What is Global Dairy Substitutes for Milk Market?

The Global Dairy Substitutes for Milk Market is a rapidly expanding sector that caters to the growing demand for plant-based alternatives to traditional dairy products. This market encompasses a wide range of non-dairy products made from plant sources such as almonds, soy, rice, oats, and coconut, designed to replace milk and its derivatives in various applications. The surge in popularity of dairy substitutes is largely driven by consumers' increasing health consciousness, dietary restrictions, lactose intolerance, and ethical concerns regarding animal welfare and environmental sustainability. These plant-based alternatives are not only appealing to vegans and vegetarians but also to a broader audience seeking healthier lifestyle choices. As a result, the Global Dairy Substitutes for Milk Market is experiencing significant growth, offering a plethora of options that mimic the taste, texture, and nutritional profile of traditional milk products, thereby catering to a diverse range of dietary needs and preferences.

Yogurt, Cream in the Global Dairy Substitutes for Milk Market:

Yogurt and cream-based products within the Global Dairy Substitutes for Milk Market are gaining remarkable traction, reflecting a broader shift towards plant-based diets. These substitutes are crafted from various plant sources, including almonds, coconuts, soy, oats, and cashews, designed to replicate the creamy texture and rich taste of traditional dairy-based yogurt and cream. The innovation in this segment has led to the development of products that not only match the sensory attributes of their dairy counterparts but also offer additional health benefits such as being lower in cholesterol and saturated fats, and free from lactose, making them suitable for consumers with dietary restrictions or lactose intolerance. Furthermore, these dairy-free alternatives are enriched with vitamins and minerals to enhance their nutritional profile. The versatility of yogurt and cream substitutes has expanded their use in a wide range of culinary applications, from breakfast bowls and smoothies to sauces and desserts, appealing to a broad audience seeking healthier, sustainable, and ethical food choices. The growth in this segment is propelled by continuous product innovation, improved availability, and increasing consumer awareness about the benefits of plant-based diets, making yogurt and cream substitutes a significant and growing part of the Global Dairy Substitutes for Milk Market.

Beverages, Desserts, Bakery, Others in the Global Dairy Substitutes for Milk Market:

The usage of Global Dairy Substitutes for Milk Market products spans across various areas including beverages, desserts, bakery, and others, reflecting their versatility and growing acceptance among consumers. In beverages, dairy substitutes like almond, soy, and oat milks are increasingly used as bases for coffee, smoothies, and protein shakes, offering lactose-free and lower-calorie options. Desserts made with dairy-free alternatives such as ice creams, yogurts, and mousses are gaining popularity for their ability to cater to dietary restrictions without compromising on taste or texture. In the bakery sector, dairy substitutes are utilized in bread, cakes, and pastries, providing moisture and richness while making the products suitable for those avoiding animal-derived ingredients. Beyond these categories, dairy substitutes find applications in a myriad of other products, including but not limited to, cheese alternatives, whipped cream, and even in non-food items like cosmetics and pharmaceuticals, showcasing their broad utility. This widespread use of dairy substitutes across different sectors is indicative of a shift towards more inclusive, health-conscious, and environmentally sustainable consumption patterns, driving growth and innovation in the Global Dairy Substitutes for Milk Market.

Global Dairy Substitutes for Milk Market Outlook:

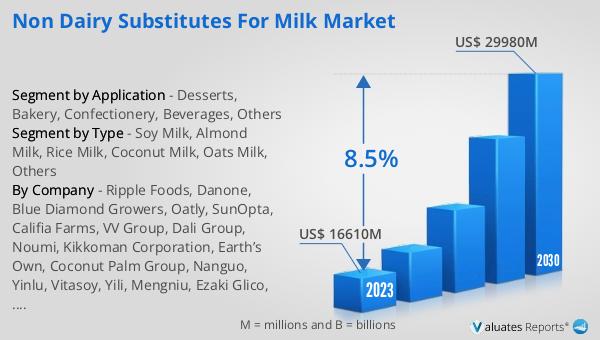

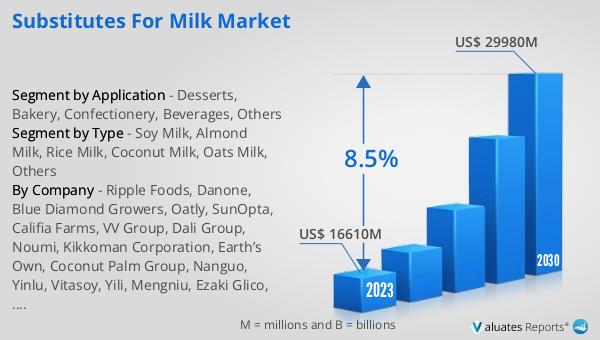

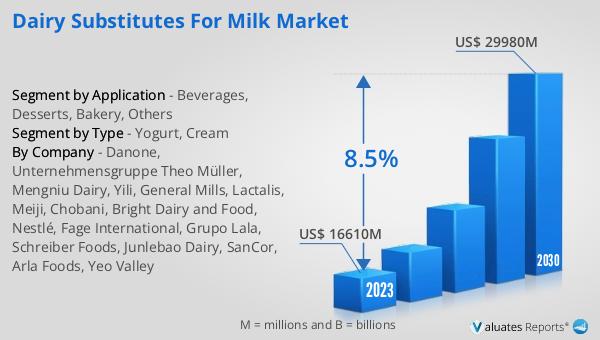

The market outlook for Global Dairy Substitutes for Milk presents a promising future, with the sector's valuation at US$ 16,610 million in 2023, and projections suggesting a climb to US$ 29,980 million by 2030. This anticipated growth, marked by a Compound Annual Growth Rate (CAGR) of 8.5% during the period from 2024 to 2030, underscores the increasing consumer shift towards plant-based alternatives and the expanding variety of options available in the market. The driving forces behind this surge include a growing awareness of health and wellness, ethical considerations regarding animal welfare, and environmental concerns. As more consumers opt for dairy-free alternatives due to dietary restrictions, lactose intolerance, or personal preference, the demand for innovative and diverse dairy substitute products continues to rise. This trend is not only reshaping consumer habits but also encouraging manufacturers to explore new formulations and product offerings, thereby fueling the market's expansion and making dairy substitutes an integral part of the global food landscape.

| Report Metric | Details |

| Report Name | Dairy Substitutes for Milk Market |

| Accounted market size in 2023 | US$ 16610 million |

| Forecasted market size in 2030 | US$ 29980 million |

| CAGR | 8.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Danone, Unternehmensgruppe Theo Müller, Mengniu Dairy, Yili, General Mills, Lactalis, Meiji, Chobani, Bright Dairy and Food, Nestlé, Fage International, Grupo Lala, Schreiber Foods, Junlebao Dairy, SanCor, Arla Foods, Yeo Valley |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |