What is Slurry Mixing and Distribution System - Global Market?

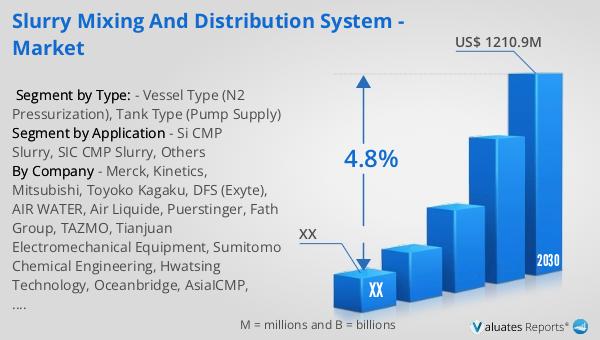

Slurry mixing and distribution systems are integral components in various industrial processes, designed to handle the preparation and conveyance of slurry—a semi-liquid mixture typically composed of fine particles suspended in a liquid. These systems are crucial in industries such as mining, wastewater treatment, and chemical processing, where they facilitate the efficient handling and transport of slurry materials. The global market for slurry mixing and distribution systems was valued at approximately US$ 848 million in 2023. It is projected to grow to a revised size of US$ 1210.9 million by 2030, reflecting a compound annual growth rate (CAGR) of 4.8% during the forecast period from 2024 to 2030. This growth is driven by the increasing demand for efficient material handling solutions in various sectors, coupled with advancements in technology that enhance the performance and reliability of these systems. As industries continue to seek ways to optimize their operations and reduce costs, the adoption of advanced slurry mixing and distribution systems is expected to rise, further propelling market growth.

Vessel Type (N2 Pressurization), Tank Type (Pump Supply) in the Slurry Mixing and Distribution System - Global Market:

In the realm of slurry mixing and distribution systems, two prominent configurations are the Vessel Type (N2 Pressurization) and Tank Type (Pump Supply) systems. The Vessel Type system employs nitrogen pressurization to facilitate the movement of slurry. This method involves using a pressurized vessel where nitrogen gas is introduced to create a pressure differential, propelling the slurry through the system. This type of system is particularly advantageous in applications requiring precise control over slurry flow and pressure, as the use of nitrogen allows for fine-tuning of these parameters. Additionally, the inert nature of nitrogen ensures that the slurry remains uncontaminated, making it ideal for sensitive applications in industries such as semiconductor manufacturing, where purity is paramount. On the other hand, the Tank Type system relies on pump supply to move slurry. This configuration typically involves a storage tank equipped with pumps that draw slurry from the tank and distribute it to the desired location. The pump supply method is favored for its simplicity and cost-effectiveness, making it a popular choice in industries where large volumes of slurry need to be handled efficiently. The choice between these two systems often depends on the specific requirements of the application, including factors such as the nature of the slurry, the required flow rate, and the level of control needed over the distribution process. Both systems have their unique advantages and are employed in various industries to optimize slurry handling and distribution.

Si CMP Slurry, SIC CMP Slurry, Others in the Slurry Mixing and Distribution System - Global Market:

Slurry mixing and distribution systems find extensive applications in the semiconductor industry, particularly in the preparation and handling of Chemical Mechanical Planarization (CMP) slurries. CMP is a critical process in semiconductor manufacturing, used to smooth and flatten the surfaces of wafers. Si CMP slurry, which is used for silicon wafer polishing, requires precise mixing and distribution to ensure uniformity and consistency in the polishing process. The slurry mixing and distribution system plays a vital role in maintaining the quality of the Si CMP slurry by ensuring that the abrasive particles are evenly suspended in the liquid medium. Similarly, SIC CMP slurry, used for silicon carbide wafer polishing, also relies on efficient slurry mixing and distribution systems. Silicon carbide is a harder material compared to silicon, necessitating the use of specialized slurries with different abrasive properties. The slurry mixing and distribution system ensures that the SIC CMP slurry is properly prepared and delivered to the polishing equipment, enabling precise control over the polishing process. In addition to Si and SIC CMP slurries, slurry mixing and distribution systems are also used in other applications, such as the preparation of slurries for chemical processing and wastewater treatment. In these applications, the systems are designed to handle a wide range of slurry compositions, ensuring that the slurry is properly mixed and distributed to achieve the desired processing outcomes. The versatility and efficiency of slurry mixing and distribution systems make them indispensable in various industrial processes, where they contribute to improved product quality and operational efficiency.

Slurry Mixing and Distribution System - Global Market Outlook:

The global market for slurry mixing and distribution systems was valued at approximately US$ 848 million in 2023, with projections indicating a growth to US$ 1210.9 million by 2030. This anticipated growth, at a compound annual growth rate (CAGR) of 4.8% from 2024 to 2030, underscores the increasing importance of these systems across various industries. Slurry mixing and distribution systems are essential in sectors such as mining, wastewater treatment, and chemical processing, where they facilitate the efficient handling and transport of slurry materials. The demand for these systems is driven by the need for efficient material handling solutions that can optimize operations and reduce costs. Technological advancements have further enhanced the performance and reliability of slurry mixing and distribution systems, making them more attractive to industries seeking to improve their operational efficiency. As industries continue to evolve and seek ways to enhance their processes, the adoption of advanced slurry mixing and distribution systems is expected to rise, contributing to the overall growth of the market.

| Report Metric | Details |

| Report Name | Slurry Mixing and Distribution System - Market |

| Forecasted market size in 2030 | US$ 1210.9 million |

| CAGR | 4.8% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Merck, Kinetics, Mitsubishi, Toyoko Kagaku, DFS (Exyte), AIR WATER, Air Liquide, Puerstinger, Fath Group, TAZMO, Tianjuan Electromechanical Equipment, Sumitomo Chemical Engineering, Hwatsing Technology, Oceanbridge, AsiaICMP, PLUSENG, Axus Technology, SCREEN SPE Service, PLUS TECH, TRUSVAL TECHNOLOGY, GMC Semitech |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |