What is Global Size Exclusion Chromatography Column Market?

The Global Size Exclusion Chromatography (SEC) Column Market is a specialized segment within the broader chromatography market, focusing on the separation and analysis of molecules based on their size. This technique is widely used in various industries, including pharmaceuticals, biotechnology, and chemical manufacturing, to analyze proteins, polymers, and other macromolecules. The market for SEC columns is driven by the increasing demand for accurate and efficient analytical techniques in research and development activities. These columns are essential tools in laboratories for quality control and assurance, helping scientists and researchers to understand the molecular weight distribution and purity of samples. The growth of this market is also fueled by advancements in technology, which have led to the development of more sophisticated and efficient columns that offer higher resolution and faster analysis times. As industries continue to invest in research and development, the demand for SEC columns is expected to rise, making it a vital component of the analytical instrumentation market. The market is characterized by a diverse range of products, catering to different applications and requirements, ensuring that there is a suitable solution for every analytical need.

ID <3.5 mm, ID 3.5-6 mm, ID 6-8 mm in the Global Size Exclusion Chromatography Column Market:

In the Global Size Exclusion Chromatography Column Market, the internal diameter (ID) of the columns plays a crucial role in determining their application and efficiency. Columns with an ID of less than 3.5 mm are typically used for high-resolution analysis and are favored in applications where sample volume is limited. These columns are ideal for detailed analysis of small molecules and are often used in research settings where precision is paramount. The smaller diameter allows for better separation efficiency and faster analysis times, making them suitable for high-throughput environments. On the other hand, columns with an ID ranging from 3.5 mm to 6 mm are more versatile and are commonly used in both research and industrial applications. They offer a balance between resolution and sample capacity, making them suitable for a wide range of analyses, including protein and polymer analysis. These columns are often used in quality control laboratories where a moderate level of detail is required, and sample sizes are larger. Columns with an ID of 6 mm to 8 mm are designed for preparative applications where larger sample volumes are processed. These columns are used in industrial settings where the focus is on the purification and isolation of specific compounds. The larger diameter allows for higher sample throughput, making them ideal for large-scale production processes. Each of these column types serves a specific purpose, and their selection depends on the specific requirements of the analysis being performed. The choice of column diameter is influenced by factors such as the nature of the sample, the desired resolution, and the available instrumentation. As the demand for more efficient and precise analytical techniques continues to grow, the market for SEC columns with varying diameters is expected to expand, offering a wide range of options for researchers and industry professionals alike.

Protein Analysis, Polymer Analysis, Others in the Global Size Exclusion Chromatography Column Market:

The Global Size Exclusion Chromatography Column Market finds extensive usage in various analytical applications, particularly in protein analysis, polymer analysis, and other specialized areas. In protein analysis, SEC columns are indispensable tools for determining the molecular weight distribution and purity of proteins. They are used to separate proteins based on their size, allowing researchers to study their structure and function in detail. This is crucial in the development of biopharmaceuticals, where understanding the properties of proteins is essential for ensuring the efficacy and safety of the final product. SEC columns are also used in the characterization of protein aggregates, which can impact the stability and performance of therapeutic proteins. In polymer analysis, SEC columns are used to determine the molecular weight distribution of polymers, which is a critical parameter in understanding their physical and chemical properties. This information is vital for the development of new materials and for quality control in polymer manufacturing. SEC columns allow for the separation of polymers based on their size, providing insights into their structure and behavior. This is particularly important in industries such as plastics, where the properties of the final product are heavily influenced by the molecular weight distribution of the polymers used. In addition to protein and polymer analysis, SEC columns are used in a variety of other applications, including the analysis of nanoparticles, oligosaccharides, and other macromolecules. They are also used in the purification of complex mixtures, where the separation of components based on size is required. The versatility of SEC columns makes them valuable tools in a wide range of research and industrial settings, where accurate and efficient analysis is essential. As the demand for more sophisticated analytical techniques continues to grow, the usage of SEC columns in these areas is expected to increase, driving the growth of the market.

Global Size Exclusion Chromatography Column Market Outlook:

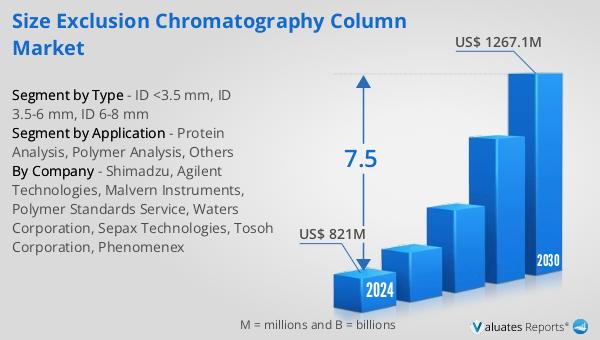

The outlook for the Global Size Exclusion Chromatography Column Market is promising, with projections indicating significant growth in the coming years. The market is expected to expand from $821 million in 2024 to $1,267.1 million by 2030, reflecting a compound annual growth rate (CAGR) of 7.5% during the forecast period. This growth is driven by the increasing demand for advanced analytical techniques in various industries, including pharmaceuticals, biotechnology, and chemical manufacturing. The need for accurate and efficient analysis of macromolecules is a key factor contributing to the expansion of the market. Additionally, the broader market for medical devices, estimated at $603 billion in 2023, is also expected to grow at a CAGR of 5% over the next six years. This growth is indicative of the increasing investment in research and development activities, which in turn drives the demand for analytical instrumentation such as SEC columns. As industries continue to prioritize innovation and quality control, the market for SEC columns is poised for substantial growth, offering numerous opportunities for manufacturers and suppliers in the sector. The combination of technological advancements and the growing emphasis on precision and efficiency in analytical processes is expected to further propel the market forward, ensuring its continued expansion in the years to come.

| Report Metric | Details |

| Report Name | Size Exclusion Chromatography Column Market |

| Accounted market size in 2024 | US$ 821 million |

| Forecasted market size in 2030 | US$ 1267.1 million |

| CAGR | 7.5 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Segment by Region |

|

| By Company | Shimadzu, Agilent Technologies, Malvern Instruments, Polymer Standards Service, Waters Corporation, Sepax Technologies, Tosoh Corporation, Phenomenex |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |