What is Global Semiconductor Monocrystalline Silicon Furnace Market?

The Global Semiconductor Monocrystalline Silicon Furnace Market is a specialized sector within the broader semiconductor industry, focusing on the production of high-purity silicon crystals. These crystals are essential for manufacturing semiconductor devices, which are the building blocks of modern electronics. The market revolves around the use of furnaces designed to produce monocrystalline silicon, a material known for its uniform structure and superior electronic properties. These furnaces employ advanced techniques to grow silicon crystals from a single seed crystal, ensuring the resulting material has minimal defects and high conductivity. The demand for monocrystalline silicon is driven by its critical role in producing integrated circuits, solar cells, and other electronic components. As technology advances, the need for more efficient and powerful electronic devices continues to grow, fueling the demand for high-quality silicon. This market is characterized by continuous innovation, as manufacturers strive to improve the efficiency and cost-effectiveness of silicon production. The global reach of this market is evident, with key players operating in various regions to meet the increasing demand for semiconductor devices worldwide. The market's growth is supported by ongoing research and development efforts aimed at enhancing the quality and performance of monocrystalline silicon.

Czochralski (CZ) Method, Floating Zone (FZ) Method in the Global Semiconductor Monocrystalline Silicon Furnace Market:

The Czochralski (CZ) Method and Floating Zone (FZ) Method are two predominant techniques used in the Global Semiconductor Monocrystalline Silicon Furnace Market for producing high-quality silicon crystals. The Czochralski Method, named after its inventor Jan Czochralski, involves melting high-purity silicon in a crucible and then dipping a seed crystal into the molten silicon. The seed crystal is slowly pulled upwards while rotating, allowing a large single crystal to form as the silicon solidifies. This method is widely used due to its ability to produce large-diameter crystals, which are essential for manufacturing large wafers used in semiconductor devices. The CZ method is known for its efficiency and scalability, making it a preferred choice for mass production. However, it can introduce impurities from the crucible material, which may affect the crystal's purity. On the other hand, the Floating Zone Method is a crucible-free technique that involves passing a polycrystalline silicon rod through a heating coil, creating a molten zone that moves along the rod. A seed crystal is placed at one end of the rod, and as the molten zone passes, the silicon solidifies into a single crystal. The FZ method is renowned for producing extremely pure silicon crystals, as it eliminates contamination from the crucible. This method is particularly advantageous for applications requiring high-purity silicon, such as power electronics and high-frequency devices. However, the FZ method is less scalable than the CZ method, as it is more challenging to produce large-diameter crystals. Both methods play a crucial role in the semiconductor industry, each offering unique advantages and limitations. The choice between the CZ and FZ methods depends on the specific requirements of the application, such as the desired crystal size, purity, and production volume. As the demand for advanced semiconductor devices continues to rise, these methods remain integral to the production of high-quality monocrystalline silicon. Ongoing research and development efforts aim to enhance these techniques, improving their efficiency and reducing production costs. The global semiconductor industry relies heavily on these methods to meet the growing demand for electronic devices, driving innovation and technological advancements in the field.

6 Inches, 8 Inches, 12 Inches, Others in the Global Semiconductor Monocrystalline Silicon Furnace Market:

The Global Semiconductor Monocrystalline Silicon Furnace Market caters to various wafer sizes, including 6 inches, 8 inches, 12 inches, and others, each serving different applications within the semiconductor industry. The 6-inch wafers, once the standard in the industry, are now primarily used for niche applications and in the production of certain types of sensors and discrete devices. These wafers are favored for their lower cost and are often utilized in applications where cutting-edge technology is not a primary requirement. The 8-inch wafers, on the other hand, are widely used in the production of microcontrollers, analog devices, and power management circuits. They offer a balance between cost and performance, making them suitable for a broad range of applications, including automotive electronics and consumer devices. The transition from 6-inch to 8-inch wafers marked a significant advancement in the industry, allowing for increased production efficiency and reduced costs. The 12-inch wafers represent the current standard for high-volume production of advanced semiconductor devices. These larger wafers enable manufacturers to produce more chips per wafer, significantly reducing the cost per chip and increasing overall production efficiency. The use of 12-inch wafers is prevalent in the production of microprocessors, memory chips, and other high-performance devices used in computers, smartphones, and data centers. The shift towards 12-inch wafers has been driven by the need for more powerful and efficient electronic devices, as well as the demand for higher production volumes. Other wafer sizes, such as those used in specialized applications, continue to play a role in the industry, catering to specific needs that cannot be met by standard wafer sizes. The choice of wafer size depends on various factors, including the intended application, cost considerations, and technological requirements. As the semiconductor industry continues to evolve, the demand for different wafer sizes will be influenced by advancements in technology and changes in market dynamics. The Global Semiconductor Monocrystalline Silicon Furnace Market plays a critical role in supporting this demand, providing the necessary infrastructure and technology to produce high-quality silicon wafers of various sizes.

Global Semiconductor Monocrystalline Silicon Furnace Market Outlook:

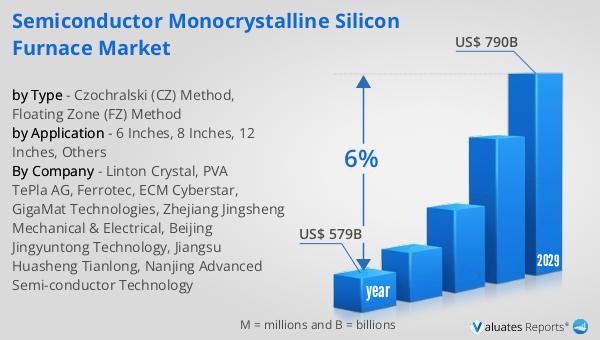

In 2022, the global semiconductor market was valued at approximately $579 billion, and it is anticipated to reach around $790 billion by 2029, reflecting a compound annual growth rate (CAGR) of 6% over the forecast period. This growth trajectory underscores the increasing demand for semiconductor devices across various industries, driven by technological advancements and the proliferation of electronic devices. The semiconductor market's expansion is fueled by the rising adoption of technologies such as artificial intelligence, the Internet of Things (IoT), and 5G connectivity, which require advanced semiconductor components to function effectively. Additionally, the growing demand for consumer electronics, automotive electronics, and industrial automation systems contributes to the market's upward trend. As industries continue to embrace digital transformation, the need for more efficient and powerful semiconductor devices becomes increasingly critical. The market's growth is also supported by ongoing research and development efforts aimed at enhancing the performance and capabilities of semiconductor components. This dynamic landscape presents numerous opportunities for innovation and investment, as companies strive to meet the evolving needs of consumers and industries worldwide. The projected growth of the semiconductor market highlights its vital role in shaping the future of technology and its impact on various sectors of the global economy.

| Report Metric | Details |

| Report Name | Semiconductor Monocrystalline Silicon Furnace Market |

| Accounted market size in year | US$ 579 billion |

| Forecasted market size in 2029 | US$ 790 billion |

| CAGR | 6% |

| Base Year | year |

| Forecasted years | 2025 - 2029 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Linton Crystal, PVA TePla AG, Ferrotec, ECM Cyberstar, GigaMat Technologies, Zhejiang Jingsheng Mechanical & Electrical, Beijing Jingyuntong Technology, Jiangsu Huasheng Tianlong, Nanjing Advanced Semi-conductor Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |