What is Business Background Check - Global Market?

Business background checks are an essential component of the global market landscape, serving as a critical tool for companies to assess the credibility and reliability of potential business partners, employees, and other stakeholders. These checks involve a comprehensive review of an entity's financial history, legal standing, and overall reputation. By conducting thorough background checks, businesses can mitigate risks associated with fraud, financial instability, and legal liabilities. This process not only helps in safeguarding a company's assets but also enhances decision-making by providing a clearer picture of the entities they are dealing with. In today's interconnected world, where businesses often operate across borders, the demand for reliable and efficient background check services has grown significantly. Companies are increasingly relying on these services to ensure compliance with international regulations and to maintain their reputation in the global market. As a result, the business background check market has become a vital component of the broader risk management and due diligence industry, offering a range of solutions tailored to meet the diverse needs of businesses worldwide.

Cloud-based, On-premise in the Business Background Check - Global Market:

In the realm of business background checks, two primary deployment models have emerged: cloud-based and on-premise solutions. Cloud-based background check services have gained significant traction due to their flexibility, scalability, and cost-effectiveness. These solutions allow businesses to access background check services via the internet, eliminating the need for extensive IT infrastructure and reducing upfront costs. Cloud-based services offer the advantage of real-time updates and seamless integration with other business applications, making them an attractive option for companies looking to streamline their operations. Additionally, the cloud model supports remote access, enabling businesses to conduct background checks from anywhere, which is particularly beneficial for organizations with a global presence. On the other hand, on-premise background check solutions provide businesses with greater control over their data and processes. These solutions are installed and operated on the company's own servers, offering a higher level of customization and security. For businesses that handle sensitive information or operate in highly regulated industries, on-premise solutions may be preferred due to the enhanced data protection they offer. However, they require a significant investment in IT infrastructure and ongoing maintenance, which can be a barrier for smaller companies. Despite these challenges, on-premise solutions remain a viable option for businesses that prioritize data security and control. As the business background check market continues to evolve, companies must carefully evaluate their specific needs and resources to determine the most suitable deployment model. Both cloud-based and on-premise solutions have their unique advantages and limitations, and the choice between them often depends on factors such as budget, regulatory requirements, and the level of IT expertise available within the organization. Ultimately, the decision should align with the company's overall business strategy and risk management objectives. By leveraging the right background check solution, businesses can enhance their due diligence processes, protect their interests, and build stronger, more trustworthy relationships with their partners and stakeholders.

Commercial, Government, Others in the Business Background Check - Global Market:

The application of business background checks spans various sectors, including commercial, government, and others, each with its unique requirements and challenges. In the commercial sector, background checks are primarily used to vet potential employees, partners, and suppliers. Companies conduct these checks to ensure that they are hiring trustworthy individuals and engaging with reputable entities. This process helps in minimizing risks associated with fraud, theft, and other unethical practices that could harm the business. For instance, a company might perform a background check on a new supplier to verify their financial stability and track record of delivering quality products. In the government sector, background checks are often more stringent due to the sensitive nature of the information and operations involved. Government agencies use background checks to screen employees, contractors, and vendors to ensure national security and compliance with regulatory standards. These checks are crucial in maintaining the integrity of government operations and protecting public interests. For example, a government agency might conduct a thorough background check on a contractor bidding for a defense project to ensure they have no ties to foreign adversaries. Beyond the commercial and government sectors, business background checks are also utilized in other areas such as non-profit organizations, educational institutions, and healthcare providers. In these sectors, background checks help in verifying the credentials and integrity of individuals and entities involved, thereby safeguarding the organization's reputation and ensuring compliance with industry standards. For example, a non-profit organization might conduct background checks on volunteers to ensure they have no criminal history that could jeopardize the safety of the people they serve. Overall, the use of business background checks across various sectors underscores their importance in fostering trust, transparency, and accountability in the global market.

Business Background Check - Global Market Outlook:

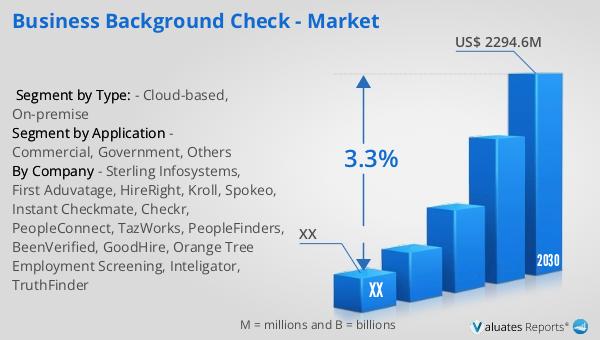

The global market for business background checks was valued at approximately $1,834 million in 2023, with projections indicating a growth to around $2,294.6 million by 2030. This growth is expected to occur at a compound annual growth rate (CAGR) of 3.3% from 2024 to 2030. This steady growth reflects the increasing demand for reliable background check services as businesses seek to mitigate risks and ensure compliance with regulatory standards. In North America, the market for business background checks was valued at a significant amount in 2023, with expectations of continued growth through 2030. The CAGR for this region during the forecast period of 2024 to 2030 is anticipated to be robust, reflecting the region's strong emphasis on risk management and due diligence. As businesses continue to navigate an increasingly complex global landscape, the demand for comprehensive background check services is likely to remain strong, driving growth in the market. This trend underscores the critical role that background checks play in helping businesses make informed decisions and build trustworthy relationships with their partners and stakeholders.

| Report Metric | Details |

| Report Name | Business Background Check - Market |

| Forecasted market size in 2030 | US$ 2294.6 million |

| CAGR | 3.3% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Sterling Infosystems, First Aduvatage, HireRight, Kroll, Spokeo, Instant Checkmate, Checkr, PeopleConnect, TazWorks, PeopleFinders, BeenVerified, GoodHire, Orange Tree Employment Screening, Inteligator, TruthFinder |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |