What is Global High Alumina Refractory Material Market?

The Global High Alumina Refractory Material Market is a specialized segment within the broader refractory materials industry. Refractory materials are substances that are resistant to high temperatures and are used in applications that require extreme heat resistance. High alumina refractory materials, in particular, are composed of aluminum oxide (Al2O3) and are known for their ability to withstand high temperatures, chemical corrosion, and mechanical wear. These materials are essential in industries such as steel, cement, glass, and ceramics, where they are used to line furnaces, kilns, incinerators, and reactors. The demand for high alumina refractory materials is driven by the need for durable and efficient materials that can enhance the performance and longevity of high-temperature industrial processes. As industries continue to evolve and seek more efficient and sustainable solutions, the global market for high alumina refractory materials is expected to grow, driven by advancements in technology and increasing industrial activities worldwide.

0.4, 0.55, 0.7, 0.8, Other in the Global High Alumina Refractory Material Market:

High alumina refractory materials are categorized based on their alumina content, which significantly influences their properties and applications. The categories include 0.4, 0.55, 0.7, 0.8, and other alumina content levels. The 0.4 category, which contains approximately 40% alumina, is typically used in applications where moderate heat resistance is required. These materials are often employed in the construction of industrial kilns and furnaces where temperatures do not exceed certain thresholds. The 0.55 category, with around 55% alumina, offers better heat resistance and is suitable for more demanding applications such as lining steel furnaces and cement kilns. The 0.7 category, containing about 70% alumina, provides even higher resistance to heat and chemical corrosion, making it ideal for use in environments with extreme temperatures and aggressive chemical reactions. This category is commonly used in the glass and ceramics industries, where the materials must withstand both high temperatures and corrosive substances. The 0.8 category, with 80% alumina content, represents some of the highest quality refractory materials available. These materials are used in the most demanding industrial applications, such as in the production of high-purity metals and advanced ceramics. They offer exceptional heat resistance, mechanical strength, and durability. Other categories of high alumina refractory materials may include specialized formulations with varying alumina content and additional components to enhance specific properties. These materials are tailored for niche applications that require unique performance characteristics. The choice of alumina content in refractory materials is crucial as it directly impacts their thermal stability, mechanical strength, and resistance to chemical attack. Industries select the appropriate category based on the specific requirements of their processes, ensuring optimal performance and longevity of their equipment. As technology advances and industrial processes become more sophisticated, the demand for high-quality refractory materials with precise alumina content is expected to increase, driving innovation and growth in the global high alumina refractory material market.

Special Road & Construction, Industry Kiln, Sewer Applications, Other in the Global High Alumina Refractory Material Market:

High alumina refractory materials are extensively used in various applications due to their exceptional heat resistance, mechanical strength, and durability. In the area of special road and construction, these materials are utilized in the construction of high-temperature resistant structures such as tunnels, bridges, and other infrastructure projects that require materials capable of withstanding extreme conditions. Their ability to endure high temperatures and resist chemical corrosion makes them ideal for use in environments where traditional construction materials would fail. In industrial kilns, high alumina refractory materials are essential for lining the interiors of these high-temperature processing units. Kilns used in the production of ceramics, cement, and glass rely on these materials to maintain structural integrity and efficiency under intense heat. The refractory lining protects the kiln's structure from thermal damage and ensures consistent temperature control, which is crucial for the quality of the final product. In sewer applications, high alumina refractory materials are used to line sewer pipes and other components exposed to harsh chemical environments. These materials provide excellent resistance to chemical corrosion and abrasion, ensuring the longevity and reliability of sewer systems. Their use in this area helps prevent leaks and structural failures, contributing to the overall efficiency and safety of wastewater management systems. Other applications of high alumina refractory materials include their use in the production of high-purity metals, advanced ceramics, and various high-temperature industrial processes. These materials are chosen for their ability to withstand extreme conditions and provide reliable performance over extended periods. Their versatility and durability make them indispensable in industries that require materials capable of enduring harsh environments and maintaining their integrity under stress. As industries continue to seek more efficient and sustainable solutions, the demand for high alumina refractory materials is expected to grow, driven by their proven performance and adaptability in a wide range of applications.

Global High Alumina Refractory Material Market Outlook:

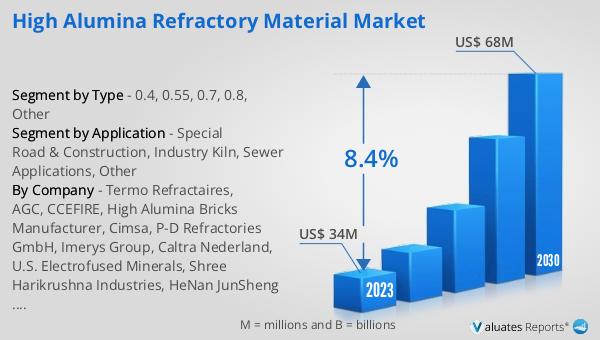

The global High Alumina Refractory Material market was valued at US$ 34 million in 2023 and is anticipated to reach US$ 68 million by 2030, witnessing a CAGR of 8.4% during the forecast period 2024-2030. This significant growth reflects the increasing demand for high-performance refractory materials across various industries. The market's expansion is driven by the need for materials that can withstand extreme temperatures and harsh chemical environments, ensuring the efficiency and longevity of industrial processes. As industries such as steel, cement, glass, and ceramics continue to evolve and expand, the demand for high alumina refractory materials is expected to rise. These materials play a crucial role in enhancing the performance and durability of high-temperature processing units, contributing to the overall efficiency and productivity of industrial operations. The projected growth of the market underscores the importance of high alumina refractory materials in modern industrial applications and highlights the ongoing advancements in material science and technology that are driving innovation and development in this field.

| Report Metric | Details |

| Report Name | High Alumina Refractory Material Market |

| Accounted market size in 2023 | US$ 34 million |

| Forecasted market size in 2030 | US$ 68 million |

| CAGR | 8.4% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Termo Refractaires, AGC, CCEFIRE, High Alumina Bricks Manufacturer, Cimsa, P-D Refractories GmbH, Imerys Group, Caltra Nederland, U.S. Electrofused Minerals, Shree Harikrushna Industries, HeNan JunSheng Refractories Limited, Zhengzhou Dengfeng Smelting Materials |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |