What is Global Printable Heat Shrink Tubing for Cable Market?

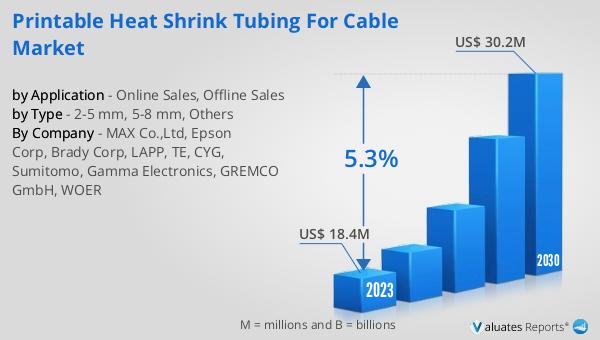

The Global Printable Heat Shrink Tubing for Cable Market is a niche yet significant segment within the broader cable management industry, focusing on solutions that not only protect cable connections but also offer identification features. This market revolves around the production and distribution of heat shrink tubing, a type of material that can be easily printed on and then shrunk through the application of heat to fit snugly around cables. The purpose of these tubings extends beyond mere protection; they are designed to provide a durable method for labeling and identifying various cables in complex systems, making them indispensable in environments where cable management is critical. With a valuation of US$ 18.4 million in 2023, the market is on a growth trajectory, expected to climb to US$ 30.2 million by 2030. This growth, at a compound annual growth rate (CAGR) of 5.3% during the forecast period from 2024 to 2030, underscores the increasing demand for efficient and reliable cable management solutions across various industries, including telecommunications, automotive, and electronics, among others.

2-5 mm, 5-8 mm, Others in the Global Printable Heat Shrink Tubing for Cable Market:

In the realm of the Global Printable Heat Shrink Tubing for Cable Market, the segmentation based on the size of the tubing, specifically 2-5 mm, 5-8 mm, and others, plays a pivotal role in catering to diverse application needs. The 2-5 mm segment, for instance, is particularly suited for smaller cable assemblies where space is at a premium and precision is key. These smaller tubings are ideal for electronics, aerospace, and automotive applications, where they not only provide protection and insulation but also facilitate easy identification of wiring, thereby enhancing safety and efficiency. On the other hand, the 5-8 mm range finds its utility in slightly larger cable bundles, common in industrial machinery, home appliances, and network servers. These tubings offer a balance between flexibility and durability, making them suitable for environments that require robust cable management solutions. The "others" category encompasses a variety of sizes beyond the 8 mm mark, addressing the needs of heavy-duty applications such as power distribution, outdoor telecommunications infrastructure, and large-scale manufacturing equipment. This segmentation ensures that the market can serve a wide array of industries with specific requirements, from delicate electronic components to rugged outdoor installations, highlighting the versatility and importance of printable heat shrink tubing in modern cable management practices.

Online Sales, Offline Sales in the Global Printable Heat Shrink Tubing for Cable Market:

The usage of Global Printable Heat Shrink Tubing for Cable Market products spans across both online and offline sales channels, each catering to different customer preferences and buying behaviors. Online sales have surged in popularity, offering convenience and a wide selection of products at competitive prices. This channel allows customers to easily compare different products, read reviews, and make informed decisions without the need to visit a physical store. It's particularly appealing to tech-savvy consumers and businesses looking for specific types of heat shrink tubing that may not be readily available locally. Online platforms also provide manufacturers with the opportunity to reach a global audience, expanding their market presence beyond traditional geographic limitations. Offline sales, on the other hand, remain a vital component of the market. Physical stores and direct sales through distributors offer the advantage of immediate availability and the ability to inspect products firsthand. This channel is especially important for industries where compliance with specific standards is critical, and the tactile evaluation of tubing quality can influence purchasing decisions. Both online and offline sales channels play crucial roles in the distribution of printable heat shrink tubing for cables, ensuring that the needs of diverse customer segments are met, from individual consumers to large corporations.

Global Printable Heat Shrink Tubing for Cable Market Outlook:

The market outlook for the Global Printable Heat Shrink Tubing for Cable sector presents a promising future, with the industry's value set to expand from US$ 18.4 million in 2023 to an estimated US$ 30.2 million by the year 2030. This growth trajectory, characterized by a steady compound annual growth rate (CAGR) of 5.3% throughout the forecast period spanning from 2024 to 2030, reflects the increasing reliance on and demand for sophisticated cable management solutions across various sectors. The surge in market value underscores the critical role that printable heat shrink tubing plays in ensuring the safety, efficiency, and reliability of cable systems in numerous applications. From telecommunications to automotive, and from consumer electronics to industrial machinery, the need for durable, easily identifiable cable protection solutions is more pronounced than ever. This upward trend in the market's valuation is indicative of the broader trends in technology and infrastructure development, where precision, safety, and efficiency are paramount.

| Report Metric | Details |

| Report Name | Printable Heat Shrink Tubing for Cable Market |

| Accounted market size in 2023 | US$ 18.4 million |

| Forecasted market size in 2030 | US$ 30.2 million |

| CAGR | 5.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | MAX Co.,Ltd, Epson Corp, Brady Corp, LAPP, TE, CYG, Sumitomo, Gamma Electronics, GREMCO GmbH, WOER |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |