What is Global Piezoresistive Strain Gauge Transducers Market?

The Global Piezoresistive Strain Gauge Transducers Market is a specialized segment within the broader field of sensor technology, focusing on devices that measure strain or deformation in materials. These transducers are essential in various industries because they convert mechanical strain into an electrical signal, which can be easily measured and analyzed. The market for these devices is driven by the increasing demand for precise and reliable measurement tools in sectors such as automotive, aerospace, construction, and manufacturing. As industries continue to advance technologically, the need for accurate data collection and analysis becomes more critical, thereby boosting the demand for piezoresistive strain gauge transducers. These transducers are known for their high sensitivity and ability to provide accurate readings even in challenging environments, making them indispensable in applications where precision is paramount. The market is characterized by continuous innovation, with manufacturers striving to enhance the performance and durability of these devices to meet the evolving needs of end-users. As a result, the Global Piezoresistive Strain Gauge Transducers Market is poised for steady growth, driven by technological advancements and the expanding application scope of these transducers across various industries.

Foil Strain Gage, Wire Strain Gage, Semiconductor Strain Gage in the Global Piezoresistive Strain Gauge Transducers Market:

Foil strain gauges, wire strain gauges, and semiconductor strain gauges are three primary types of strain gauges used in the Global Piezoresistive Strain Gauge Transducers Market, each with distinct characteristics and applications. Foil strain gauges are widely used due to their versatility and reliability. They consist of a thin metallic foil arranged in a grid pattern, which is bonded to a backing material. When subjected to strain, the foil deforms, causing a change in electrical resistance that can be measured. These gauges are known for their accuracy and stability, making them suitable for a wide range of applications, including structural testing and load measurement. Wire strain gauges, on the other hand, use a fine wire arranged in a grid pattern. They are typically used in applications where high precision is required, such as in laboratory experiments and high-stress environments. Wire strain gauges are valued for their high sensitivity and ability to measure minute changes in strain, although they can be more fragile compared to foil gauges. Semiconductor strain gauges are made from silicon or germanium and are known for their high sensitivity and small size. They operate on the principle that the electrical resistance of a semiconductor material changes significantly with strain. These gauges are often used in applications where space is limited, or where very high sensitivity is required, such as in microelectromechanical systems (MEMS) and other advanced technologies. Each type of strain gauge has its advantages and limitations, and the choice of gauge depends on the specific requirements of the application, such as the level of precision needed, the environmental conditions, and the available space for installation. In the Global Piezoresistive Strain Gauge Transducers Market, manufacturers continue to innovate and improve these gauges to meet the growing demand for more accurate and reliable measurement tools across various industries.

Load Transducer, Pressure Transducer, Torque Transducer, Others in the Global Piezoresistive Strain Gauge Transducers Market:

The Global Piezoresistive Strain Gauge Transducers Market finds extensive usage in several key areas, including load transducers, pressure transducers, torque transducers, and other specialized applications. Load transducers, also known as load cells, are devices that measure force or weight. They are widely used in industries such as manufacturing, automotive, and aerospace to ensure the safety and efficiency of machinery and structures. Piezoresistive strain gauge transducers are integral to load cells because they provide accurate and reliable measurements of force, which are critical for maintaining the structural integrity and performance of various systems. Pressure transducers, on the other hand, are used to measure the pressure of gases or liquids. These devices are essential in industries such as oil and gas, chemical processing, and HVAC systems, where precise pressure measurements are crucial for process control and safety. Piezoresistive strain gauge transducers are favored in pressure transducers due to their high sensitivity and ability to operate in harsh environments. Torque transducers measure the rotational force applied to an object, such as a shaft or a bolt. They are commonly used in automotive and industrial applications to monitor and control the performance of engines, motors, and other rotating machinery. Piezoresistive strain gauge transducers are ideal for torque measurement because they can accurately detect small changes in rotational force, ensuring optimal performance and efficiency. In addition to these primary applications, piezoresistive strain gauge transducers are also used in other specialized areas, such as medical devices, robotics, and consumer electronics, where precise measurement and control are essential. The versatility and reliability of these transducers make them indispensable in a wide range of industries, driving their demand and growth in the global market.

Global Piezoresistive Strain Gauge Transducers Market Outlook:

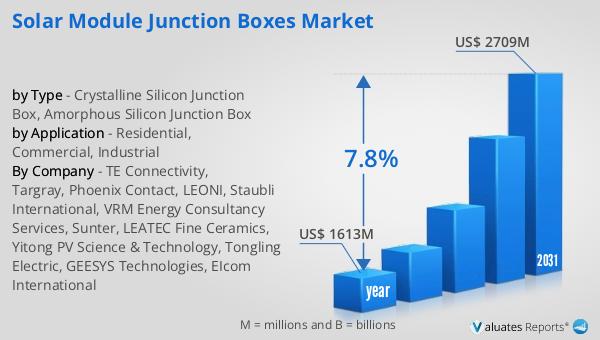

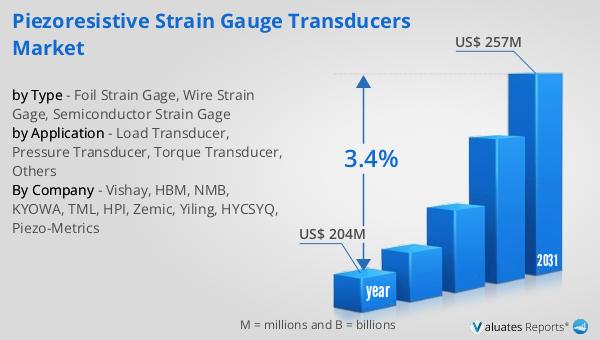

The global market for Piezoresistive Strain Gauge Transducers was valued at $204 million in 2024 and is anticipated to expand to a revised size of $257 million by 2031, reflecting a compound annual growth rate (CAGR) of 3.4% over the forecast period. This growth trajectory underscores the increasing demand for precise and reliable measurement tools across various industries. As technological advancements continue to reshape sectors such as automotive, aerospace, and manufacturing, the need for accurate data collection and analysis becomes more critical, thereby driving the demand for piezoresistive strain gauge transducers. These devices are known for their high sensitivity and ability to provide accurate readings even in challenging environments, making them indispensable in applications where precision is paramount. The market is characterized by continuous innovation, with manufacturers striving to enhance the performance and durability of these devices to meet the evolving needs of end-users. As a result, the Global Piezoresistive Strain Gauge Transducers Market is poised for steady growth, driven by technological advancements and the expanding application scope of these transducers across various industries.

| Report Metric | Details |

| Report Name | Piezoresistive Strain Gauge Transducers Market |

| Accounted market size in year | US$ 204 million |

| Forecasted market size in 2031 | US$ 257 million |

| CAGR | 3.4% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Vishay, HBM, NMB, KYOWA, TML, HPI, Zemic, Yiling, HYCSYQ, Piezo-Metrics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |