What is Global MEMS-based Variable Optical Attenuator Market?

The Global MEMS-based Variable Optical Attenuator Market is a specialized segment within the broader optical components industry. MEMS, or Micro-Electro-Mechanical Systems, are tiny devices that integrate electrical and mechanical components at a microscale. In the context of variable optical attenuators (VOAs), MEMS technology is used to precisely control the amount of light passing through an optical fiber. This is crucial in various optical communication systems where managing signal strength is necessary to ensure optimal performance and prevent signal degradation. The market for these devices is driven by the increasing demand for high-speed internet and data services, which require robust and efficient optical networks. As telecommunications infrastructure continues to expand globally, the need for reliable and adaptable optical components like MEMS-based VOAs is expected to grow. These devices are valued for their precision, reliability, and compact size, making them ideal for modern optical networks. The market encompasses various types of VOAs, including handheld and desktop models, each catering to different application needs and user preferences. Overall, the Global MEMS-based Variable Optical Attenuator Market plays a critical role in supporting the infrastructure of modern communication systems.

Handheld Type, Desktop Type in the Global MEMS-based Variable Optical Attenuator Market:

In the Global MEMS-based Variable Optical Attenuator Market, two primary types of devices are prevalent: handheld and desktop models. Handheld VOAs are portable devices designed for field use, offering flexibility and convenience for technicians working on-site. These devices are typically battery-powered and feature user-friendly interfaces, allowing for quick adjustments and measurements in various environments. Handheld VOAs are essential tools for field engineers who need to test and maintain optical networks, ensuring that signal levels are within optimal ranges. Their portability makes them ideal for use in remote locations or situations where quick deployment is necessary. On the other hand, desktop VOAs are designed for more permanent installations, often used in laboratory settings or network operation centers. These devices are typically larger and offer more advanced features compared to their handheld counterparts. Desktop VOAs are used for detailed analysis and testing, providing precise control over optical signals in a controlled environment. They are essential for research and development activities, as well as for quality assurance in manufacturing processes. Both handheld and desktop VOAs play crucial roles in the optical communication industry, each serving specific needs and applications. The choice between handheld and desktop models depends on the specific requirements of the task at hand, with considerations for portability, precision, and functionality. As the demand for high-speed data transmission continues to rise, the need for reliable and efficient VOAs will remain strong, driving innovation and development in this market segment. The integration of MEMS technology in these devices enhances their performance, offering improved accuracy and reliability over traditional optical attenuators. This technological advancement is a key factor in the growing adoption of MEMS-based VOAs across various industries. The versatility of these devices makes them suitable for a wide range of applications, from telecommunications to data centers and beyond. As the market evolves, manufacturers are focusing on developing more advanced and user-friendly VOAs to meet the changing needs of their customers. This includes the incorporation of smart features and connectivity options, allowing for remote monitoring and control. The ongoing development of MEMS technology is expected to further enhance the capabilities of VOAs, making them even more integral to modern optical networks. Overall, the Global MEMS-based Variable Optical Attenuator Market is characterized by a diverse range of products and applications, each contributing to the efficient operation of optical communication systems.

Fiber Optical Communiction System, Test Equipment, Others in the Global MEMS-based Variable Optical Attenuator Market:

The Global MEMS-based Variable Optical Attenuator Market finds extensive usage in several key areas, including fiber optical communication systems, test equipment, and other applications. In fiber optical communication systems, VOAs are used to manage the power levels of optical signals, ensuring that they remain within optimal ranges for transmission. This is crucial for maintaining the quality and reliability of data transmission over long distances. By adjusting the attenuation levels, VOAs help prevent signal degradation and loss, which can occur due to factors such as fiber bends, splices, and connectors. In test equipment, VOAs are used to simulate different network conditions, allowing engineers to evaluate the performance of optical components and systems under various scenarios. This is essential for the development and testing of new technologies, as well as for troubleshooting and maintenance of existing networks. VOAs provide precise control over signal levels, enabling accurate measurements and analysis. In addition to these primary applications, MEMS-based VOAs are also used in other areas such as data centers, where they help manage the distribution of optical signals across complex networks. They are also used in research and development activities, where precise control over optical signals is required for experiments and testing. The versatility and precision of MEMS-based VOAs make them valuable tools in a wide range of applications, supporting the efficient operation of modern optical networks. As the demand for high-speed data transmission continues to grow, the need for reliable and efficient VOAs will remain strong, driving further innovation and development in this market segment. The integration of MEMS technology in these devices enhances their performance, offering improved accuracy and reliability over traditional optical attenuators. This technological advancement is a key factor in the growing adoption of MEMS-based VOAs across various industries. Overall, the Global MEMS-based Variable Optical Attenuator Market plays a critical role in supporting the infrastructure of modern communication systems, providing the necessary tools for managing and optimizing optical signals.

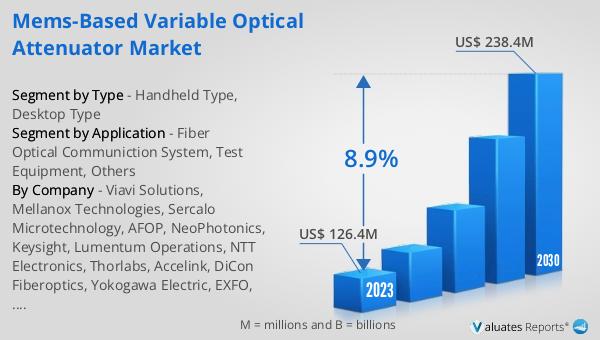

Global MEMS-based Variable Optical Attenuator Market Outlook:

The global market for MEMS-based Variable Optical Attenuators was valued at $154 million in 2024 and is anticipated to expand to a revised size of $278 million by 2031, reflecting a compound annual growth rate (CAGR) of 8.9% over the forecast period. This growth trajectory underscores the increasing demand for these devices, driven by the expanding telecommunications infrastructure and the need for efficient optical networks. As data consumption continues to rise globally, fueled by the proliferation of high-speed internet and data services, the importance of reliable and adaptable optical components like MEMS-based VOAs becomes even more pronounced. These devices are integral to maintaining the quality and efficiency of optical communication systems, ensuring that signal levels are optimized for performance. The projected growth in the market reflects the ongoing advancements in MEMS technology, which enhance the precision and reliability of VOAs. As the market evolves, manufacturers are focusing on developing more advanced and user-friendly VOAs to meet the changing needs of their customers. This includes the incorporation of smart features and connectivity options, allowing for remote monitoring and control. The ongoing development of MEMS technology is expected to further enhance the capabilities of VOAs, making them even more integral to modern optical networks. Overall, the Global MEMS-based Variable Optical Attenuator Market is poised for significant growth, driven by the increasing demand for high-speed data transmission and the need for efficient optical networks.

| Report Metric | Details |

| Report Name | MEMS-based Variable Optical Attenuator Market |

| Accounted market size in year | US$ 154 million |

| Forecasted market size in 2031 | US$ 278 million |

| CAGR | 8.9% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Viavi Solutions, Mellanox Technologies, Sercalo Microtechnology, AFOP, NeoPhotonics, Keysight, Lumentum Operations, NTT Electronics, Thorlabs, Accelink, DiCon Fiberoptics, Yokogawa Electric, EXFO, Diamond, Santec, Agiltron |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |