What is Global Low Molecular Weight PVC Paste Resin Market?

The Global Low Molecular Weight PVC Paste Resin Market refers to the worldwide industry focused on the production and distribution of low molecular weight polyvinyl chloride (PVC) paste resin. This type of PVC paste resin is characterized by its lower molecular weight, which makes it particularly suitable for applications requiring flexibility, durability, and ease of processing. The market encompasses various regions and industries, including manufacturing sectors that utilize PVC paste resin in products such as gloves, artificial leather, automotive interiors, wallpaper, plastic flooring, paints, and coatings. The demand for low molecular weight PVC paste resin is driven by its versatile properties, which make it an essential material in numerous applications. The market is influenced by factors such as technological advancements, regulatory standards, and the overall economic environment. Companies operating in this market are continually innovating to improve product quality and meet the evolving needs of their customers.

Micro Suspension Method, Emulsion Method in the Global Low Molecular Weight PVC Paste Resin Market:

The Micro Suspension Method and Emulsion Method are two primary techniques used in the production of low molecular weight PVC paste resin. The Micro Suspension Method involves the polymerization of vinyl chloride monomer (VCM) in a water-based medium with the help of suspending agents and initiators. This method produces PVC particles that are uniform in size and have a narrow particle size distribution, which is crucial for achieving consistent quality in the final product. The process begins with the dispersion of VCM in water, followed by the addition of initiators that trigger the polymerization reaction. The resulting PVC particles are then separated, washed, and dried to obtain the final paste resin. This method is known for its efficiency and ability to produce high-quality PVC paste resin with excellent mechanical properties. On the other hand, the Emulsion Method involves the polymerization of VCM in an emulsion system, where the monomer is dispersed in water with the help of emulsifying agents. This method produces PVC particles that are much smaller in size compared to those produced by the Micro Suspension Method. The emulsion polymerization process starts with the formation of an emulsion by mixing VCM, water, and emulsifying agents. Initiators are then added to the emulsion to start the polymerization reaction. The resulting PVC particles are stabilized by the emulsifying agents, which prevent them from coalescing. After the polymerization is complete, the PVC particles are coagulated, washed, and dried to obtain the final paste resin. The Emulsion Method is known for its ability to produce PVC paste resin with a very fine particle size, which is ideal for applications requiring smooth and uniform coatings. Both methods have their advantages and are chosen based on the specific requirements of the end-use application. The Micro Suspension Method is preferred for applications that require PVC paste resin with excellent mechanical properties and uniform particle size, such as in the production of automotive interiors and plastic flooring. The Emulsion Method, on the other hand, is preferred for applications that require a very fine particle size and smooth finish, such as in the production of paints and coatings. The choice of method also depends on factors such as production cost, environmental impact, and regulatory compliance. Companies in the Global Low Molecular Weight PVC Paste Resin Market are continually optimizing these methods to improve efficiency, reduce costs, and meet the stringent quality standards required by their customers.

PVC Gloves, Artificial Leather, Automotive Interiors, Wallpaper, Plastic Floor, Paint and Coatings, Other in the Global Low Molecular Weight PVC Paste Resin Market:

The Global Low Molecular Weight PVC Paste Resin Market finds extensive usage in various applications, including PVC gloves, artificial leather, automotive interiors, wallpaper, plastic flooring, paints, and coatings. In the production of PVC gloves, low molecular weight PVC paste resin is used to create flexible and durable gloves that provide excellent protection and comfort. The resin's properties allow for the production of gloves that are resistant to chemicals, punctures, and abrasions, making them suitable for use in medical, industrial, and household applications. In the artificial leather industry, low molecular weight PVC paste resin is used to produce synthetic leather that mimics the appearance and texture of natural leather. The resin's flexibility and durability make it an ideal material for creating high-quality artificial leather products used in furniture, footwear, and fashion accessories. The automotive industry also relies on low molecular weight PVC paste resin for the production of interior components such as dashboards, door panels, and seat covers. The resin's ability to provide a smooth finish, along with its resistance to wear and tear, makes it a preferred material for automotive interiors. Wallpaper production is another significant application of low molecular weight PVC paste resin. The resin is used to create wallpapers that are easy to apply, durable, and resistant to moisture and stains. This makes PVC wallpapers a popular choice for both residential and commercial spaces. In the plastic flooring industry, low molecular weight PVC paste resin is used to produce flooring materials that are durable, easy to maintain, and available in a wide range of designs and colors. The resin's properties ensure that the flooring is resistant to scratches, stains, and moisture, making it suitable for high-traffic areas. In the paints and coatings industry, low molecular weight PVC paste resin is used to create coatings that provide excellent adhesion, flexibility, and resistance to chemicals and weathering. These coatings are used in various applications, including protective coatings for industrial equipment, decorative coatings for buildings, and coatings for consumer goods. The versatility of low molecular weight PVC paste resin makes it an essential material in the paints and coatings industry, where it is used to enhance the performance and durability of coatings. Other applications of low molecular weight PVC paste resin include the production of toys, medical devices, and packaging materials. The resin's properties, such as flexibility, durability, and resistance to chemicals, make it suitable for a wide range of applications. Companies in the Global Low Molecular Weight PVC Paste Resin Market are continually developing new formulations and applications to meet the evolving needs of their customers.

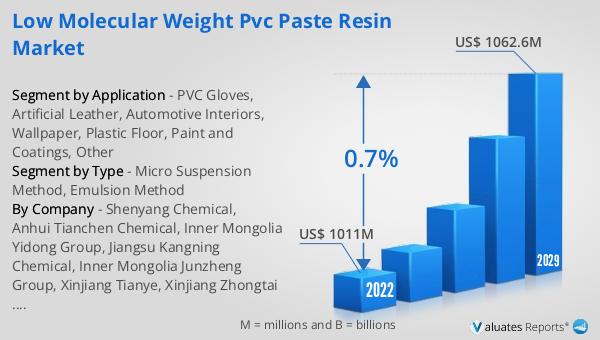

Global Low Molecular Weight PVC Paste Resin Market Outlook:

In 2023, the global market for Low Molecular Weight PVC Paste Resin was valued at approximately US$ 1011 million. Projections indicate that by 2030, this market is expected to grow to around US$ 1062.6 million, reflecting a compound annual growth rate (CAGR) of 0.7% over the forecast period from 2024 to 2030. This modest growth rate suggests a steady demand for low molecular weight PVC paste resin across various industries. The market's expansion can be attributed to the increasing applications of this versatile material in sectors such as automotive, construction, healthcare, and consumer goods. Companies operating in this market are focusing on innovation and quality improvement to cater to the specific needs of their customers. The steady growth also highlights the importance of low molecular weight PVC paste resin in modern manufacturing processes, where its unique properties such as flexibility, durability, and ease of processing are highly valued. As industries continue to evolve and new applications for PVC paste resin are discovered, the market is expected to maintain its growth trajectory, albeit at a gradual pace.

| Report Metric | Details |

| Report Name | Low Molecular Weight PVC Paste Resin Market |

| Accounted market size in 2023 | US$ 1011 million |

| Forecasted market size in 2030 | US$ 1062.6 million |

| CAGR | 0.7% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Shenyang Chemical, Anhui Tianchen Chemical, Inner Mongolia Yidong Group, Jiangsu Kangning Chemical, Inner Mongolia Junzheng Group, Xinjiang Tianye, Xinjiang Zhongtai Chemical, Tangshan Sanyou Group, Formosa Ningbo, Jining Zhongyin Electrochemical, Vinnolit, Kem One, Mexichem (Orbia), INEOS |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |