What is Global MEMS Actuator Market?

The Global MEMS Actuator Market refers to the worldwide industry focused on the production and distribution of Micro-Electro-Mechanical Systems (MEMS) actuators. These tiny devices are integral components in various electronic systems, converting electrical signals into mechanical movement. MEMS actuators are pivotal in numerous applications due to their small size, low power consumption, and high precision. They are used in a wide range of industries, including automotive, consumer electronics, healthcare, and industrial machinery. The market is driven by the increasing demand for miniaturized electronic devices and the growing adoption of automation across different sectors. As technology advances, MEMS actuators are becoming more sophisticated, offering enhanced performance and reliability. This market is characterized by continuous innovation and development, with companies investing heavily in research and development to create more efficient and versatile actuators. The global MEMS actuator market is expected to experience significant growth in the coming years, driven by technological advancements and the increasing integration of MEMS technology in various applications. The market's expansion is also supported by the rising demand for smart devices and the Internet of Things (IoT), which require compact and efficient components like MEMS actuators.

Electrostatic Actuator, Thermal Actuator, Piezoelectric Actuator, Magnetic Actuator, Others in the Global MEMS Actuator Market:

Electrostatic actuators are a type of MEMS actuator that operate based on the principle of electrostatic force. They are widely used in applications where precise control of movement is required, such as in micro-mirrors for optical systems and in micro-valves for fluid control. Electrostatic actuators are favored for their low power consumption and fast response times, making them ideal for high-speed applications. However, they typically require high voltages to operate, which can be a limitation in some scenarios. Thermal actuators, on the other hand, utilize the expansion and contraction of materials in response to temperature changes to produce movement. These actuators are commonly used in applications where large displacements are needed, such as in micro-grippers and micro-pumps. Thermal actuators are known for their simplicity and reliability, but they tend to have slower response times compared to other types of actuators. Piezoelectric actuators leverage the piezoelectric effect, where certain materials generate an electric charge in response to mechanical stress. These actuators are highly precise and can produce very small movements, making them suitable for applications like precision positioning and vibration control. Piezoelectric actuators are often used in high-precision instruments and devices that require fine control. Magnetic actuators use magnetic fields to generate motion and are commonly found in applications that require strong forces, such as in micro-motors and micro-speakers. They are known for their robustness and ability to operate in harsh environments. However, magnetic actuators can be bulkier compared to other types of MEMS actuators. The "Others" category in the MEMS actuator market includes various niche and emerging technologies that do not fit into the traditional categories. These may include actuators that use novel materials or mechanisms to achieve movement. As the MEMS actuator market continues to evolve, new types of actuators are being developed to meet the specific needs of different applications. Each type of actuator has its own set of advantages and limitations, and the choice of actuator depends on the specific requirements of the application, such as size, power consumption, speed, and precision. The diversity of MEMS actuators allows for a wide range of applications, from consumer electronics to industrial machinery, and their continued development is crucial for the advancement of technology in various fields.

Machine and Equipment, Automobile, Consumer Electronic Products, Others in the Global MEMS Actuator Market:

The Global MEMS Actuator Market finds extensive usage across various sectors, including machine and equipment, automobile, consumer electronic products, and others. In the realm of machines and equipment, MEMS actuators are integral to the functioning of precision instruments and automation systems. They are used in applications such as micro-pumps, micro-valves, and micro-grippers, where precise control and miniaturization are essential. The ability of MEMS actuators to provide accurate and reliable movement makes them ideal for use in complex machinery and equipment, enhancing their performance and efficiency. In the automotive industry, MEMS actuators play a crucial role in the development of advanced driver-assistance systems (ADAS) and other automotive electronics. They are used in applications such as airbag deployment systems, tire pressure monitoring systems, and adaptive lighting systems. The compact size and low power consumption of MEMS actuators make them suitable for integration into the limited space available in vehicles, contributing to the overall safety and functionality of modern automobiles. Consumer electronic products are another significant area of application for MEMS actuators. They are used in devices such as smartphones, tablets, and wearable technology, where they enable features like autofocus in cameras, haptic feedback, and motion sensing. The demand for smaller, more efficient electronic devices drives the need for MEMS actuators, which offer the precision and reliability required for these applications. Additionally, MEMS actuators are used in various other sectors, including healthcare, where they are employed in medical devices such as insulin pumps and hearing aids. The versatility and adaptability of MEMS actuators make them suitable for a wide range of applications, and their continued development is essential for the advancement of technology in these areas. As the demand for miniaturized and efficient components continues to grow, the Global MEMS Actuator Market is expected to expand, driven by the increasing adoption of MEMS technology across different industries.

Global MEMS Actuator Market Outlook:

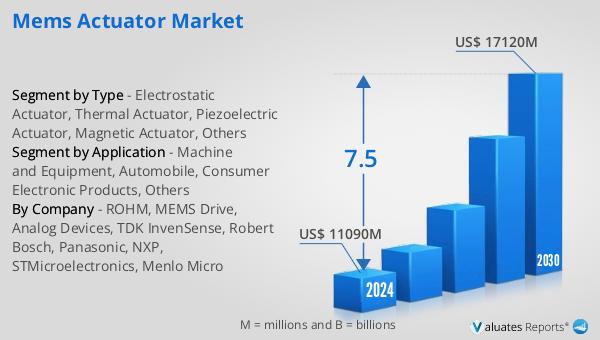

The global MEMS Actuator market is anticipated to witness substantial growth over the coming years. Starting from a valuation of approximately US$ 11,090 million in 2024, it is expected to reach around US$ 17,120 million by 2030. This growth trajectory represents a Compound Annual Growth Rate (CAGR) of 7.5% during the forecast period. This expansion is indicative of the increasing demand for MEMS actuators across various industries, driven by the need for miniaturized and efficient components in modern electronic devices. The market's growth is supported by technological advancements and the rising adoption of automation and smart devices. As industries continue to integrate MEMS technology into their products and systems, the demand for MEMS actuators is expected to rise significantly. The market's expansion is also fueled by the growing popularity of the Internet of Things (IoT) and the increasing need for compact and reliable components in connected devices. The MEMS actuator market's growth is a testament to the importance of these tiny devices in the advancement of technology and their role in shaping the future of various industries. As the market continues to evolve, companies are investing in research and development to create more efficient and versatile actuators, further driving the market's growth.

| Report Metric | Details |

| Report Name | MEMS Actuator Market |

| Accounted market size in 2024 | US$ 11090 million |

| Forecasted market size in 2030 | US$ 17120 million |

| CAGR | 7.5 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | ROHM, MEMS Drive, Analog Devices, TDK InvenSense, Robert Bosch, Panasonic, NXP, STMicroelectronics, Menlo Micro |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |