What is Global Air-Based Military Electro-Optical and Infrared Systems Market?

The Global Air-Based Military Electro-Optical and Infrared Systems Market refers to the industry focused on the development, production, and deployment of advanced optical and infrared technologies used in military aircraft. These systems are designed to enhance the capabilities of military forces by providing superior imaging, targeting, and surveillance functionalities. Electro-optical systems use electronic devices to detect and measure light, while infrared systems detect heat signatures, allowing for operations in low-visibility conditions such as night or adverse weather. These technologies are crucial for modern warfare, offering enhanced situational awareness, precision targeting, and improved reconnaissance capabilities. The market encompasses a wide range of products, including sensors, cameras, and targeting systems, which are integrated into various types of military aircraft, from fighter jets to unmanned aerial vehicles (UAVs). The continuous advancements in technology and the increasing demand for more sophisticated defense systems drive the growth of this market, making it a vital component of national security strategies worldwide.

Airborne System, Pilot Portable System in the Global Air-Based Military Electro-Optical and Infrared Systems Market:

Airborne systems and pilot portable systems are two critical components within the Global Air-Based Military Electro-Optical and Infrared Systems Market. Airborne systems are integrated directly into military aircraft, providing real-time data and imaging to pilots and ground control. These systems include advanced sensors and cameras that can detect and track targets from long distances, even in challenging environments. They are essential for missions that require high levels of precision and situational awareness, such as air-to-ground strikes, reconnaissance, and surveillance. The integration of these systems into aircraft allows for seamless communication and data sharing between different units, enhancing the overall effectiveness of military operations. On the other hand, pilot portable systems are designed to be carried and operated by individual pilots or crew members. These systems are typically more compact and lightweight, allowing for greater mobility and flexibility. They can be used for a variety of purposes, including target acquisition, navigation, and threat detection. Pilot portable systems are particularly useful in situations where quick deployment and adaptability are required, such as in search and rescue missions or in rapidly changing combat scenarios. Both airborne and pilot portable systems rely on cutting-edge technology to provide accurate and reliable data, ensuring that military personnel have the information they need to make informed decisions. The development and deployment of these systems are driven by the need for enhanced operational capabilities and the desire to maintain a technological edge over potential adversaries. As such, the Global Air-Based Military Electro-Optical and Infrared Systems Market continues to evolve, with ongoing research and development efforts aimed at improving the performance and functionality of these critical systems.

Military, National Defense, Others in the Global Air-Based Military Electro-Optical and Infrared Systems Market:

The usage of Global Air-Based Military Electro-Optical and Infrared Systems Market spans several key areas, including military operations, national defense, and other specialized applications. In military operations, these systems are indispensable for a wide range of missions, from combat to reconnaissance. They provide real-time imaging and targeting information, allowing military forces to engage targets with greater accuracy and effectiveness. The ability to operate in low-visibility conditions, such as at night or in adverse weather, gives military units a significant tactical advantage. These systems also enhance situational awareness, enabling commanders to make better-informed decisions and coordinate complex operations more effectively. In the realm of national defense, electro-optical and infrared systems play a crucial role in protecting a nation's airspace and critical infrastructure. They are used in early warning systems to detect and track potential threats, such as incoming missiles or unauthorized aircraft. By providing high-resolution imaging and precise tracking data, these systems help to ensure the security of a nation's borders and strategic assets. Additionally, they are used in intelligence, surveillance, and reconnaissance (ISR) missions to gather vital information about potential adversaries and their activities. Beyond military and national defense applications, these systems are also used in various other fields. For example, they are employed in search and rescue operations to locate and identify individuals in distress, even in challenging environments. They are also used in disaster response efforts to assess damage and coordinate relief efforts. In the field of environmental monitoring, electro-optical and infrared systems are used to track changes in the environment, such as deforestation or the movement of wildlife. Overall, the versatility and advanced capabilities of these systems make them valuable tools in a wide range of applications, contributing to the safety and security of nations and their citizens.

Global Air-Based Military Electro-Optical and Infrared Systems Market Outlook:

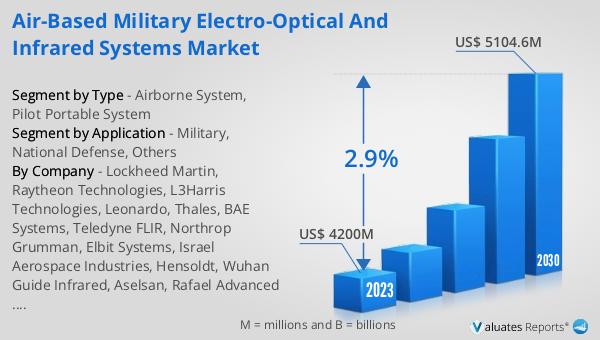

The global Air-Based Military Electro-Optical and Infrared Systems market was valued at US$ 4200 million in 2023 and is anticipated to reach US$ 5104.6 million by 2030, witnessing a CAGR of 2.9% during the forecast period 2024-2030. This market outlook highlights the steady growth and increasing demand for advanced electro-optical and infrared systems in the military sector. The projected growth reflects the ongoing investments in defense technologies and the continuous need for enhanced operational capabilities. As military forces around the world seek to maintain a technological edge, the demand for sophisticated imaging and targeting systems is expected to rise. The market's expansion is driven by the development of new and improved systems that offer greater accuracy, reliability, and functionality. This growth trajectory underscores the importance of electro-optical and infrared systems in modern warfare and national defense strategies. The increasing adoption of these systems in various military applications, from combat operations to intelligence gathering, further emphasizes their critical role in ensuring the effectiveness and efficiency of military forces. As the market continues to evolve, it is likely to see further advancements in technology and increased integration of these systems into a wide range of military platforms.

| Report Metric | Details |

| Report Name | Air-Based Military Electro-Optical and Infrared Systems Market |

| Accounted market size in 2023 | US$ 4200 million |

| Forecasted market size in 2030 | US$ 5104.6 million |

| CAGR | 2.9% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Lockheed Martin, Raytheon Technologies, L3Harris Technologies, Leonardo, Thales, BAE Systems, Teledyne FLIR, Northrop Grumman, Elbit Systems, Israel Aerospace Industries, Hensoldt, Wuhan Guide Infrared, Aselsan, Rafael Advanced Defense, Transvaro, Safran |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |