What is Global Miniature Deep Groove Ball Bearing Market?

The Global Miniature Deep Groove Ball Bearing Market is a specialized segment within the broader bearings industry, focusing on small-sized bearings that are essential for various applications requiring precision and efficiency. These miniature bearings are characterized by their small size and ability to handle both radial and axial loads, making them versatile components in many mechanical systems. They are widely used in industries such as automotive, telecommunications, and household appliances, where space constraints and high performance are critical. The market for these bearings is driven by the increasing demand for compact and efficient machinery, as well as advancements in technology that require precise and reliable components. As industries continue to innovate and miniaturize their products, the need for miniature deep groove ball bearings is expected to grow. These bearings are designed to operate at high speeds with minimal friction, contributing to the overall efficiency and longevity of the machinery in which they are used. The market is also influenced by factors such as the rise in automation, the growth of the electric vehicle sector, and the increasing use of smart devices, all of which require high-quality bearings to function effectively.

Single Row Groove Ball Bearing, Double Row Groove Ball Bearing in the Global Miniature Deep Groove Ball Bearing Market:

Single Row Groove Ball Bearings and Double Row Groove Ball Bearings are two primary types of bearings within the Global Miniature Deep Groove Ball Bearing Market, each serving distinct purposes based on their design and application requirements. Single Row Groove Ball Bearings are the most common type and are designed to support radial loads and moderate axial loads in both directions. They consist of a single row of balls, which allows them to operate at high speeds with low friction. These bearings are typically used in applications where space is limited, and high-speed operation is necessary, such as in small motors and various household appliances. Their simple design makes them easy to install and maintain, contributing to their widespread use across different industries. On the other hand, Double Row Groove Ball Bearings are designed to handle higher radial loads and axial loads in both directions compared to their single-row counterparts. They consist of two rows of balls, which provide greater load-carrying capacity and stability. This makes them suitable for applications where higher load capacity is required, such as in industrial machinery and automotive components. The double-row design also offers enhanced rigidity, making these bearings ideal for applications that experience high levels of vibration or shock loads. In the context of the Global Miniature Deep Groove Ball Bearing Market, both single and double-row bearings play crucial roles in meeting the diverse needs of various industries. The choice between single and double-row bearings depends on factors such as load requirements, space constraints, and the specific operational conditions of the application. As industries continue to evolve and demand more efficient and compact solutions, the development and innovation of these bearings are expected to advance, providing even more specialized options to meet the growing needs of the market. The versatility and adaptability of both single and double-row groove ball bearings ensure their continued relevance and importance in the global market, as they contribute to the efficiency and reliability of countless mechanical systems worldwide.

Small Motors, Telecommunications Equipment, Automotive, Industrial Machinery, Household Electrical Appliances, Others in the Global Miniature Deep Groove Ball Bearing Market:

The Global Miniature Deep Groove Ball Bearing Market finds extensive usage across various sectors, including small motors, telecommunications equipment, automotive, industrial machinery, household electrical appliances, and others, each benefiting from the unique properties of these bearings. In small motors, miniature deep groove ball bearings are essential for ensuring smooth and efficient operation. These motors are used in a wide range of applications, from household appliances to industrial equipment, where reliability and performance are crucial. The bearings help reduce friction and wear, allowing the motors to operate at high speeds with minimal energy loss. In telecommunications equipment, these bearings play a vital role in the functioning of devices such as routers, switches, and other networking hardware. The precision and low noise levels of miniature deep groove ball bearings make them ideal for use in environments where signal clarity and reliability are paramount. In the automotive industry, these bearings are used in various components, including electric motors, alternators, and steering systems. Their ability to handle both radial and axial loads makes them suitable for the demanding conditions of automotive applications, where durability and performance are essential. In industrial machinery, miniature deep groove ball bearings are used in equipment such as conveyors, pumps, and compressors, where they contribute to the smooth and efficient operation of the machinery. Their high load-carrying capacity and ability to operate at high speeds make them indispensable in industrial settings. In household electrical appliances, these bearings are used in products such as washing machines, vacuum cleaners, and fans, where they help reduce noise and improve energy efficiency. The compact size and high performance of miniature deep groove ball bearings make them ideal for use in these applications, where space and efficiency are critical considerations. Other areas where these bearings are used include medical devices, robotics, and aerospace applications, where precision and reliability are of utmost importance. The versatility and adaptability of miniature deep groove ball bearings make them a vital component in a wide range of applications, contributing to the efficiency and reliability of countless products and systems worldwide.

Global Miniature Deep Groove Ball Bearing Market Outlook:

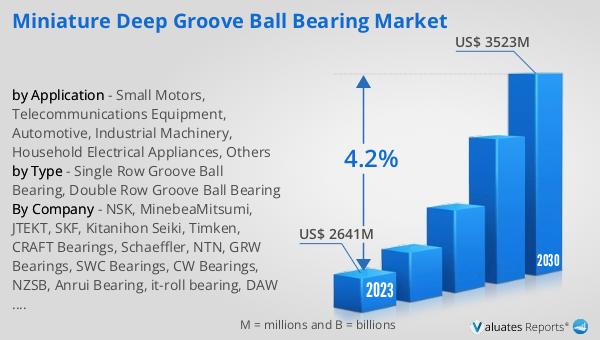

The outlook for the Global Miniature Deep Groove Ball Bearing Market is promising, with significant growth anticipated over the coming years. In 2023, the market was valued at approximately US$ 2,641 million, reflecting its substantial presence in various industries. By 2030, it is expected to reach around US$ 3,523 million, indicating a steady growth trajectory with a compound annual growth rate (CAGR) of 4.2% during the forecast period from 2024 to 2030. This growth can be attributed to several factors, including the increasing demand for compact and efficient machinery across different sectors. As industries continue to innovate and develop new technologies, the need for high-quality, reliable components like miniature deep groove ball bearings becomes more critical. The rise in automation, the growth of the electric vehicle sector, and the increasing use of smart devices are all contributing to the expanding market for these bearings. Additionally, the ongoing trend towards miniaturization in various industries is driving the demand for smaller, more efficient components, further boosting the market for miniature deep groove ball bearings. As a result, manufacturers are focusing on developing advanced bearing solutions that meet the evolving needs of their customers, ensuring the continued growth and success of the market in the years to come.

| Report Metric | Details |

| Report Name | Miniature Deep Groove Ball Bearing Market |

| Accounted market size in 2023 | US$ 2641 million |

| Forecasted market size in 2030 | US$ 3523 million |

| CAGR | 4.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | NSK, MinebeaMitsumi, JTEKT, SKF, Kitanihon Seiki, Timken, CRAFT Bearings, Schaeffler, NTN, GRW Bearings, SWC Bearings, CW Bearings, NZSB, Anrui Bearing, it-roll bearing, DAW Bearing, YITONG INDUSTRY, Dongqing Precision Bearing |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |