What is 3D Surface Vision and Inspection - Global Market?

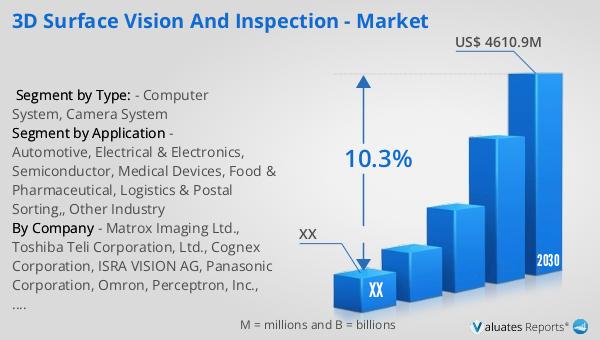

3D Surface Vision and Inspection is a cutting-edge technology that plays a crucial role in the global market by enabling the precise inspection and measurement of complex, free-formed surfaces. This technology utilizes advanced imaging techniques to capture detailed three-dimensional data, which is essential for quality control and assurance in various industries. By providing accurate and reliable surface measurements, 3D Surface Vision and Inspection helps manufacturers ensure that their products meet stringent quality standards. This technology is particularly valuable in industries where precision and accuracy are paramount, such as automotive, electronics, and medical devices. The global market for 3D Surface Vision and Inspection was valued at approximately US$ 2365 million in 2023, and it is projected to grow significantly, reaching an estimated size of US$ 4610.9 million by 2030. This growth is driven by a compound annual growth rate (CAGR) of 10.3% during the forecast period from 2024 to 2030. The North American market is also expected to experience substantial growth, reflecting the increasing demand for advanced inspection solutions across various sectors. As industries continue to prioritize quality and efficiency, the adoption of 3D Surface Vision and Inspection technology is likely to expand further.

Computer System, Camera System in the 3D Surface Vision and Inspection - Global Market:

The computer system and camera system are integral components of the 3D Surface Vision and Inspection technology, forming the backbone of its functionality in the global market. The computer system serves as the processing unit, where the captured data is analyzed and interpreted. It is equipped with sophisticated software that can handle complex algorithms to process the three-dimensional data collected by the camera system. This software is designed to identify defects, measure dimensions, and ensure that the surfaces meet the required specifications. The computer system's ability to process large volumes of data quickly and accurately is crucial for maintaining the efficiency and effectiveness of the inspection process. On the other hand, the camera system is responsible for capturing the three-dimensional images of the surfaces being inspected. It utilizes advanced imaging technologies, such as laser triangulation, structured light, or stereo vision, to create detailed 3D models of the surfaces. These cameras are capable of capturing high-resolution images, which are essential for detecting even the smallest defects or deviations from the desired specifications. The integration of the camera system with the computer system allows for real-time analysis and feedback, enabling manufacturers to make immediate adjustments to their production processes if necessary. This synergy between the computer and camera systems is what makes 3D Surface Vision and Inspection a powerful tool for quality control and assurance. The global market for these systems is driven by the increasing demand for high-quality products and the need for efficient inspection solutions. As industries continue to evolve and adopt more advanced technologies, the role of computer and camera systems in 3D Surface Vision and Inspection is expected to become even more significant. The ability to provide accurate and reliable inspection results is crucial for maintaining competitiveness in today's fast-paced market. Moreover, the flexibility and adaptability of these systems make them suitable for a wide range of applications, from automotive manufacturing to semiconductor production. The continuous advancements in imaging technologies and data processing capabilities are likely to further enhance the performance and capabilities of 3D Surface Vision and Inspection systems, driving their adoption across various industries. As a result, the global market for these systems is poised for substantial growth in the coming years, reflecting the increasing importance of quality control and assurance in modern manufacturing processes.

Automotive, Electrical & Electronics, Semiconductor, Medical Devices, Food & Pharmaceutical, Logistics & Postal Sorting,, Other Industry in the 3D Surface Vision and Inspection - Global Market:

The application of 3D Surface Vision and Inspection technology spans across various industries, each benefiting from its ability to provide precise and reliable inspection and measurement solutions. In the automotive industry, this technology is used to ensure that components and assemblies meet stringent quality standards. By capturing detailed 3D images of parts, manufacturers can detect defects, measure dimensions, and verify that components fit together correctly. This is crucial for maintaining the safety and performance of vehicles. In the electrical and electronics industry, 3D Surface Vision and Inspection is used to inspect circuit boards, connectors, and other components. The technology helps identify defects such as misalignments, soldering issues, and surface irregularities, ensuring that electronic devices function properly. The semiconductor industry also relies on this technology for inspecting wafers and chips. The ability to detect minute defects and deviations is essential for maintaining the performance and reliability of semiconductor devices. In the medical devices industry, 3D Surface Vision and Inspection is used to ensure that products meet strict regulatory standards. The technology is used to inspect components such as implants, surgical instruments, and diagnostic equipment, ensuring that they are safe and effective for use. In the food and pharmaceutical industry, this technology is used to inspect packaging and ensure that products are free from contamination. The ability to detect defects and ensure that packaging is sealed correctly is crucial for maintaining product safety and quality. In logistics and postal sorting, 3D Surface Vision and Inspection is used to automate the sorting process, ensuring that packages are sorted accurately and efficiently. This technology helps reduce errors and improve the speed and accuracy of the sorting process. Other industries, such as aerospace and defense, also benefit from the use of 3D Surface Vision and Inspection technology. The ability to provide precise and reliable inspection solutions is crucial for maintaining the safety and performance of products in these industries. As the demand for high-quality products continues to grow, the adoption of 3D Surface Vision and Inspection technology is expected to expand further, driving growth in the global market.

3D Surface Vision and Inspection - Global Market Outlook:

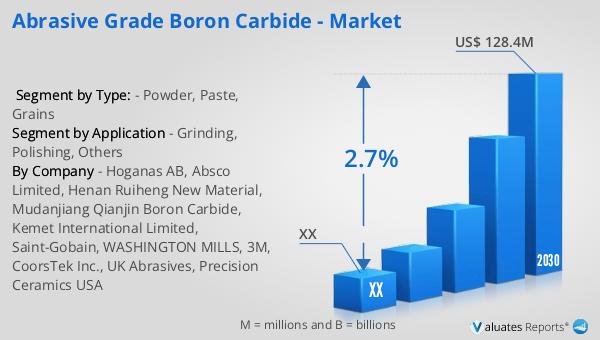

The 3D Surface Vision and Inspection technology is predominantly utilized for the three-dimensional inspection and measurement of intricate, free-formed surfaces. In 2023, the global market for this technology was valued at approximately US$ 2365 million. It is anticipated to grow to a revised size of US$ 4610.9 million by 2030, driven by a compound annual growth rate (CAGR) of 10.3% during the forecast period from 2024 to 2030. This growth reflects the increasing demand for advanced inspection solutions across various industries. The North American market for 3D Surface Vision and Inspection is also expected to witness significant growth, although specific figures for this region were not provided. The technology's ability to provide accurate and reliable inspection results is crucial for maintaining competitiveness in today's fast-paced market. As industries continue to prioritize quality and efficiency, the adoption of 3D Surface Vision and Inspection technology is likely to expand further. The continuous advancements in imaging technologies and data processing capabilities are expected to enhance the performance and capabilities of these systems, driving their adoption across various sectors. As a result, the global market for 3D Surface Vision and Inspection is poised for substantial growth in the coming years, reflecting the increasing importance of quality control and assurance in modern manufacturing processes.

| Report Metric | Details |

| Report Name | 3D Surface Vision and Inspection - Market |

| Forecasted market size in 2030 | US$ 4610.9 million |

| CAGR | 10.3% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Matrox Imaging Ltd., Toshiba Teli Corporation, Ltd., Cognex Corporation, ISRA VISION AG, Panasonic Corporation, Omron, Perceptron, Inc., Sharp Corporation, Edmund Optics, AMETEK, Inc., Teledyne Technologies, Keyence Corporation, Datalogic S.p.A., Sony Corporation, Basler AG, Vitronic GmbH, SICK AG, IMS Messsysteme GmbH, Industrial Vision Systems Ltd., Allied Vision Technologies, Baumer Group, Dark Field Technologies |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |