What is Global Solar Grid Connected Inverter Market?

The Global Solar Grid Connected Inverter Market is a rapidly evolving sector within the renewable energy industry, focusing on the development and deployment of inverters that connect solar power systems to the electrical grid. These inverters play a crucial role in converting the direct current (DC) electricity generated by solar panels into alternating current (AC) electricity, which can be used by homes and businesses or fed back into the grid. The market is driven by the increasing demand for clean and sustainable energy solutions, government incentives, and technological advancements that enhance the efficiency and reliability of solar power systems. As countries worldwide strive to reduce their carbon footprint and transition to renewable energy sources, the demand for solar grid-connected inverters is expected to grow significantly. This market encompasses various types of inverters, including centralized, string, and microinverters, each catering to different scales and configurations of solar installations. The global push towards renewable energy, coupled with the declining costs of solar technology, positions the solar grid-connected inverter market as a key component in the future of energy production and consumption.

Centralized Inverter, String Inverter, Others in the Global Solar Grid Connected Inverter Market:

Centralized inverters, string inverters, and other types of inverters each play a distinct role in the Global Solar Grid Connected Inverter Market, catering to different needs and scales of solar installations. Centralized inverters are typically used in large-scale solar power plants. They are designed to handle high power levels, often in the megawatt range, and are known for their efficiency and cost-effectiveness in large installations. These inverters consolidate the DC power from multiple solar panels into a single unit, converting it into AC power for grid distribution. Their centralized nature allows for easier maintenance and monitoring, but they can be less flexible in terms of system design and expansion compared to other types.

String inverters, on the other hand, are more commonly used in residential and commercial solar installations. They are designed to handle smaller power levels, typically ranging from a few kilowatts to several hundred kilowatts. String inverters connect a series of solar panels, or a "string," to a single inverter unit. This setup allows for greater flexibility in system design and is easier to scale up or down as needed. String inverters are known for their reliability and ease of installation, making them a popular choice for homeowners and small businesses looking to harness solar energy.

In addition to centralized and string inverters, there are other types of inverters that cater to specific needs within the solar grid-connected inverter market. Microinverters, for example, are designed to be installed on individual solar panels, allowing for maximum energy harvest and system flexibility. They are particularly useful in installations where shading or panel orientation may vary, as each panel operates independently. This can lead to higher overall system efficiency and easier troubleshooting, as issues can be isolated to individual panels rather than affecting the entire system.

Hybrid inverters are another category within the market, offering the ability to manage both solar power and energy storage systems. These inverters are becoming increasingly popular as more consumers and businesses look to incorporate battery storage into their solar installations. Hybrid inverters allow for seamless integration of solar power and stored energy, providing greater energy independence and resilience against grid outages.

Overall, the Global Solar Grid Connected Inverter Market is characterized by a diverse range of products designed to meet the varying needs of solar energy consumers. Whether for large-scale power plants, residential rooftops, or commercial installations, the choice of inverter plays a critical role in the efficiency, reliability, and scalability of solar power systems. As technology continues to advance and the demand for renewable energy grows, the market for solar grid-connected inverters is poised for significant expansion, offering a wide array of solutions to meet the world's energy needs.

Home, Industrial, Others in the Global Solar Grid Connected Inverter Market:

The usage of Global Solar Grid Connected Inverter Market products spans across various sectors, including residential homes, industrial applications, and other areas, each with unique requirements and benefits. In residential settings, solar grid-connected inverters are primarily used to convert the DC electricity generated by rooftop solar panels into AC electricity that can be used to power household appliances. This not only reduces reliance on traditional energy sources but also allows homeowners to potentially sell excess electricity back to the grid, providing an additional source of income. The integration of solar inverters in homes is often driven by the desire for energy independence, cost savings on electricity bills, and environmental consciousness. With advancements in technology, modern inverters offer features such as remote monitoring and smart grid compatibility, enhancing their appeal to tech-savvy homeowners.

In industrial applications, solar grid-connected inverters are used to power large-scale operations, often in conjunction with other renewable energy sources. Industries with high energy demands, such as manufacturing, mining, and agriculture, benefit from the cost savings and sustainability offered by solar power. In these settings, inverters must be robust and capable of handling significant power loads, often requiring centralized or string inverter configurations. The use of solar inverters in industrial applications is also driven by corporate sustainability goals and regulatory requirements to reduce carbon emissions. By integrating solar power into their energy mix, industries can not only lower their operational costs but also enhance their brand image as environmentally responsible entities.

Beyond residential and industrial applications, solar grid-connected inverters find usage in various other areas, including commercial buildings, educational institutions, and public infrastructure projects. In commercial buildings, solar inverters help reduce energy costs and contribute to green building certifications, which are increasingly important in the real estate market. Educational institutions use solar power to lower operational costs and serve as a teaching tool for students, demonstrating the practical applications of renewable energy. Public infrastructure projects, such as street lighting and transportation systems, also benefit from the integration of solar inverters, providing reliable and sustainable energy solutions.

The versatility of solar grid-connected inverters makes them an essential component in the transition to renewable energy across different sectors. As technology continues to evolve, the efficiency and capabilities of these inverters are expected to improve, further driving their adoption. The global push towards sustainability and the increasing affordability of solar technology are key factors contributing to the growing usage of solar grid-connected inverters in homes, industries, and beyond.

Global Solar Grid Connected Inverter Market Outlook:

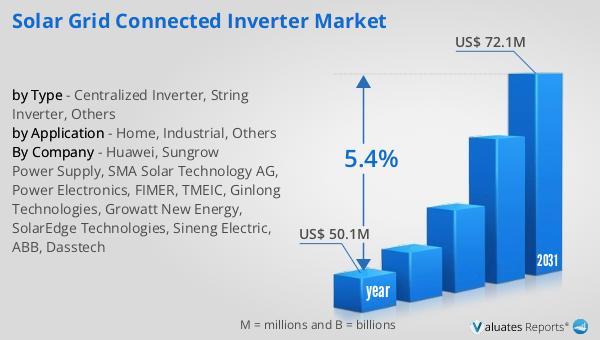

The global market for solar grid-connected inverters was valued at approximately $50.1 million in 2024, with projections indicating a growth to around $72.1 million by 2031. This growth represents a compound annual growth rate (CAGR) of 5.4% over the forecast period. The market's expansion is driven by the increasing demand for renewable energy solutions and the technological advancements that enhance the efficiency and reliability of solar power systems. According to the International Energy Agency, China holds a dominant position in the market, with its share in all key products of the supply chain exceeding 80%. This significant market share highlights China's role as a major player in the global solar industry, driven by its large-scale manufacturing capabilities and government support for renewable energy initiatives.

The growth of the solar grid-connected inverter market is also influenced by the declining costs of solar technology, making it more accessible to a broader range of consumers and businesses. As countries worldwide strive to reduce their carbon footprint and transition to renewable energy sources, the demand for solar grid-connected inverters is expected to grow significantly. This market encompasses various types of inverters, including centralized, string, and microinverters, each catering to different scales and configurations of solar installations. The global push towards renewable energy, coupled with the declining costs of solar technology, positions the solar grid-connected inverter market as a key component in the future of energy production and consumption.

| Report Metric |

Details |

| Report Name |

Solar Grid Connected Inverter Market |

| Accounted market size in year |

US$ 50.1 million |

| Forecasted market size in 2031 |

US$ 72.1 million |

| CAGR |

5.4% |

| Base Year |

year |

| Forecasted years |

2025 - 2031 |

| by Type |

- Centralized Inverter

- String Inverter

- Others

|

| by Application |

|

| Production by Region |

- North America

- Europe

- China

- Japan

|

| Consumption by Region |

- North America (United States, Canada)

- Europe (Germany, France, UK, Italy, Russia)

- Asia-Pacific (China, Japan, South Korea, Taiwan)

- Southeast Asia (India)

- Latin America (Mexico, Brazil)

|

| By Company |

Huawei, Sungrow Power Supply, SMA Solar Technology AG, Power Electronics, FIMER, TMEIC, Ginlong Technologies, Growatt New Energy, SolarEdge Technologies, Sineng Electric, ABB, Dasstech |

| Forecast units |

USD million in value |

| Report coverage |

Revenue and volume forecast, company share, competitive landscape, growth factors and trends |