What is Global Industrial Microwave Heating Equipment Market?

The Global Industrial Microwave Heating Equipment Market refers to the industry focused on the production and distribution of microwave-based heating systems used in various industrial applications. These systems utilize microwave energy to heat materials quickly and uniformly, making them highly efficient compared to traditional heating methods. The market encompasses a wide range of equipment, including microwave dryers, sterilizers, and curing equipment, among others. These devices are employed across multiple sectors such as food and beverage, pharmaceuticals, chemicals, textiles, and more. The growing demand for energy-efficient and time-saving heating solutions is driving the expansion of this market. Additionally, advancements in microwave technology and increasing awareness about the benefits of microwave heating are contributing to its growth. The market is characterized by the presence of several key players who are continuously innovating to offer advanced and customized solutions to meet the specific needs of different industries.

Microwave Dryer, Microwave Sterilizer, Microwave Curing Equipment, Others in the Global Industrial Microwave Heating Equipment Market:

Microwave dryers are a significant segment within the Global Industrial Microwave Heating Equipment Market. These dryers use microwave energy to remove moisture from materials, making them ideal for applications in the food and beverage industry, pharmaceuticals, and chemicals. The rapid and uniform drying process helps in preserving the quality and nutritional value of food products, while also reducing drying times significantly. Microwave sterilizers, on the other hand, are used to eliminate microorganisms from various products, ensuring their safety and extending their shelf life. This equipment is crucial in the pharmaceutical and biotechnology sectors, where maintaining sterility is paramount. Microwave curing equipment is employed in industries such as ceramics, textiles, and wood processing. This equipment uses microwave energy to cure or harden materials, enhancing their durability and performance. The curing process is faster and more energy-efficient compared to conventional methods, making it a preferred choice for many manufacturers. Other types of industrial microwave heating equipment include systems designed for specific applications such as thawing frozen products, pasteurization, and tempering. These specialized systems cater to the unique requirements of different industries, providing tailored solutions that enhance productivity and efficiency. The versatility and efficiency of microwave heating equipment make it an indispensable tool in modern industrial processes.

Food and Beverage, Chemical, Pharmaceuticals and Biotechnology, Paper, Wood & Derivatives, Ceramics, Textile, Others in the Global Industrial Microwave Heating Equipment Market:

The usage of Global Industrial Microwave Heating Equipment Market spans across various industries, each benefiting from the unique advantages offered by microwave technology. In the food and beverage industry, microwave heating equipment is used for drying, sterilizing, and cooking food products. The rapid and uniform heating ensures that food retains its nutritional value and taste, while also extending its shelf life. In the chemical industry, microwave heating is employed for processes such as drying, curing, and synthesis of chemical compounds. The precise control over temperature and heating rates provided by microwave technology enhances the efficiency and quality of chemical processes. The pharmaceutical and biotechnology sectors utilize microwave heating equipment for sterilization, drying, and synthesis of pharmaceutical compounds. The ability to achieve high levels of sterility and precise control over heating parameters makes microwave equipment indispensable in these industries. In the paper, wood, and derivatives industry, microwave heating is used for drying and curing processes. The uniform heating provided by microwave technology ensures that materials are dried or cured evenly, reducing the risk of defects and improving product quality. The ceramics industry benefits from microwave curing equipment, which provides faster and more energy-efficient curing of ceramic materials. This results in improved product quality and reduced production times. In the textile industry, microwave heating is used for drying and curing textile materials, enhancing their durability and performance. Other industries, such as rubber and plastics, also utilize microwave heating equipment for various applications, benefiting from the efficiency and precision offered by microwave technology. The widespread adoption of microwave heating equipment across these diverse industries highlights its versatility and effectiveness in enhancing industrial processes.

Global Industrial Microwave Heating Equipment Market Outlook:

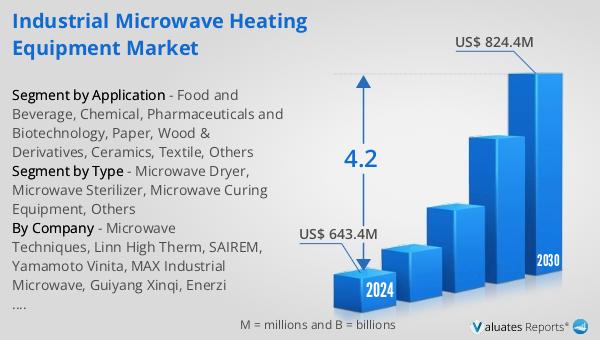

The global Industrial Microwave Heating Equipment market is anticipated to expand from US$ 643.4 million in 2024 to US$ 824.4 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 4.2% during the forecast period. Leading players in this market include Microwave Techniques, Linn High Therm, SAIREM, Yamamoto Vinita, MAX Industrial Microwave, Guiyang Xinqi, Enerzi Microwave Systems, and Jinan Talin Tech, with the top eight companies collectively holding around 16% of the market share. Among these, Microwave Techniques stands out as the largest producer, commanding a 3% share. The Asia-Pacific region dominates the market, accounting for approximately 45% of the global share, followed by North America and Europe, which hold about 26% and 20% respectively. In terms of product types, microwave dryers represent the largest segment, making up around 69% of the market. When it comes to applications, the food and beverage sector is the most significant, constituting about 33% of the market.

| Report Metric | Details |

| Report Name | Industrial Microwave Heating Equipment Market |

| Accounted market size in 2024 | US$ 643.4 million |

| Forecasted market size in 2030 | US$ 824.4 million |

| CAGR | 4.2 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Microwave Techniques, Linn High Therm, SAIREM, Yamamoto Vinita, MAX Industrial Microwave, Guiyang Xinqi, Enerzi Microwave Systems, Jinan Talin Tech, Kerone, Thermex-Thermatron, Püschner, Cober Electronics, Guangzhou Diwei, Shandong Loyal Industrial, Microdry Inc., Seji-tech Co., Ltd., ROMILL, Jinan Kelid Machinery |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |