What is Global Silicon Wafer Manufacturing Equipment Market?

The Global Silicon Wafer Manufacturing Equipment Market refers to the industry that produces machinery and tools used to create silicon wafers. These wafers are thin slices of silicon, a key material in the production of semiconductors and solar cells. The equipment used in this market includes machines for slicing, polishing, and cleaning silicon wafers, as well as tools for inspecting and testing their quality. This market is crucial because silicon wafers are foundational components in many electronic devices, including computers, smartphones, and solar panels. The demand for silicon wafers is driven by the growing need for advanced electronics and renewable energy solutions. As technology continues to evolve, the equipment used to manufacture silicon wafers must also advance to meet higher standards of precision and efficiency.

Monocrystalline Silicon, Polycrystalline Silicon in the Global Silicon Wafer Manufacturing Equipment Market:

Monocrystalline silicon and polycrystalline silicon are two primary types of silicon used in the Global Silicon Wafer Manufacturing Equipment Market. Monocrystalline silicon is made from a single, continuous crystal structure, which gives it superior electrical properties and efficiency. This type of silicon is commonly used in high-performance applications such as computer processors and high-efficiency solar panels. The manufacturing process for monocrystalline silicon involves growing a single crystal from molten silicon, a method known as the Czochralski process. This process requires highly specialized equipment to control the temperature and environment precisely, ensuring the crystal grows without defects. On the other hand, polycrystalline silicon is composed of multiple small silicon crystals. It is less expensive to produce than monocrystalline silicon and is often used in applications where cost is a more significant factor than performance, such as in standard solar panels and some electronic devices. The production of polycrystalline silicon involves melting silicon and allowing it to solidify in a mold, resulting in a material with a grainy structure. The equipment used in this process includes furnaces for melting the silicon and molds for shaping it. Both types of silicon require additional processing steps, such as slicing the silicon into wafers, polishing the wafers to a smooth finish, and cleaning them to remove any impurities. These steps involve various types of equipment, including wire saws for slicing, chemical-mechanical polishing machines for smoothing, and cleaning systems that use chemicals and ultrasonic waves to remove contaminants. The choice between monocrystalline and polycrystalline silicon depends on the specific requirements of the end application, with monocrystalline silicon being preferred for high-performance needs and polycrystalline silicon being chosen for cost-sensitive applications. The Global Silicon Wafer Manufacturing Equipment Market must cater to both types of silicon, providing the necessary tools and machinery to produce high-quality wafers efficiently and cost-effectively. As the demand for electronic devices and renewable energy solutions continues to grow, the market for silicon wafer manufacturing equipment is expected to expand, driven by the need for more advanced and efficient production technologies.

Semiconductor, Photovoltaics, Others in the Global Silicon Wafer Manufacturing Equipment Market:

The Global Silicon Wafer Manufacturing Equipment Market plays a crucial role in several key areas, including semiconductors, photovoltaics, and other applications. In the semiconductor industry, silicon wafers are the foundational material for creating integrated circuits, which are essential components in nearly all electronic devices. The equipment used in this sector includes machines for slicing silicon ingots into wafers, polishing the wafers to achieve a smooth surface, and cleaning them to remove any impurities. Additionally, advanced inspection and testing equipment are used to ensure the wafers meet stringent quality standards. The precision and reliability of this equipment are critical, as even minor defects in silicon wafers can lead to significant performance issues in the final electronic products. In the field of photovoltaics, silicon wafers are used to manufacture solar cells, which convert sunlight into electricity. The equipment used in this area includes tools for cutting silicon ingots into wafers, texturing the wafer surface to enhance light absorption, and applying anti-reflective coatings to improve efficiency. The demand for high-quality silicon wafers in the photovoltaic industry is driven by the need for more efficient and cost-effective solar panels. As the world shifts towards renewable energy sources, the importance of advanced silicon wafer manufacturing equipment in this sector continues to grow. Beyond semiconductors and photovoltaics, silicon wafers are also used in various other applications, such as sensors, MEMS (Micro-Electro-Mechanical Systems), and power devices. These applications require specialized equipment to produce wafers with specific properties tailored to their unique requirements. For example, MEMS devices, which are used in a wide range of applications from automotive sensors to medical devices, require silicon wafers with precise dimensions and surface characteristics. The equipment used to manufacture these wafers must be capable of achieving the high levels of precision and consistency needed for these advanced applications. Overall, the Global Silicon Wafer Manufacturing Equipment Market is essential for producing the high-quality silicon wafers required in a wide range of industries. The continued advancement of this equipment is crucial for meeting the growing demand for more efficient and reliable electronic devices, renewable energy solutions, and other high-tech applications.

Global Silicon Wafer Manufacturing Equipment Market Outlook:

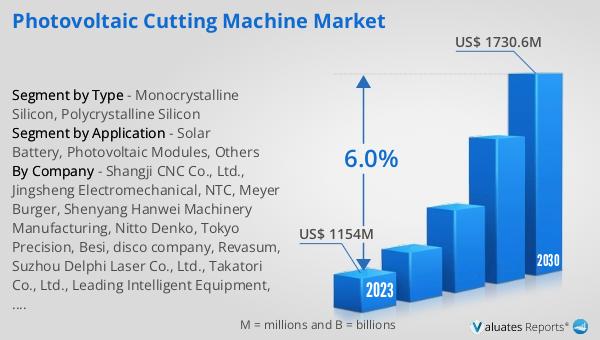

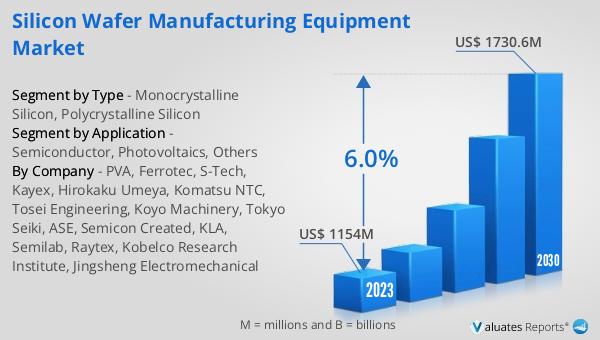

The global Silicon Wafer Manufacturing Equipment market was valued at US$ 1154 million in 2023 and is anticipated to reach US$ 1730.6 million by 2030, witnessing a CAGR of 6.0% during the forecast period 2024-2030. This market outlook highlights the significant growth expected in the industry over the coming years. The increasing demand for advanced electronic devices and renewable energy solutions is driving the need for high-quality silicon wafers, which in turn fuels the demand for sophisticated manufacturing equipment. As technology continues to evolve, the equipment used to produce silicon wafers must also advance to meet higher standards of precision and efficiency. The projected growth in the market reflects the ongoing investments in research and development, as well as the adoption of new technologies to enhance the manufacturing process. Companies operating in this market are focusing on developing innovative solutions to improve the quality and performance of silicon wafers while reducing production costs. This growth trajectory underscores the critical role of silicon wafer manufacturing equipment in supporting the advancement of various high-tech industries, from semiconductors to renewable energy.

| Report Metric | Details |

| Report Name | Silicon Wafer Manufacturing Equipment Market |

| Accounted market size in 2023 | US$ 1154 million |

| Forecasted market size in 2030 | US$ 1730.6 million |

| CAGR | 6.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | PVA, Ferrotec, S-Tech, Kayex, Hirokaku Umeya, Komatsu NTC, Tosei Engineering, Koyo Machinery, Tokyo Seiki, ASE, Semicon Created, KLA, Semilab, Raytex, Kobelco Research Institute, Jingsheng Electromechanical |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |