What is Global Plant Pathogen Control Market?

The Global Plant Pathogen Control Market is a specialized sector within the agricultural industry focused on managing and mitigating the impact of pathogens that affect plant health. Pathogens such as bacteria, fungi, viruses, and nematodes can cause significant damage to crops, leading to reduced yields and economic losses. The market encompasses a range of products and solutions designed to protect plants from these harmful organisms. These include chemical treatments, biological controls, and integrated pest management strategies. The goal is to ensure healthy plant growth, improve crop productivity, and maintain food security. The market is driven by the increasing demand for high-quality crops, advancements in agricultural technologies, and the need to address the challenges posed by climate change and evolving pathogen resistance.

Bactericides, Fungicides, Nematicides, Others in the Global Plant Pathogen Control Market:

Bactericides, fungicides, nematicides, and other pathogen control agents play a crucial role in the Global Plant Pathogen Control Market. Bactericides are chemical or biological agents specifically designed to kill or inhibit the growth of harmful bacteria that can cause diseases in plants. These products are essential for managing bacterial infections that can lead to significant crop losses. Fungicides, on the other hand, target fungal pathogens that cause diseases such as mildew, rust, and blight. These chemicals work by disrupting the cellular processes of fungi, preventing them from spreading and causing further damage to plants. Nematicides are used to control nematodes, which are microscopic worms that attack plant roots, leading to stunted growth and reduced yields. These products can be chemical or biological in nature and are applied to the soil to protect plants from nematode infestations. In addition to these specific agents, the market also includes a range of other products and solutions designed to control plant pathogens. These can include natural predators, beneficial microorganisms, and plant extracts that enhance plant resistance to diseases. The use of these products is often integrated into broader pest management strategies to provide a comprehensive approach to plant health. The effectiveness of these pathogen control agents depends on various factors, including the type of pathogen, the crop being protected, and environmental conditions. As a result, farmers and agricultural professionals must carefully select and apply these products to achieve the best results. The development and use of these pathogen control agents are also subject to regulatory oversight to ensure their safety and efficacy. Overall, bactericides, fungicides, nematicides, and other pathogen control agents are essential tools in the Global Plant Pathogen Control Market, helping to protect crops, improve yields, and support sustainable agriculture.

Seeds, Foliage, Flowers, Fruit, Soil in the Global Plant Pathogen Control Market:

The usage of products and solutions from the Global Plant Pathogen Control Market extends across various areas, including seeds, foliage, flowers, fruit, and soil. In the case of seeds, pathogen control products are often applied as seed treatments to protect young plants from diseases right from the start. These treatments can include fungicides, bactericides, and other protective agents that coat the seeds and provide a barrier against pathogens. This early protection is crucial for ensuring healthy germination and robust plant growth. For foliage, pathogen control products are typically applied as sprays or dusts to the leaves and stems of plants. These treatments help to prevent and manage diseases that affect the above-ground parts of plants, such as leaf spots, blights, and mildews. By protecting the foliage, these products help to maintain the photosynthetic capacity of plants, which is essential for their growth and productivity. Flowers, being delicate and often highly susceptible to diseases, also benefit from the use of pathogen control products. These treatments help to prevent infections that can cause discoloration, wilting, and other damage to flowers, ensuring their aesthetic quality and market value. For fruit, pathogen control products are used to protect against diseases that can affect both the fruit itself and the plant as a whole. These treatments help to prevent issues such as fruit rot, mold, and other infections that can reduce the quality and shelf life of the produce. Finally, soil treatments are an important aspect of pathogen control, as many plant diseases originate from soil-borne pathogens. Soil treatments can include the application of nematicides, fungicides, and other agents that target harmful organisms in the soil. These treatments help to create a healthier growing environment for plants, reducing the risk of disease and promoting better root development. Overall, the use of pathogen control products across these various areas is essential for maintaining plant health, improving crop yields, and supporting sustainable agricultural practices.

Global Plant Pathogen Control Market Outlook:

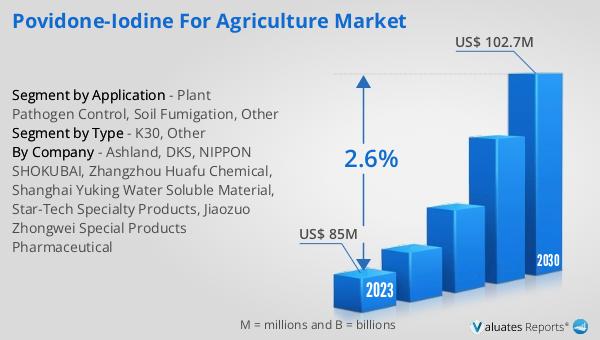

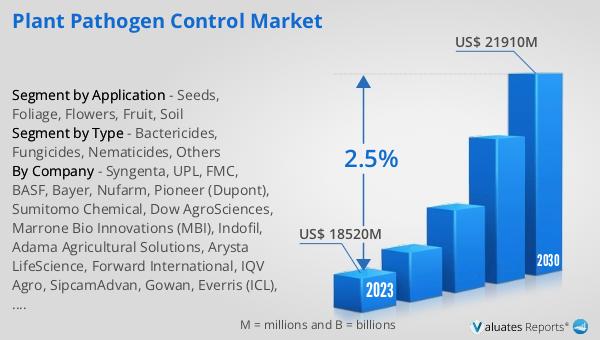

The global Plant Pathogen Control market was valued at US$ 18,520 million in 2023 and is anticipated to reach US$ 21,910 million by 2030, witnessing a CAGR of 2.5% during the forecast period 2024-2030. This market growth reflects the increasing demand for effective solutions to manage plant diseases and ensure healthy crop production. The market's expansion is driven by factors such as the rising global population, which necessitates higher agricultural productivity, and the growing awareness of the importance of plant health in achieving food security. Additionally, advancements in agricultural technologies and the development of new pathogen control products are contributing to the market's growth. The market outlook indicates a steady increase in the adoption of pathogen control solutions, as farmers and agricultural professionals seek to protect their crops from the damaging effects of pathogens. This trend is expected to continue as the agricultural industry faces ongoing challenges related to climate change, evolving pathogen resistance, and the need for sustainable farming practices. Overall, the Global Plant Pathogen Control Market is poised for growth, driven by the need to ensure healthy and productive crops in the face of various challenges.

| Report Metric | Details |

| Report Name | Plant Pathogen Control Market |

| Accounted market size in 2023 | US$ 18520 million |

| Forecasted market size in 2030 | US$ 21910 million |

| CAGR | 2.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Syngenta, UPL, FMC, BASF, Bayer, Nufarm, Pioneer (Dupont), Sumitomo Chemical, Dow AgroSciences, Marrone Bio Innovations (MBI), Indofil, Adama Agricultural Solutions, Arysta LifeScience, Forward International, IQV Agro, SipcamAdvan, Gowan, Everris (ICL), Certis USA, Acme Organics Private, Rotam, Sinochem, Limin Chemical, Shuangji Chemical, Jiangxi Heyi, Lier Chemical |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |