What is Global Embedded Vibration Monitoring System Market?

The Global Embedded Vibration Monitoring System Market refers to the industry focused on the development, production, and implementation of systems that monitor vibrations in machinery and equipment. These systems are embedded within the machinery to continuously track and analyze vibration data, which helps in identifying potential issues before they lead to significant failures. By detecting anomalies early, these systems can prevent costly downtime and extend the lifespan of equipment. The market encompasses a wide range of industries, including manufacturing, automotive, aerospace, and more, where machinery reliability and maintenance are critical. The increasing demand for predictive maintenance and the need to enhance operational efficiency are driving the growth of this market. As industries continue to adopt advanced technologies, the Global Embedded Vibration Monitoring System Market is expected to expand, offering innovative solutions to meet the evolving needs of various sectors.

Accelerometers, Proximity probes, Velocity sensors, Transmitters, Others in the Global Embedded Vibration Monitoring System Market:

Accelerometers, proximity probes, velocity sensors, transmitters, and other components play crucial roles in the Global Embedded Vibration Monitoring System Market. Accelerometers are sensors that measure the acceleration forces acting on an object, which can be used to detect vibrations and monitor the condition of machinery. They are essential for identifying imbalances, misalignments, and other issues that can lead to equipment failure. Proximity probes, on the other hand, measure the distance between a sensor and a target object, providing precise data on the position and movement of machine parts. This information is vital for detecting shaft misalignment, rotor imbalance, and other mechanical problems. Velocity sensors measure the speed of vibration, offering insights into the severity and frequency of vibrations. These sensors are particularly useful for monitoring rotating machinery, such as motors and pumps, where excessive vibration can indicate wear and tear or impending failure. Transmitters are devices that convert sensor data into signals that can be transmitted to monitoring systems for analysis. They play a critical role in ensuring that vibration data is accurately captured and communicated in real-time. Other components in the market include data acquisition systems, software, and communication modules that work together to provide a comprehensive vibration monitoring solution. These components are integrated into a single system that continuously monitors machinery, analyzes data, and provides actionable insights to maintenance teams. By leveraging these technologies, industries can implement predictive maintenance strategies, reduce downtime, and improve overall operational efficiency. The Global Embedded Vibration Monitoring System Market is characterized by continuous innovation, with manufacturers developing advanced sensors and monitoring solutions to meet the evolving needs of various industries. As technology advances, these systems are becoming more sophisticated, offering higher accuracy, better data analysis capabilities, and improved integration with other industrial systems. This ongoing development is driving the adoption of embedded vibration monitoring systems across a wide range of applications, from manufacturing and automotive to aerospace and beyond.

Chemicals, Automobile Industry, Aerospace and Defense, Food and Drink, Marines, Pulp and Paper, Others in the Global Embedded Vibration Monitoring System Market:

The usage of Global Embedded Vibration Monitoring System Market spans across various industries, including chemicals, automobile, aerospace and defense, food and drink, marines, pulp and paper, and others. In the chemicals industry, these systems are used to monitor the condition of pumps, compressors, and other critical equipment, ensuring that they operate efficiently and safely. By detecting early signs of wear and tear, companies can prevent equipment failures and minimize production downtime. In the automobile industry, embedded vibration monitoring systems are used to monitor the performance of engines, transmissions, and other components. This helps manufacturers identify potential issues before they lead to costly recalls or warranty claims. In the aerospace and defense sector, these systems are used to monitor the condition of aircraft engines, landing gear, and other critical components. By ensuring that these parts are in optimal condition, companies can enhance the safety and reliability of their aircraft. In the food and drink industry, vibration monitoring systems are used to monitor the condition of mixers, conveyors, and other equipment. This helps companies maintain product quality and prevent contamination. In the marine industry, these systems are used to monitor the condition of ship engines, propellers, and other critical components. By detecting early signs of wear and tear, companies can prevent costly repairs and ensure the safety of their vessels. In the pulp and paper industry, vibration monitoring systems are used to monitor the condition of paper machines, pumps, and other equipment. This helps companies maintain production efficiency and prevent equipment failures. Other industries that use embedded vibration monitoring systems include power generation, oil and gas, and mining. In each of these industries, the ability to monitor equipment condition in real-time and detect potential issues early is critical for maintaining operational efficiency and preventing costly downtime. The adoption of embedded vibration monitoring systems is driven by the need to enhance equipment reliability, reduce maintenance costs, and improve overall operational efficiency. As industries continue to adopt advanced technologies, the demand for these systems is expected to grow, offering new opportunities for innovation and development.

Global Embedded Vibration Monitoring System Market Outlook:

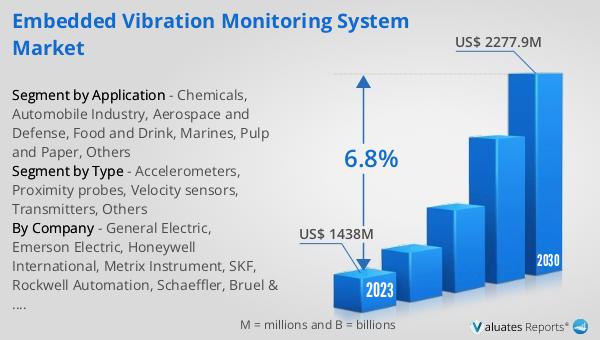

The global Embedded Vibration Monitoring System market was valued at US$ 1438 million in 2023 and is anticipated to reach US$ 2277.9 million by 2030, witnessing a CAGR of 6.8% during the forecast period 2024-2030. This growth reflects the increasing demand for predictive maintenance solutions and the need to enhance operational efficiency across various industries. As companies continue to invest in advanced technologies to monitor and maintain their equipment, the market for embedded vibration monitoring systems is expected to expand. These systems offer significant benefits, including the ability to detect potential issues early, reduce downtime, and extend the lifespan of machinery. The continuous innovation in sensor technology, data analysis, and communication modules is driving the adoption of these systems across a wide range of applications. As industries strive to improve their operational efficiency and reduce maintenance costs, the demand for embedded vibration monitoring systems is likely to grow, creating new opportunities for manufacturers and solution providers in this market.

| Report Metric | Details |

| Report Name | Embedded Vibration Monitoring System Market |

| Accounted market size in 2023 | US$ 1438 million |

| Forecasted market size in 2030 | US$ 2277.9 million |

| CAGR | 6.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | General Electric, Emerson Electric, Honeywell International, Metrix Instrument, SKF, Rockwell Automation, Schaeffler, Bruel & Kjaer, Meggitt, Analog Devices |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |