What is Global Aviation De-icing and Anti-icing Systems Market?

The Global Aviation De-icing and Anti-icing Systems Market is a specialized sector within the aviation industry that focuses on technologies and solutions designed to remove and prevent the accumulation of ice on aircraft surfaces. Ice formation on aircraft can pose significant safety risks, including reduced lift, increased drag, and impaired control surfaces, which can lead to accidents. De-icing systems are used to remove ice that has already formed, while anti-icing systems prevent ice from forming in the first place. These systems are essential for ensuring the safety and efficiency of aircraft operations, particularly in regions with harsh winter conditions. The market encompasses a variety of technologies, including mechanical, electric, liquid, and hot air systems, each with its own advantages and applications. The demand for these systems is driven by the need for enhanced safety measures, regulatory requirements, and the increasing number of aircraft in service globally.

Mechanical De-icing System, Electric Pulse Anti-icing System, Liquid Anti-icing System, Hot Air Anti-icing System, Electric Heating Anti-icing System in the Global Aviation De-icing and Anti-icing Systems Market:

Mechanical De-icing Systems are among the most traditional methods used in the aviation industry. These systems typically involve the use of pneumatic boots attached to the leading edges of aircraft wings and tail surfaces. When ice is detected, these boots inflate and deflate rapidly, breaking the ice and allowing it to be shed from the aircraft. This method is highly effective but requires regular maintenance to ensure the boots remain functional. Electric Pulse Anti-icing Systems, on the other hand, use electrical pulses to create vibrations on the aircraft surface, preventing ice from adhering. This technology is relatively new and offers the advantage of being lightweight and requiring less power compared to traditional methods. Liquid Anti-icing Systems involve the application of anti-icing fluids, such as glycol-based solutions, to the aircraft surfaces. These fluids lower the freezing point of water, preventing ice from forming. This method is commonly used during pre-flight preparations and can be reapplied as needed. Hot Air Anti-icing Systems utilize hot air bled from the aircraft's engines to heat critical surfaces, such as the wings and tail. This method is highly effective and is often used in conjunction with other systems for maximum protection. Finally, Electric Heating Anti-icing Systems use electrically heated elements embedded in the aircraft surfaces to prevent ice formation. This method is particularly useful for smaller aircraft and helicopters, where weight and power consumption are critical considerations. Each of these systems plays a vital role in ensuring the safety and efficiency of aircraft operations in icy conditions.

Commercial Aircraft, Fighter, Fire Plane, Others in the Global Aviation De-icing and Anti-icing Systems Market:

The usage of Global Aviation De-icing and Anti-icing Systems Market extends across various types of aircraft, including commercial aircraft, fighter jets, fire planes, and others. In commercial aircraft, these systems are crucial for maintaining safety during takeoff, flight, and landing in icy conditions. Airlines invest heavily in de-icing and anti-icing technologies to ensure passenger safety and minimize delays caused by adverse weather. For fighter jets, the need for reliable de-icing and anti-icing systems is even more critical. These aircraft often operate in extreme conditions and require advanced systems to maintain performance and maneuverability. The ability to quickly and effectively remove ice can be the difference between mission success and failure. Fire planes, which are used for aerial firefighting, also benefit from these systems. These aircraft often operate in remote and rugged environments where weather conditions can change rapidly. De-icing and anti-icing systems ensure that fire planes can respond quickly to emergencies without being grounded by ice accumulation. Other types of aircraft, such as private jets, helicopters, and cargo planes, also rely on these systems to ensure safe and efficient operations. The versatility and effectiveness of de-icing and anti-icing technologies make them indispensable across the aviation industry.

Global Aviation De-icing and Anti-icing Systems Market Outlook:

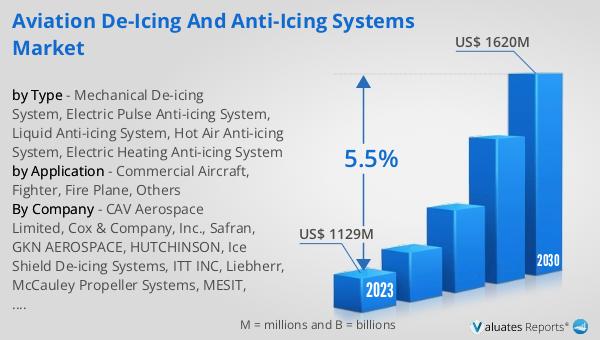

The global Aviation De-icing and Anti-icing Systems market was valued at US$ 1129 million in 2023 and is anticipated to reach US$ 1620 million by 2030, witnessing a CAGR of 5.5% during the forecast period 2024-2030. According to research data from the company's Construction Machinery Research Center, the total sales of the top 50 global construction machinery manufacturers will reach US$230 billion in 2022. Sales revenue accounted for 26%, and North America accounted for 23%. According to data from the China Machinery Industry Federation, the operating income of the construction machinery industry in 2022 will drop by more than 12%.

| Report Metric | Details |

| Report Name | Aviation De-icing and Anti-icing Systems Market |

| Accounted market size in 2023 | US$ 1129 million |

| Forecasted market size in 2030 | US$ 1620 million |

| CAGR | 5.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | CAV Aerospace Limited, Cox & Company, Inc., Safran, GKN AEROSPACE, HUTCHINSON, Ice Shield De-icing Systems, ITT INC, Liebherr, McCauley Propeller Systems, MESIT, THERMOCOAX, UTC Aerospace Systems, Ultra Electronics Controls, UBIQ Aerospace, TDG Aerospace |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |