What is Charging Pile - Global Market?

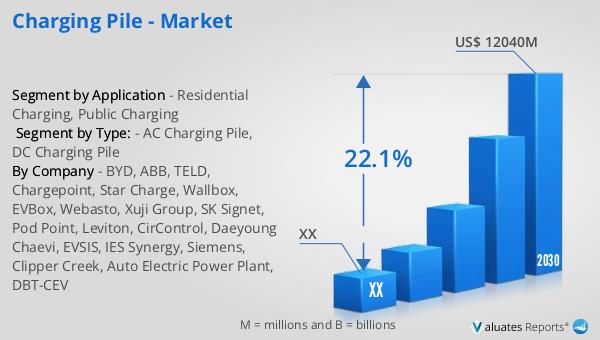

In the realm of electric vehicles (EVs), the Charging Pile - Global Market stands as a pivotal infrastructure component, facilitating the replenishment of EV batteries. Essentially, a charging pile is a specialized station equipped with connectors that link electric vehicles to an electricity source, enabling the charging of EV batteries. This market, which was valued at approximately US$ 2766.2 million in 2023, is on a trajectory to expand to US$ 12040 million by 2030, growing at a compound annual growth rate (CAGR) of 22.1% from 2024 to 2030. This growth is underpinned by the escalating adoption of electric vehicles worldwide, driven by a collective move towards sustainable and eco-friendly transportation options. The market is characterized by the presence of key players such as Star Charge, TELD, and ABB, among others, who collectively hold about 45% of the market share. Geographically, China emerges as the dominant player, accounting for approximately 60% of the market, followed by Europe and North America, which hold shares of about 20% and 15%, respectively. The DC charging pile segment, in particular, claims the largest share of the market, representing about 70% of the product types available. This segment's prominence is attributed to its faster charging capabilities compared to its AC counterpart, making it a preferred choice for many EV users and operators.

AC Charging Pile, DC Charging Pile in the Charging Pile - Global Market:

Diving deeper into the Charging Pile - Global Market, we find two primary types of charging piles: AC (Alternating Current) and DC (Direct Current) Charging Piles. AC Charging Piles, often found in residential settings, offer a slower charging speed, making them suitable for overnight charging or situations where time is not of the essence. On the other hand, DC Charging Piles are the powerhouses of the charging world, providing rapid charging capabilities that can significantly reduce charging times to as little as 30 minutes for a substantial charge. This makes them ideal for public charging stations and locations where quick turnaround times are crucial. The global market's expansion is closely tied to the increasing demand for electric vehicles, as consumers and businesses alike seek more sustainable and cost-effective transportation solutions. This surge in EV adoption has spurred the development and deployment of both AC and DC charging piles across various settings, from private homes to public parking lots, highways, and commercial establishments. Manufacturers and service providers are continuously innovating to improve charging technologies, reduce costs, and enhance user experiences, further propelling the market's growth. As the market evolves, the balance between AC and DC charging infrastructure, along with the integration of smart charging solutions and renewable energy sources, will be key factors shaping the future of electric vehicle charging.

Residential Charging, Public Charging in the Charging Pile - Global Market:

The Charging Pile - Global Market finds its applications sprawling across two main areas: Residential Charging and Public Charging. In residential settings, charging piles are typically of the AC type due to their lower installation costs and the convenience of overnight charging. This setup aligns with the daily routines of most EV owners, allowing them to recharge their vehicles in the comfort of their homes. On the flip side, public charging infrastructure predominantly features DC charging piles, catering to the need for quick recharge options while on the move. Public charging stations are strategically located in places like shopping centers, parking lots, and along major highways to provide easy access and minimal disruption to travel plans. The expansion of public charging networks is crucial to supporting the growing number of EVs on the road, addressing range anxiety, and facilitating longer journeys. As the market for electric vehicles continues to expand, the development of both residential and public charging solutions is paramount in creating a robust ecosystem that supports the transition to electric mobility. The interplay between these two charging options forms the backbone of the EV charging infrastructure, ensuring that the needs of all EV users are met, whether at home or away.

Charging Pile - Global Market Outlook:

The outlook for the Charging Pile - Global Market is decidedly optimistic, with projections indicating a significant growth trajectory from US$ 2766.2 million in 2023 to an impressive US$ 12040 million by 2030. This growth, characterized by a robust CAGR of 22.1% during the forecast period of 2024-2030, underscores the burgeoning demand for electric vehicle (EV) charging infrastructure amidst the global shift towards sustainable transportation. The market is buoyed by the contributions of leading manufacturers such as Star Charge, TELD, and ABB, which collectively command a substantial market share of about 45%. Geographically, China stands out as the largest market, claiming around 60% of the global share, followed by Europe and North America with shares of approximately 20% and 15%, respectively. This distribution highlights the pivotal role of these regions in driving the adoption of EVs and, by extension, the demand for charging piles. Notably, the DC charging pile segment emerges as the dominant product category, capturing about 70% of the market. This preference for DC charging piles is largely attributed to their faster charging capabilities, which cater to the growing consumer expectation for convenience and efficiency in EV charging solutions. The market's expansion is further facilitated by ongoing technological advancements, government incentives, and increasing consumer awareness about the benefits of electric vehicles, setting the stage for a future where electric mobility is the norm.

| Report Metric | Details |

| Report Name | Charging Pile - Market |

| Forecasted market size in 2030 | US$ 12040 million |

| CAGR | 22.1% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | BYD, ABB, TELD, Chargepoint, Star Charge, Wallbox, EVBox, Webasto, Xuji Group, SK Signet, Pod Point, Leviton, CirControl, Daeyoung Chaevi, EVSIS, IES Synergy, Siemens, Clipper Creek, Auto Electric Power Plant, DBT-CEV |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |