What is Global BOPP Film for Capacitor Market?

The Global BOPP Film for Capacitor Market refers to the worldwide industry focused on the production and distribution of Biaxially Oriented Polypropylene (BOPP) films specifically designed for use in capacitors. These films are essential components in the manufacturing of capacitors, which are devices used to store electrical energy. BOPP films are favored in this application due to their excellent dielectric properties, high insulation resistance, and ability to withstand high temperatures. The market encompasses various segments based on film thickness, application areas, and geographical regions. The demand for BOPP films in capacitors is driven by the growing need for efficient energy storage solutions across various industries, including automotive, electronics, and renewable energy sectors. As technology advances and the demand for energy-efficient solutions increases, the Global BOPP Film for Capacitor Market is expected to experience significant growth. This market is characterized by continuous innovation and development to meet the evolving needs of capacitor manufacturers and end-users. Companies operating in this market are focused on enhancing the performance characteristics of BOPP films to cater to the diverse requirements of different applications.

Below 3μm, 3~6μm, 6~9μm, 9~12μm, Above 12μm in the Global BOPP Film for Capacitor Market:

In the Global BOPP Film for Capacitor Market, film thickness plays a crucial role in determining the suitability of the film for various applications. Films with a thickness below 3μm are typically used in applications where high capacitance and low energy loss are critical. These ultra-thin films are ideal for high-frequency applications and are often used in advanced electronic devices where space is at a premium. The 3~6μm thickness range is the most commonly used in the capacitor industry, offering a balance between performance and cost. These films provide excellent dielectric properties and are suitable for a wide range of applications, including consumer electronics and automotive systems. Films in the 6~9μm range are used in applications where higher voltage ratings are required. They offer enhanced mechanical strength and are often used in industrial and power electronics applications. The 9~12μm thickness range is suitable for capacitors used in heavy-duty applications, such as power transmission and distribution systems. These films provide superior insulation and are designed to withstand harsh environmental conditions. Films above 12μm are used in specialized applications where extreme durability and high insulation resistance are required. These thick films are often used in aerospace and military applications, where reliability and performance are critical. The choice of film thickness is determined by the specific requirements of the application, including voltage rating, capacitance, and environmental conditions. Manufacturers in the Global BOPP Film for Capacitor Market are continuously innovating to develop films with improved performance characteristics to meet the diverse needs of their customers. The market is highly competitive, with companies focusing on research and development to enhance the properties of BOPP films, such as dielectric strength, thermal stability, and mechanical durability. As the demand for energy-efficient solutions continues to grow, the Global BOPP Film for Capacitor Market is expected to expand, driven by advancements in technology and the increasing adoption of renewable energy sources.

Automotive, Household Appliances, Wind and Solar power, Aerospace, Others in the Global BOPP Film for Capacitor Market:

The Global BOPP Film for Capacitor Market finds extensive usage across various sectors, including automotive, household appliances, wind and solar power, aerospace, and others. In the automotive industry, BOPP films are used in capacitors that are essential for the efficient functioning of electronic systems, such as engine control units, infotainment systems, and advanced driver-assistance systems (ADAS). These films provide the necessary insulation and dielectric properties to ensure the reliability and performance of automotive electronics. In household appliances, BOPP films are used in capacitors that help regulate power supply and improve energy efficiency. They are commonly found in appliances such as refrigerators, air conditioners, and washing machines, where they contribute to the smooth operation and longevity of the devices. In the renewable energy sector, BOPP films are used in capacitors for wind and solar power systems. These films help in the efficient storage and conversion of energy, ensuring the stability and reliability of power supply from renewable sources. In the aerospace industry, BOPP films are used in capacitors that are critical for the operation of avionics and other electronic systems. These films provide the necessary insulation and durability to withstand the extreme conditions encountered in aerospace applications. Other sectors that utilize BOPP films for capacitors include telecommunications, industrial electronics, and medical devices. The versatility and superior performance characteristics of BOPP films make them an ideal choice for a wide range of applications, driving their demand in the Global BOPP Film for Capacitor Market. As industries continue to seek energy-efficient and reliable solutions, the usage of BOPP films in capacitors is expected to grow, contributing to the overall expansion of the market.

Global BOPP Film for Capacitor Market Outlook:

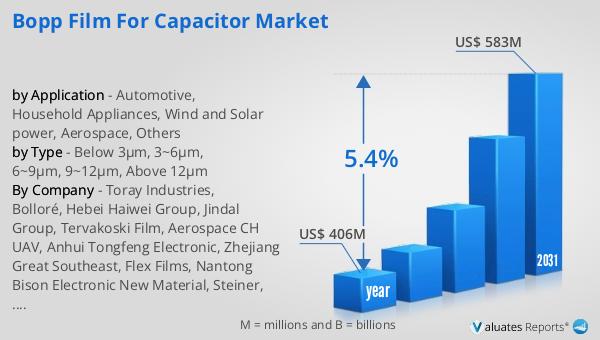

The global market for BOPP Film for Capacitor was valued at approximately 406 million USD in 2024. This market is anticipated to grow significantly, reaching an estimated size of 583 million USD by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 5.4% over the forecast period. The increasing demand for energy-efficient solutions across various industries is a key driver of this market growth. As industries such as automotive, electronics, and renewable energy continue to expand, the need for reliable and efficient capacitors is becoming more pronounced. BOPP films, with their excellent dielectric properties and high insulation resistance, are well-suited to meet these demands. The market is characterized by continuous innovation and development, with companies focusing on enhancing the performance characteristics of BOPP films to cater to the evolving needs of capacitor manufacturers and end-users. The competitive landscape of the market is shaped by the efforts of key players to develop advanced BOPP films that offer improved dielectric strength, thermal stability, and mechanical durability. As the market continues to grow, companies are expected to invest in research and development to maintain their competitive edge and meet the increasing demand for high-performance BOPP films in capacitors.

| Report Metric | Details |

| Report Name | BOPP Film for Capacitor Market |

| Accounted market size in year | US$ 406 million |

| Forecasted market size in 2031 | US$ 583 million |

| CAGR | 5.4% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Toray Industries, Bolloré, Hebei Haiwei Group, Jindal Group, Tervakoski Film, Aerospace CH UAV, Anhui Tongfeng Electronic, Zhejiang Great Southeast, Flex Films, Nantong Bison Electronic New Material, Steiner, Xpro India |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |