What is Global Stationary Containment Fill Station Market?

The Global Stationary Containment Fill Station Market is a niche yet vital segment within the broader industrial and safety equipment landscape. These fill stations are designed to safely and efficiently refill air cylinders, which are crucial for various applications, including firefighting, industrial safety, and other emergency services. The market is driven by the increasing demand for safety equipment in industries and the need for efficient and reliable systems to ensure the safety of personnel working in hazardous environments. Stationary containment fill stations are preferred for their durability, ease of use, and ability to handle high-pressure refills, making them indispensable in settings where safety cannot be compromised. The market is characterized by technological advancements aimed at enhancing the efficiency and safety of these systems, as well as by regulatory standards that mandate the use of such equipment in certain industries. As industries continue to prioritize safety and compliance, the demand for stationary containment fill stations is expected to grow, driven by both new installations and the replacement of outdated systems. This market is poised for steady growth as it adapts to the evolving needs of its end-users.

One Position, Two Position, Three Position in the Global Stationary Containment Fill Station Market:

In the Global Stationary Containment Fill Station Market, the terms One Position, Two Position, and Three Position refer to the number of fill positions available in a containment fill station. These configurations are crucial as they determine the station's capacity to refill multiple air cylinders simultaneously, which can significantly impact operational efficiency and response times in critical situations. A One Position fill station is designed to accommodate a single air cylinder at a time. This configuration is typically used in smaller facilities or in situations where the demand for refilling is not high. It offers a compact and cost-effective solution for organizations with limited space or budget constraints. Despite its limited capacity, a One Position fill station is built to the same safety and performance standards as larger models, ensuring reliable operation. Two Position fill stations, on the other hand, can accommodate two air cylinders simultaneously. This configuration is ideal for medium-sized operations where there is a moderate demand for refilling. By allowing two cylinders to be refilled at once, these stations can effectively double the throughput compared to a One Position station, making them a more efficient choice for organizations that require a higher volume of refills. The Three Position fill station is the largest standard configuration, capable of handling three air cylinders at once. This setup is best suited for large facilities or operations with a high demand for refilling, such as busy fire departments or large industrial sites. The ability to refill three cylinders simultaneously can significantly reduce downtime and improve operational readiness, which is critical in emergency situations. Each of these configurations is designed with safety as a top priority, incorporating features such as pressure relief valves, containment shields, and user-friendly controls to ensure safe and efficient operation. The choice between One, Two, or Three Position fill stations depends largely on the specific needs and operational demands of the end-user. Factors such as the volume of refills required, available space, budget, and the criticality of the operations being supported all play a role in determining the most suitable configuration. As the Global Stationary Containment Fill Station Market continues to evolve, manufacturers are focusing on enhancing the flexibility and adaptability of these systems to meet the diverse needs of their customers. This includes the development of modular designs that allow for easy upgrades or expansions, as well as the integration of advanced technologies such as digital monitoring and automated controls to further improve efficiency and safety. In summary, the One Position, Two Position, and Three Position configurations in the Global Stationary Containment Fill Station Market offer a range of options to suit different operational requirements, ensuring that organizations can choose a solution that best meets their needs while maintaining the highest standards of safety and performance.

Fire Departments, Industrial Facilities, Others in the Global Stationary Containment Fill Station Market:

The Global Stationary Containment Fill Station Market finds extensive usage across various sectors, with fire departments, industrial facilities, and other areas being the primary users. In fire departments, these fill stations are indispensable tools that ensure firefighters have a constant supply of breathable air during emergencies. Firefighters rely on self-contained breathing apparatus (SCBA) to protect themselves from smoke and toxic fumes, and the ability to quickly and safely refill these air cylinders is crucial for maintaining operational readiness. Stationary containment fill stations provide a reliable solution for refilling SCBA cylinders, allowing fire departments to respond swiftly and effectively to emergencies. In industrial facilities, stationary containment fill stations play a vital role in ensuring the safety of workers in hazardous environments. Industries such as chemical manufacturing, oil and gas, and mining often require workers to use breathing apparatus to protect against exposure to harmful substances. These fill stations enable the efficient refilling of air cylinders, ensuring that workers have access to clean air at all times. By maintaining a steady supply of refilled cylinders, industrial facilities can minimize downtime and enhance the safety of their operations. Beyond fire departments and industrial facilities, stationary containment fill stations are also used in other areas where safety is a priority. This includes sectors such as healthcare, where clean air is essential for certain medical procedures, and in emergency response teams that require portable breathing apparatus for rescue operations. The versatility and reliability of these fill stations make them a valuable asset in any setting where the safety of personnel is paramount. The usage of stationary containment fill stations in these areas is driven by the need for efficient and reliable systems that can handle high-pressure refills while ensuring the safety of users. These stations are designed to meet stringent safety standards, incorporating features such as pressure relief valves, containment shields, and user-friendly controls to prevent accidents and ensure smooth operation. As safety regulations become more stringent and industries continue to prioritize the well-being of their personnel, the demand for stationary containment fill stations is expected to grow. This growth is further supported by technological advancements that enhance the efficiency and safety of these systems, making them an increasingly attractive option for organizations across various sectors. In conclusion, the Global Stationary Containment Fill Station Market plays a crucial role in supporting the safety and operational efficiency of fire departments, industrial facilities, and other areas where the availability of breathable air is essential. By providing a reliable solution for refilling air cylinders, these fill stations help ensure that personnel can perform their duties safely and effectively, even in the most challenging environments.

Global Stationary Containment Fill Station Market Outlook:

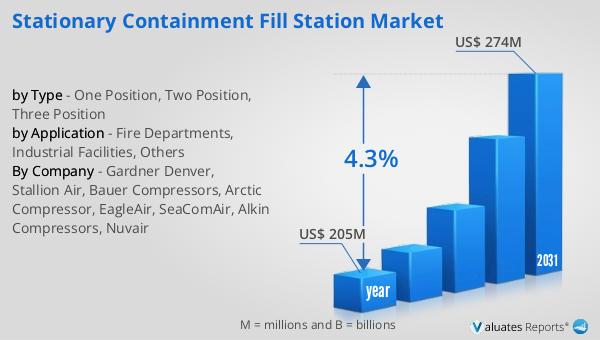

The outlook for the Global Stationary Containment Fill Station Market indicates a promising trajectory. In 2024, the market was valued at approximately $205 million, reflecting its significance in the safety equipment sector. Looking ahead, projections suggest that by 2031, the market will expand to an estimated $274 million. This growth represents a compound annual growth rate (CAGR) of 4.3% over the forecast period. Such a steady increase underscores the rising demand for efficient and reliable fill stations across various industries. The market's expansion is driven by several factors, including the growing emphasis on safety and compliance in industrial operations, advancements in technology that enhance the functionality and safety of fill stations, and the increasing need for quick and efficient refilling solutions in emergency services. As industries continue to prioritize the safety of their personnel and the efficiency of their operations, the demand for stationary containment fill stations is expected to rise. This growth trajectory highlights the market's resilience and adaptability in meeting the evolving needs of its end-users. As a result, manufacturers are likely to focus on innovation and the development of advanced features to maintain a competitive edge and cater to the diverse requirements of their customers. Overall, the Global Stationary Containment Fill Station Market is poised for steady growth, driven by the increasing demand for safety equipment and the continuous evolution of industry standards and technologies.

| Report Metric | Details |

| Report Name | Stationary Containment Fill Station Market |

| Accounted market size in year | US$ 205 million |

| Forecasted market size in 2031 | US$ 274 million |

| CAGR | 4.3% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Gardner Denver, Stallion Air, Bauer Compressors, Arctic Compressor, EagleAir, SeaComAir, Alkin Compressors, Nuvair |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |