What is Global Draw Wire Sensors Market?

The Global Draw Wire Sensors Market is a specialized segment within the broader sensor industry, focusing on devices that measure linear position and displacement. These sensors, also known as cable extension transducers or string potentiometers, are designed to convert linear motion into an electrical signal. They consist of a wire or cable wound around a spool, which extends and retracts as the object being measured moves. This movement is then translated into an electrical signal that can be interpreted by various systems. The market for these sensors is driven by their versatility and precision, making them suitable for a wide range of applications across different industries. They are particularly valued for their ability to provide accurate measurements in challenging environments, where other types of sensors might fail. The demand for draw wire sensors is expected to grow as industries continue to automate processes and require precise measurement tools. Their adaptability to various conditions and ease of integration into existing systems make them a preferred choice for many businesses looking to enhance operational efficiency and accuracy. As technology advances, the capabilities and applications of draw wire sensors are likely to expand, further solidifying their importance in the global market.

in the Global Draw Wire Sensors Market:

The Global Draw Wire Sensors Market offers a variety of types tailored to meet the diverse needs of customers across different sectors. One of the most common types is the potentiometric draw wire sensor, which uses a potentiometer to convert the linear displacement of the wire into an electrical signal. This type is favored for its simplicity and cost-effectiveness, making it suitable for applications where high precision is not the primary requirement. Another popular type is the incremental encoder-based draw wire sensor, which provides high-resolution measurements by counting the number of pulses generated as the wire extends or retracts. This type is ideal for applications requiring precise position feedback, such as in robotics or CNC machinery. Absolute encoder-based draw wire sensors offer another option, providing an absolute position reading without the need for a reference point. This feature is particularly useful in applications where the sensor may lose power or be moved during operation, as it can immediately provide an accurate position reading upon restart. Additionally, digital draw wire sensors are gaining popularity due to their ability to interface directly with digital systems, offering seamless integration into modern industrial environments. These sensors often come with advanced features such as programmable output ranges and diagnostic capabilities, enhancing their functionality and reliability. Furthermore, some draw wire sensors are designed for specific environmental conditions, such as those with rugged housings for use in harsh industrial settings or those with waterproof enclosures for outdoor applications. The choice of draw wire sensor type depends largely on the specific requirements of the application, including factors such as measurement range, accuracy, environmental conditions, and budget constraints. As the market continues to evolve, manufacturers are developing new types of draw wire sensors with enhanced features and capabilities to meet the growing demands of various industries. This ongoing innovation ensures that customers have access to a wide range of options, allowing them to select the most appropriate sensor for their specific needs.

Industrial Automation, Medical Equipment, Automotive Engineering, Military, Other in the Global Draw Wire Sensors Market:

The usage of Global Draw Wire Sensors Market spans several key areas, each benefiting from the unique capabilities of these sensors. In industrial automation, draw wire sensors are essential for monitoring and controlling the position of machinery and equipment. They provide precise feedback on the movement of components, enabling automated systems to operate with high accuracy and efficiency. This is particularly important in manufacturing processes where even minor deviations can lead to significant quality issues or production delays. In the medical equipment sector, draw wire sensors are used in devices such as patient beds and imaging equipment, where accurate positioning is crucial for patient safety and diagnostic accuracy. These sensors help ensure that equipment moves smoothly and stops at the correct position, enhancing both the functionality and safety of medical devices. In automotive engineering, draw wire sensors play a critical role in testing and development processes. They are used to measure the displacement of components such as suspension systems and steering mechanisms, providing valuable data that helps engineers optimize vehicle performance and safety. The military sector also relies on draw wire sensors for various applications, including the positioning of weapons systems and the monitoring of vehicle movements. Their robustness and reliability make them well-suited for use in demanding military environments. Additionally, draw wire sensors find applications in other areas such as construction, where they are used to monitor the movement of structures and equipment, and in the entertainment industry, where they help control the movement of stage elements and special effects. The versatility and precision of draw wire sensors make them an invaluable tool across these diverse fields, contributing to improved performance, safety, and efficiency.

Global Draw Wire Sensors Market Outlook:

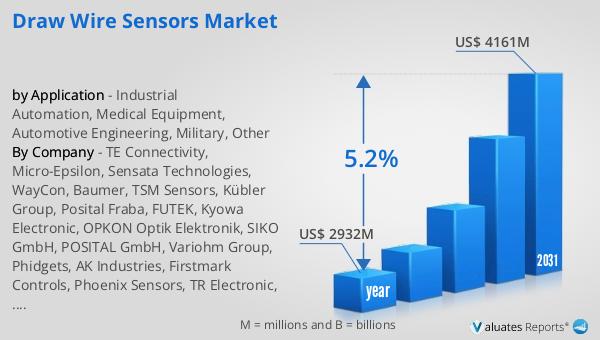

The outlook for the Global Draw Wire Sensors Market indicates a promising growth trajectory over the coming years. In 2024, the market was valued at approximately US$ 2932 million, reflecting its significant role in various industries. Looking ahead, the market is expected to expand, reaching an estimated size of US$ 4161 million by 2031. This growth represents a compound annual growth rate (CAGR) of 5.2% during the forecast period. The increasing demand for precise measurement tools in automation, medical, automotive, and military applications is a key driver of this growth. As industries continue to embrace automation and advanced technologies, the need for reliable and accurate sensors like draw wire sensors is expected to rise. These sensors offer a unique combination of precision, versatility, and ease of integration, making them an attractive choice for businesses looking to enhance their operational capabilities. The market's expansion is also supported by ongoing technological advancements, which are leading to the development of more sophisticated and capable draw wire sensors. As a result, the Global Draw Wire Sensors Market is poised to play an increasingly important role in supporting the technological advancements and efficiency improvements across various sectors.

| Report Metric | Details |

| Report Name | Draw Wire Sensors Market |

| Accounted market size in year | US$ 2932 million |

| Forecasted market size in 2031 | US$ 4161 million |

| CAGR | 5.2% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | TE Connectivity, Micro-Epsilon, Sensata Technologies, WayCon, Baumer, TSM Sensors, Kübler Group, Posital Fraba, FUTEK, Kyowa Electronic, OPKON Optik Elektronik, SIKO GmbH, POSITAL GmbH, Variohm Group, Phidgets, AK Industries, Firstmark Controls, Phoenix Sensors, TR Electronic, Wachendorff Automation, Unimeasure, Automation Sensorik Messtechnik GmbH, Changchun Rongde Optical, Danfoss, Shenzhen OIDELEC, Shenzhen Briter Technology, Shenzhen Senther Technology, Shanghai Zhichuan Technology, CALT Sensor, Shenzhen Milont Technology, by Measuring Distance, Below 20m, 20-40m, Above 40m |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |