What is Global Home and Office Water Delivery Service Market?

The Global Home and Office Water Delivery Service Market refers to the industry that provides water delivery services to both residential homes and commercial offices. This market includes the delivery of bottled water, water coolers, and other related services. The primary goal is to ensure that customers have access to clean, safe, and convenient drinking water. Companies in this market offer various subscription plans, allowing customers to receive regular deliveries of water based on their consumption needs. This service is particularly beneficial in areas where tap water quality is questionable or where there is a high demand for purified water. The market has seen significant growth due to increasing health consciousness among consumers and the convenience offered by these delivery services. Additionally, the rise in remote working and the need for home office setups have further fueled the demand for home water delivery services.

Water Cooler Service, Bottled Water Delivery in the Global Home and Office Water Delivery Service Market:

Water Cooler Service and Bottled Water Delivery are two key components of the Global Home and Office Water Delivery Service Market. Water cooler services involve the rental or purchase of water dispensers that can be placed in homes or offices. These coolers are typically equipped with both hot and cold water dispensing options, making them versatile for various needs. The service providers ensure that the water coolers are regularly maintained, cleaned, and refilled with fresh water. This eliminates the hassle for customers to manage the upkeep of the coolers themselves. Bottled water delivery, on the other hand, involves the regular delivery of large water bottles, usually ranging from 5 to 20 liters, to homes and offices. These bottles are often used in conjunction with water coolers or dispensers. The bottled water is sourced from natural springs or purified through advanced filtration processes to ensure its quality and safety. Customers can choose from a variety of water types, including spring water, purified water, and mineral water, based on their preferences. The delivery schedules are flexible, allowing customers to receive water on a weekly, bi-weekly, or monthly basis. This service is particularly advantageous for offices where there is a high demand for drinking water throughout the day. It ensures that employees have access to clean and safe drinking water, which can contribute to their overall well-being and productivity. In households, bottled water delivery is convenient for families who prefer not to rely on tap water for drinking purposes. It provides a reliable source of clean water, especially in areas where tap water quality is inconsistent. The convenience of having water delivered directly to the doorstep saves time and effort for busy households. Additionally, the use of water coolers and bottled water delivery services can reduce the reliance on single-use plastic bottles, contributing to environmental sustainability. Many service providers also offer recycling programs for the used water bottles, further promoting eco-friendly practices. Overall, the combination of water cooler services and bottled water delivery offers a comprehensive solution for ensuring access to clean and safe drinking water in both homes and offices.

Offices, Households in the Global Home and Office Water Delivery Service Market:

The usage of Global Home and Office Water Delivery Service Market in offices and households is extensive and multifaceted. In offices, the presence of water coolers and regular bottled water delivery ensures that employees have constant access to clean drinking water. This is crucial for maintaining hydration, which can significantly impact productivity and overall health. Many offices opt for water coolers with both hot and cold water options, allowing employees to make beverages like tea or coffee easily. The convenience of having water readily available reduces the need for employees to leave the office premises to purchase bottled water, thereby saving time and increasing efficiency. Additionally, providing clean drinking water is a basic amenity that can enhance employee satisfaction and contribute to a positive work environment. In households, the demand for water delivery services has surged, especially with the increasing awareness of the importance of drinking clean and purified water. Families prefer bottled water delivery services as it ensures a consistent supply of high-quality water without the need to rely on tap water, which may not always be safe for consumption. Water coolers in homes offer the added benefit of providing both hot and cold water, making it convenient for various household needs, from cooking to making hot beverages. The regular delivery schedules offered by service providers mean that households never run out of drinking water, adding to the convenience. Moreover, the use of water delivery services in homes can be particularly beneficial for elderly individuals or those with mobility issues, as it eliminates the need to carry heavy water bottles from stores. The environmental aspect is also a significant consideration for many households. By opting for water delivery services, families can reduce their reliance on single-use plastic bottles, thereby contributing to environmental sustainability. Many service providers also offer recycling programs for the used water bottles, ensuring that they are disposed of responsibly. In summary, the Global Home and Office Water Delivery Service Market plays a vital role in ensuring access to clean and safe drinking water in both offices and households. The convenience, reliability, and environmental benefits offered by these services make them an attractive option for a wide range of consumers.

Global Home and Office Water Delivery Service Market Outlook:

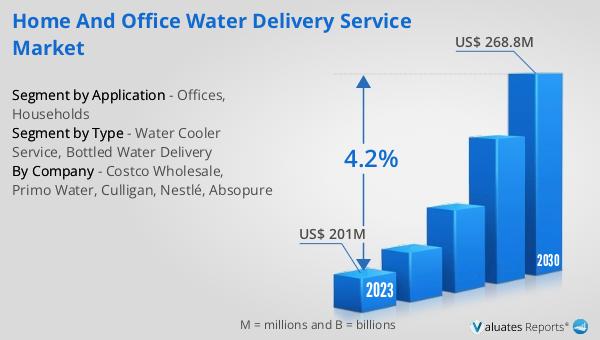

The global Home and Office Water Delivery Service market was valued at US$ 201 million in 2023 and is anticipated to reach US$ 268.8 million by 2030, witnessing a CAGR of 4.2% during the forecast period 2024-2030. This market growth reflects the increasing demand for convenient and reliable access to clean drinking water in both residential and commercial settings. The rising awareness about the health benefits of drinking purified water, coupled with the convenience of having water delivered directly to homes and offices, is driving this market expansion. The trend towards remote working and the need for home office setups have further contributed to the growth of the home water delivery segment. Additionally, the environmental benefits of reducing single-use plastic bottles through the use of large water containers and recycling programs offered by service providers are appealing to environmentally conscious consumers. The market's steady growth rate indicates a sustained demand for these services, highlighting their importance in modern lifestyles.

| Report Metric | Details |

| Report Name | Home and Office Water Delivery Service Market |

| Accounted market size in 2023 | US$ 201 million |

| Forecasted market size in 2030 | US$ 268.8 million |

| CAGR | 4.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Costco Wholesale, Primo Water, Culligan, Nestlé, Absopure |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |