What is Global High-end Polyolefin Elastomer Market?

The Global High-end Polyolefin Elastomer Market is a specialized segment within the broader elastomer industry, focusing on advanced materials known for their flexibility, durability, and resistance to various environmental factors. Polyolefin elastomers (POEs) are a type of polymer that combines the properties of rubber and plastic, making them highly versatile for numerous applications. These materials are engineered to provide superior performance in demanding conditions, offering benefits such as excellent impact resistance, low-temperature flexibility, and chemical resistance. The high-end segment of this market specifically caters to industries that require top-tier performance and reliability, such as automotive, packaging, and renewable energy sectors. The demand for high-end POEs is driven by the need for materials that can withstand harsh environments while maintaining their structural integrity and performance. As industries continue to innovate and seek materials that offer both functionality and sustainability, the Global High-end Polyolefin Elastomer Market is poised for growth, driven by advancements in material science and increasing applications across various sectors. This market is characterized by continuous research and development efforts aimed at enhancing the properties of POEs to meet the evolving needs of end-users.

Injection Grade, General Grade, Extrusion Grade, Others in the Global High-end Polyolefin Elastomer Market:

In the Global High-end Polyolefin Elastomer Market, different grades of elastomers are tailored to meet specific application requirements, each offering unique properties and benefits. Injection Grade POEs are designed for applications that require precision and high-quality finishes, such as automotive parts and consumer goods. These elastomers are engineered to flow easily into molds, allowing for the production of complex shapes with fine details. They offer excellent dimensional stability and surface finish, making them ideal for components that demand aesthetic appeal and functional performance. General Grade POEs, on the other hand, provide a balance of properties suitable for a wide range of applications. They are versatile and can be used in various industries, offering good mechanical properties, chemical resistance, and ease of processing. These elastomers are often used in applications where cost-effectiveness and performance are equally important. Extrusion Grade POEs are specifically formulated for processes that involve pushing the material through a die to create continuous shapes, such as films, sheets, and pipes. These elastomers offer excellent processability, allowing for smooth and consistent extrusion. They are commonly used in the packaging industry, where they provide flexibility, strength, and clarity. Other grades of POEs are developed for niche applications that require specialized properties, such as enhanced UV resistance, flame retardancy, or specific mechanical characteristics. These elastomers are tailored to meet the unique demands of industries such as construction, electronics, and healthcare. The diversity of grades within the Global High-end Polyolefin Elastomer Market reflects the versatility and adaptability of these materials, enabling them to meet the specific needs of various applications and industries. As technology advances and new applications emerge, the development of new grades and formulations continues to drive innovation and growth in this market.

Automobile, Photovoltaic, Packaging, Others in the Global High-end Polyolefin Elastomer Market:

The Global High-end Polyolefin Elastomer Market finds extensive usage across various industries, each leveraging the unique properties of these materials to enhance product performance and functionality. In the automobile industry, high-end POEs are used to manufacture components that require flexibility, durability, and resistance to harsh environmental conditions. These elastomers are ideal for automotive parts such as seals, gaskets, and interior components, where they provide excellent impact resistance and low-temperature performance. The use of POEs in automobiles contributes to weight reduction and improved fuel efficiency, aligning with the industry's focus on sustainability and performance. In the photovoltaic sector, high-end POEs are utilized in the encapsulation of solar panels, where they offer superior weatherability and UV resistance. These materials protect the delicate components of solar panels from environmental degradation, ensuring long-term performance and reliability. The packaging industry also benefits from the properties of high-end POEs, using them to create flexible, durable, and transparent packaging solutions. These elastomers provide excellent sealability and puncture resistance, making them ideal for food packaging, medical supplies, and consumer goods. Other industries, such as construction and electronics, also leverage the unique properties of high-end POEs for applications that require specialized performance characteristics. In construction, these elastomers are used in roofing membranes and waterproofing solutions, where they offer flexibility and resistance to environmental factors. In electronics, high-end POEs are used in cable insulation and protective coatings, providing electrical insulation and mechanical protection. The versatility and adaptability of high-end POEs make them a valuable material across various sectors, driving innovation and enhancing product performance.

Global High-end Polyolefin Elastomer Market Outlook:

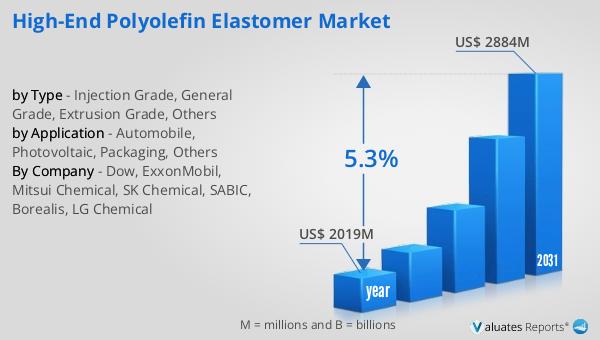

The outlook for the Global High-end Polyolefin Elastomer Market indicates a promising trajectory, with the market valued at approximately US$ 2019 million in 2024. It is anticipated to expand to a revised size of US$ 2884 million by 2031, reflecting a compound annual growth rate (CAGR) of 5.3% over the forecast period. This growth is driven by the increasing demand for high-performance materials across various industries, including automotive, packaging, and renewable energy. The market's expansion is supported by advancements in material science and the continuous development of new applications for high-end POEs. As industries seek materials that offer both functionality and sustainability, the demand for high-end POEs is expected to rise. The market's growth is also influenced by the increasing focus on reducing environmental impact and enhancing product performance. With ongoing research and development efforts, the Global High-end Polyolefin Elastomer Market is poised to meet the evolving needs of end-users, offering innovative solutions that address the challenges of modern industries. The projected growth of this market underscores the importance of high-end POEs in driving innovation and enhancing the performance of products across various sectors.

| Report Metric | Details |

| Report Name | High-end Polyolefin Elastomer Market |

| Accounted market size in year | US$ 2019 million |

| Forecasted market size in 2031 | US$ 2884 million |

| CAGR | 5.3% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Dow, ExxonMobil, Mitsui Chemical, SK Chemical, SABIC, Borealis, LG Chemical |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |