What is Global Spinal Surgical Devices Market?

The Global Spinal Surgical Devices Market is a significant segment within the broader medical devices industry, focusing on the development and distribution of devices used in spinal surgeries. These devices are crucial for treating various spinal disorders, including degenerative disc diseases, spinal stenosis, and scoliosis, among others. The market encompasses a wide range of products, such as fusion devices, non-fusion devices, and spinal biologics, each designed to address specific surgical needs and patient conditions. The demand for spinal surgical devices is driven by factors such as the increasing prevalence of spinal disorders, advancements in surgical techniques, and the growing aging population, which is more susceptible to spinal issues. Additionally, technological innovations and the introduction of minimally invasive surgical procedures have further propelled the market's growth, making spinal surgeries safer and more effective. The market is characterized by intense competition among key players, who are continuously striving to enhance their product offerings and expand their geographical presence. Overall, the Global Spinal Surgical Devices Market plays a vital role in improving patient outcomes and enhancing the quality of life for individuals suffering from spinal conditions.

Fusion Devices, Non-Fusion Devices in the Global Spinal Surgical Devices Market:

Fusion devices and non-fusion devices are two primary categories within the Global Spinal Surgical Devices Market, each serving distinct purposes in spinal surgeries. Fusion devices are designed to stabilize and fuse two or more vertebrae, providing support and reducing pain caused by spinal instability or deformities. These devices include spinal plates, screws, rods, and cages, which are often used in procedures like spinal fusion surgery. The goal of fusion devices is to create a solid bone mass that eliminates motion between the affected vertebrae, thereby alleviating pain and preventing further degeneration. On the other hand, non-fusion devices, also known as motion preservation devices, aim to maintain the natural movement of the spine while providing stability. These devices include artificial discs, dynamic stabilization devices, and interspinous process devices. Non-fusion devices are typically used in cases where preserving spinal mobility is crucial, such as in younger patients or those with specific lifestyle needs. The choice between fusion and non-fusion devices depends on various factors, including the patient's age, overall health, and the specific spinal condition being treated. Both types of devices have their advantages and limitations, and the decision is often made based on a thorough evaluation of the patient's condition and the surgeon's expertise. In recent years, there has been a growing interest in non-fusion devices due to their potential to preserve spinal motion and reduce the risk of adjacent segment disease, a condition where the segments above or below a spinal fusion develop problems over time. However, fusion devices remain a mainstay in spinal surgeries, particularly for conditions where stability is paramount. The development of new materials and technologies has also contributed to the evolution of both fusion and non-fusion devices, with innovations such as bioresorbable materials and 3D-printed implants offering new possibilities for patient care. As the Global Spinal Surgical Devices Market continues to evolve, the interplay between fusion and non-fusion devices will remain a critical area of focus, with ongoing research and development efforts aimed at improving patient outcomes and expanding the range of treatment options available to surgeons.

Hospitals, Ambulatory Surgical Centers, Specialty Clinics, Others in the Global Spinal Surgical Devices Market:

The usage of Global Spinal Surgical Devices Market spans across various healthcare settings, including hospitals, ambulatory surgical centers, specialty clinics, and others, each playing a crucial role in delivering spinal care to patients. Hospitals are the primary setting for spinal surgeries, offering comprehensive care with access to advanced surgical equipment and multidisciplinary teams. They are equipped to handle complex spinal procedures, including those requiring extended hospital stays and intensive postoperative care. Hospitals also serve as centers for training and research, contributing to the development of new surgical techniques and devices. Ambulatory surgical centers (ASCs) provide an alternative setting for spinal surgeries, particularly for minimally invasive procedures that allow for same-day discharge. ASCs offer a more cost-effective and convenient option for patients, with shorter wait times and a focus on outpatient care. The use of spinal surgical devices in ASCs has increased with advancements in minimally invasive techniques, which reduce the need for prolonged hospitalization. Specialty clinics, often led by orthopedic or neurosurgical specialists, focus on specific spinal conditions and offer personalized care tailored to individual patient needs. These clinics may provide a range of services, from diagnostic evaluations to surgical interventions, and often collaborate with hospitals and ASCs to ensure comprehensive care. Other settings, such as rehabilitation centers and pain management clinics, also play a role in the continuum of care for spinal patients, offering postoperative support and non-surgical treatment options. The integration of spinal surgical devices across these various settings highlights the importance of a coordinated approach to spinal care, ensuring that patients receive the most appropriate and effective treatment for their condition. As the Global Spinal Surgical Devices Market continues to grow, the collaboration between different healthcare providers and the adoption of innovative technologies will be key to improving patient outcomes and expanding access to spinal care.

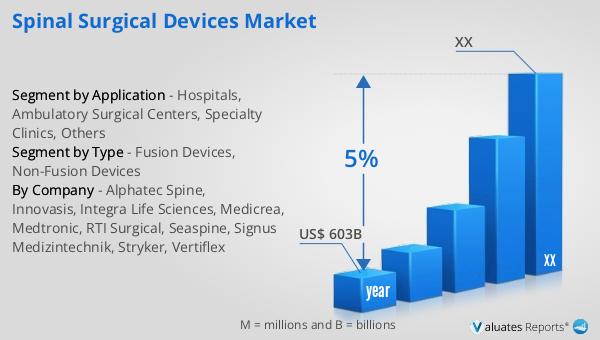

Global Spinal Surgical Devices Market Outlook:

Our research indicates that the global market for medical devices, which includes spinal surgical devices, is projected to reach approximately $603 billion in 2023. This market is expected to experience a steady growth rate, with a compound annual growth rate (CAGR) of 5% over the next six years. This growth is driven by several factors, including the increasing prevalence of chronic diseases, advancements in medical technology, and the rising demand for minimally invasive procedures. The medical devices market encompasses a wide range of products, from diagnostic equipment to surgical instruments, each playing a vital role in patient care and treatment. The Global Spinal Surgical Devices Market is a significant contributor to this overall market, with innovations in spinal surgery techniques and devices driving demand. As healthcare systems worldwide continue to evolve, the need for advanced medical devices that improve patient outcomes and enhance the quality of care will remain a priority. The projected growth of the medical devices market reflects the ongoing efforts of manufacturers, healthcare providers, and researchers to address the diverse needs of patients and improve healthcare delivery. With a focus on innovation and collaboration, the medical devices industry is poised to make significant strides in the coming years, benefiting patients and healthcare systems alike.

| Report Metric | Details |

| Report Name | Spinal Surgical Devices Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Segment by Region |

|

| By Company | Integra Life Sciences, Medicrea, Medtronic, RTI Surgical, Seaspine, Signus Medizintechnik, Stryker, Vertiflex |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |