What is Global Semiconductor Electrical Testing Equipment Market?

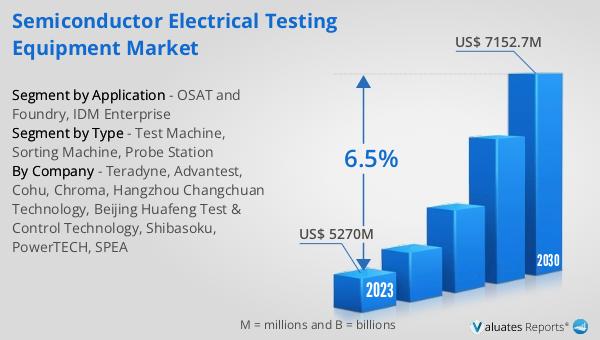

In the realm of technology, the Global Semiconductor Electrical Testing Equipment Market stands as a pivotal sector, ensuring the reliability and functionality of semiconductor devices before they are deployed in various applications. This market encompasses a broad array of equipment designed to test the electrical properties of semiconductors, a critical step in the manufacturing process. As semiconductors form the backbone of modern electronics, from smartphones to sophisticated computing systems, the demand for precise and efficient testing equipment has surged. The significance of this market lies in its role in maintaining the high standards of quality and performance expected in today's electronic products. By identifying defects and ensuring that semiconductor components meet the required specifications, electrical testing equipment helps in minimizing the risk of failures, thereby enhancing the overall reliability of electronic devices. This market's growth is propelled by the continuous advancements in semiconductor technology, including the development of smaller, faster, and more energy-efficient semiconductors, which necessitate more sophisticated testing solutions. As of 2023, the market's value was estimated at US$ 5270 million, with projections suggesting an increase to US$ 7152.7 million by 2030, marking a compound annual growth rate (CAGR) of 6.5%. This growth trajectory underscores the critical role of electrical testing equipment in the semiconductor industry's future, ensuring that as semiconductors become increasingly integral to technological progress, the tools used to test them evolve in tandem.

Test Machine, Sorting Machine, Probe Station in the Global Semiconductor Electrical Testing Equipment Market:

Diving deeper into the Global Semiconductor Electrical Testing Equipment Market, we find it segmented into various types of equipment, each serving a unique function in the semiconductor manufacturing process. Test machines, sorting machines, and probe stations represent the core categories of this market, each playing a crucial role in ensuring the quality and performance of semiconductor devices. Test machines are sophisticated devices that assess the electrical functionality of semiconductors under various conditions to ensure they meet the required performance standards. These machines are capable of conducting a wide range of tests, from basic electrical checks to complex functionality assessments, making them indispensable in the semiconductor manufacturing process. Sorting machines, on the other hand, are used to categorize semiconductors based on their performance characteristics. This process is vital for identifying and segregating components that meet the stringent quality standards from those that do not, thereby ensuring that only the highest quality semiconductors proceed to the next stages of production. Probe stations play a critical role in the early stages of semiconductor manufacturing. These devices are used to test the electrical properties of semiconductor wafers, identifying defects at an early stage and thus preventing the progression of faulty components through the manufacturing process. Together, these three types of equipment form the backbone of the Global Semiconductor Electrical Testing Equipment Market, each contributing to the meticulous process of semiconductor testing and quality assurance. Their combined use ensures that semiconductor devices are reliable, efficient, and capable of meeting the demands of various applications, from consumer electronics to industrial systems.

OSAT and Foundry, IDM Enterprise in the Global Semiconductor Electrical Testing Equipment Market:

The Global Semiconductor Electrical Testing Equipment Market finds its applications spread across various sectors, notably in Outsourced Semiconductor Assembly and Test (OSAT) services and Foundries, as well as Integrated Device Manufacturers (IDM) enterprises. In the OSAT and Foundry segment, electrical testing equipment plays a pivotal role in ensuring that semiconductors are assembled and tested to meet the highest standards of quality and performance. These services are crucial for companies that do not have their own semiconductor manufacturing facilities, relying instead on specialized providers to handle the assembly, testing, and packaging of their semiconductor devices. The use of advanced testing equipment in these settings helps in identifying potential defects and ensuring that only components that meet strict specifications are delivered to clients. This is particularly important in an industry where the functionality and reliability of semiconductor devices can significantly impact the final product's performance and consumer satisfaction. On the other hand, IDM enterprises, which control the entire semiconductor manufacturing process from design to assembly, also rely heavily on electrical testing equipment. In these companies, testing is an integral part of the production process, ensuring that every semiconductor device produced meets the company's stringent quality and performance criteria. The use of sophisticated testing equipment allows IDMs to maintain tight control over the quality of their products, thereby enhancing their competitiveness in the market. In both OSAT and Foundry services and IDM enterprises, the Global Semiconductor Electrical Testing Equipment Market is essential for maintaining the high standards of quality and reliability that are critical to the success of the semiconductor industry.

Global Semiconductor Electrical Testing Equipment Market Outlook:

The outlook for the Global Semiconductor Electrical Testing Equipment Market is notably positive, with its valuation in 2023 standing at US$ 5270 million and an expected rise to US$ 7152.7 million by 2030. This growth trajectory, marked by a compound annual growth rate (CAGR) of 6.5% during the forecast period from 2024 to 2030, highlights the robust demand and ongoing expansion within this sector. The market's growth is not confined to a single region; North America, Europe, and Japan collectively account for a significant portion of the market, holding a combined share of 23%. This widespread geographical distribution underscores the global reliance on semiconductor electrical testing equipment, reflecting the universal need for high-quality semiconductor devices across various industries. As semiconductors continue to play a crucial role in the advancement of technology, from consumer electronics to automotive and industrial applications, the demand for precise and efficient testing equipment is expected to remain strong. This market's growth is indicative of the increasing complexity and sophistication of semiconductor devices, necessitating advanced testing solutions to ensure their reliability and performance. The positive outlook for the Global Semiconductor Electrical Testing Equipment Market is a testament to the critical role it plays in the broader semiconductor industry, supporting the development and production of high-quality semiconductor components that are essential for the technological progress.

| Report Metric | Details |

| Report Name | Semiconductor Electrical Testing Equipment Market |

| Accounted market size in 2023 | US$ 5270 million |

| Forecasted market size in 2030 | US$ 7152.7 million |

| CAGR | 6.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Teradyne, Advantest, Cohu, Chroma, Hangzhou Changchuan Technology, Beijing Huafeng Test & Control Technology, Shibasoku, PowerTECH, SPEA |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |