus infections. Hospitals often deal with a high volume of patients, and the ability to quickly and accurately diagnose enterovirus infections can significantly impact patient outcomes. Rapid Detection Tests are particularly useful in emergency departments where swift decision-making is essential. On the other hand, RT-PCR tests are employed in hospital laboratories for their high sensitivity and specificity, ensuring accurate diagnosis even in complex cases. Specialty clinics, which focus on specific areas of healthcare such as infectious diseases or pediatrics, also rely heavily on enteroviruses testing kits. These clinics often deal with patients who have been referred for specialized care, and accurate diagnosis is critical for developing effective treatment plans. The use of RT-PCR in specialty clinics allows for precise identification of enterovirus strains, aiding in the management of outbreaks and the implementation of targeted interventions. Additionally, the availability of rapid testing options enables these clinics to provide timely care and reduce the risk of transmission within the community. Research laboratories play a pivotal role in advancing our understanding of enteroviruses and developing new diagnostic and therapeutic approaches. In these settings, enteroviruses testing kits are used for a variety of purposes, including epidemiological studies, vaccine development, and the evaluation of new antiviral drugs. RT-PCR is particularly valuable in research laboratories due to its ability to provide detailed genetic information about enteroviruses, facilitating the study of viral evolution and the identification of potential targets for treatment. Furthermore, research laboratories often collaborate with healthcare institutions to monitor enterovirus outbreaks and assess the effectiveness of public health interventions. In summary, the Global Enteroviruses Testing Kit Market serves a wide range of applications across hospitals, specialty clinics, and research laboratories. Each of these settings has unique requirements and challenges, and the availability of diverse testing options ensures that healthcare providers and researchers can effectively address the complexities of enterovirus infections. As the demand for accurate and efficient diagnostics continues to grow, the role of enteroviruses testing kits in these areas will remain critical in improving patient care and advancing scientific knowledge.

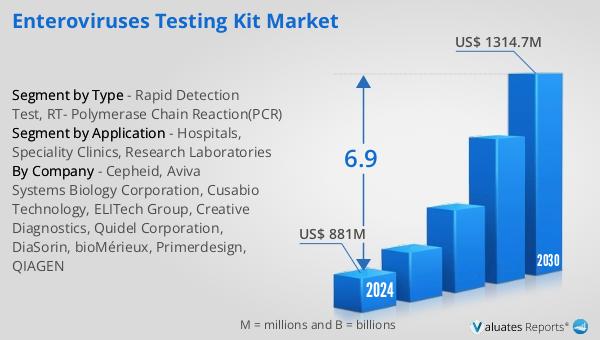

Global Enteroviruses Testing Kit Market Outlook:

The global market for Enteroviruses Testing Kits is anticipated to experience significant growth over the coming years. Starting from a valuation of approximately US$ 881 million in 2024, it is expected to reach around US$ 1314.7 million by 2030. This growth trajectory represents a Compound Annual Growth Rate (CAGR) of 6.9% throughout the forecast period. This upward trend is indicative of the increasing demand for effective diagnostic solutions in the healthcare sector, driven by the rising prevalence of enterovirus infections worldwide. The expansion of healthcare infrastructure, particularly in emerging economies, is also contributing to the market's growth, as more healthcare facilities adopt advanced diagnostic technologies to improve patient outcomes. The projected growth of the Enteroviruses Testing Kit market underscores the importance of early and accurate diagnosis in managing enterovirus infections. As healthcare providers and laboratories seek more efficient and reliable testing solutions, the demand for enteroviruses testing kits is expected to rise. This growth presents significant opportunities for manufacturers and stakeholders in the industry to innovate and expand their product offerings to meet the evolving needs of the market. Additionally, the increasing awareness of the importance of timely diagnosis and the implementation of public health initiatives to control enterovirus outbreaks are likely to further drive the market's expansion. In conclusion, the Enteroviruses Testing Kit market is poised for substantial growth in the coming years, driven by a combination of factors including rising infection rates, advancements in diagnostic technologies, and the expansion of healthcare infrastructure. As the market continues to evolve, stakeholders will need to focus on innovation and collaboration to address the growing demand for efficient and accurate diagnostic solutions.

| Report Metric | Details |

| Report Name | Enteroviruses Testing Kit Market |

| Accounted market size in 2024 | US$ 881 million |

| Forecasted market size in 2030 | US$ 1314.7 million |

| CAGR | 6.9 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Segment by Region |

|

| By Company | Cepheid, Aviva Systems Biology Corporation, Cusabio Technology, ELITech Group, Creative Diagnostics, Quidel Corporation, DiaSorin, bioMérieux, Primerdesign, QIAGEN |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |